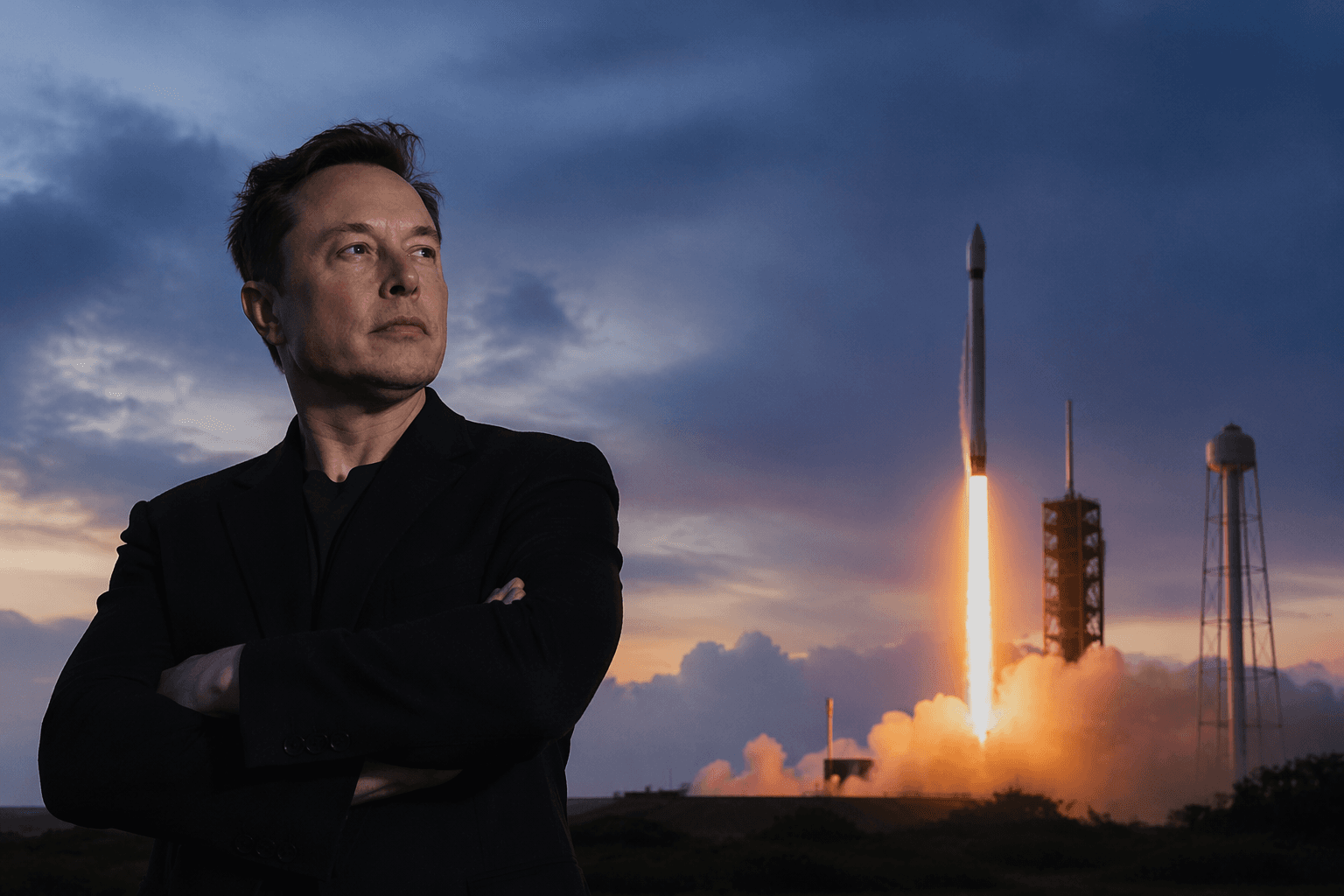

SpaceX launches record IPO, Elon Musk becomes trillionaire

SpaceX's public debut priced 555,555,555 shares at $135, making it the largest IPO ever and lifting Elon Musk into trillionaire status.

SpaceX turned its long-awaited market debut into a milestone for both Wall Street and Silicon Valley, opening a roadshow for 555,555,555 shares of Class A common stock at an expected $135 a share. The offering, which includes a 30-day underwriters’ option for up to 83,333,333 additional shares, was described by the company as the largest initial public offering ever and came with Elon Musk now holding the title of trillionaire.

The company said it planned to list on the Nasdaq Global Select Market and Nasdaq Texas under the ticker SPCX. Its filing also said the registration statement had not yet become effective when the offering was first announced, underscoring that the deal still has formal steps to clear even as investor demand is being tested. SpaceX said the roadshow was launched from Starbase, Texas, on June 4.

Beyond the headline number, the offering pushes SpaceX’s core businesses into a new phase of market scrutiny. The company’s materials highlight its scale in launch services, satellite connectivity and AI infrastructure, signaling to investors that SpaceX wants to be valued not just as a rocket maker but as a broad industrial and technology platform with global reach. Its prospectus materials point to a distribution spanning the United States, Europe, Canada, Australia and Japan.

The debut lands at a moment when capital markets are rewarding companies that control hard-to-replicate infrastructure, and it gives public investors a direct stake in a business that has shaped commercial launch economics and satellite communications. For Musk, the listing expands the visibility of his wealth and influence at a time when his companies continue to sit at the center of aerospace, telecom and artificial intelligence competition.

In a separate deal that speaks to the same appetite for scale, the Justice Department gave the green light to the merger between Paramount Skydance and Warner Bros. Discovery after an eight-month review. The department said the transaction was not likely to harm competition or American consumers in streaming video on demand, linear television or film production and distribution, and said its review covered more than two million documents and involved state attorneys general.

The approval clears a major federal hurdle for a deal valued at about $110 billion to $111 billion, but it does not end the fight. The combined company would unite Paramount+ and HBO Max into a streaming service with roughly 200 million subscribers, and state-level legal challenges still loom, including in California. Paramount has argued the merger would create a stronger company better able to compete with dominant technology platforms, and David Ellison has told investors the deal is on track to close by September, with a ticking fee set to begin after that point.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip