SpaceX pitches $28.5 trillion market, says AI dwarfs its space business

SpaceX is selling investors on a $28.5 trillion market, but more than 90% of that case rests on AI, not rockets or Starlink. Its control-heavy IPO structure raises the stakes.

SpaceX is asking investors to look past rockets and satellite internet and buy into a far larger story: a business it says could compete in a $28.5 trillion total addressable market. More than 90% of that opportunity is tied to artificial intelligence, with the largest share in enterprise software and services, a pitch that recasts Elon Musk’s space company as an AI platform company just as it prepares for a summer IPO at an estimated $1.75 trillion valuation.

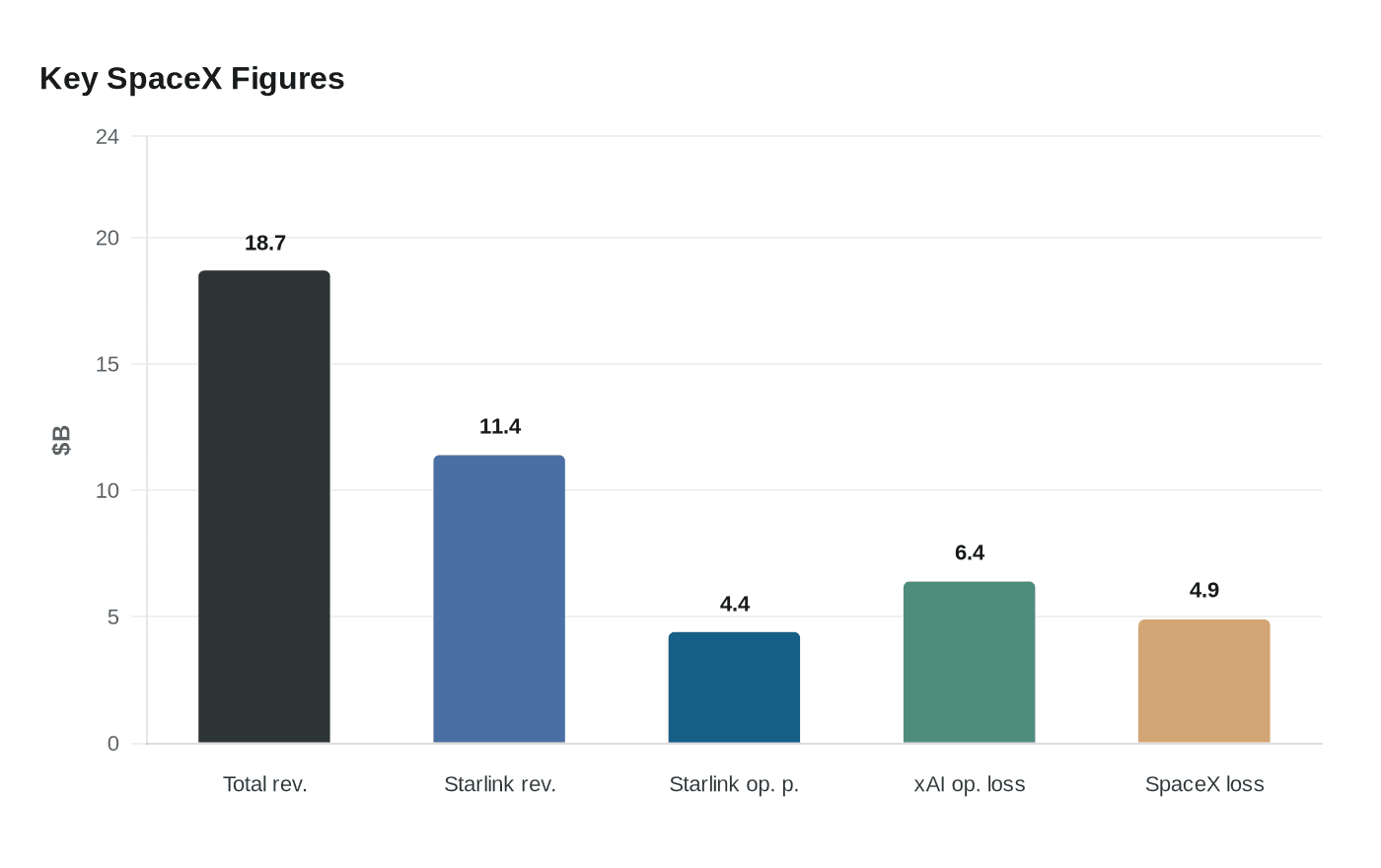

That framing marks a sharp break from SpaceX’s traditional identity. Starlink remains the company’s biggest revenue engine, generating $11.4 billion of SpaceX’s $18.7 billion in 2025 revenue and delivering $4.4 billion in operating profit. Yet the new AI push has become large enough to dominate the internal financial picture. xAI, which SpaceX acquired in February 2026, posted a $6.4 billion operating loss last year, up from $1.6 billion a year earlier. SpaceX as a whole still reported a $4.9 billion loss in 2025 even as it poured $20.7 billion into capital spending, including $12.7 billion tied to AI.

The expansion case is bold, but it is not yet proven. Musk has linked the merger with xAI to orbital data centers, signaling that he sees AI as the next major layer in his business empire rather than a side venture. SpaceX also secured an option to buy Cursor for $60 billion or alternatively pay $10 billion for a partnership, another sign that the company is trying to build an AI stack around its existing infrastructure. For investors, the question is whether those bets turn SpaceX’s enormous balance-sheet commitment into a durable new profit center, or whether they deepen exposure to a still-loss-making strategy.

The governance structure is just as consequential as the growth story. SpaceX plans to keep controlled-company status after the IPO, which means it would not need a majority-independent board or independent nominating and compensation committees. Only the audit committee would have to be fully independent, a standard feature for controlled companies. Musk and a small group of insiders would also hold super-voting shares, preserving his grip on the board even after the listing. Meta Platforms is a public-market precedent for this kind of structure, but a National Association of Corporate Directors study cited in the deal materials found that only about 3% to 4% of Russell 3000 companies had insider-majority boards.

That combination, a record-sized IPO, a massive AI claim and unusually concentrated control, is what makes SpaceX’s offering stand apart. The company is not just selling growth. It is asking investors to underwrite Musk’s next empire while accepting that they will have little say in how it is run.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?