SpaceX raises $25 billion in bond sale, drawing huge demand

SpaceX’s $25 billion bond sale drew nearly $89 billion of orders, spotlighting investor appetite for Musk-linked credit and the concentration risk behind it.

SpaceX’s $25 billion bond sale drew nearly $89 billion of orders, a demand surge that showed how far investors will stretch for exposure to Elon Musk’s company. The size of the deal also sharpened a harder question for credit markets: whether buyers are building smart access to the space economy or concentrating too much risk in one iconic, opaque private name.

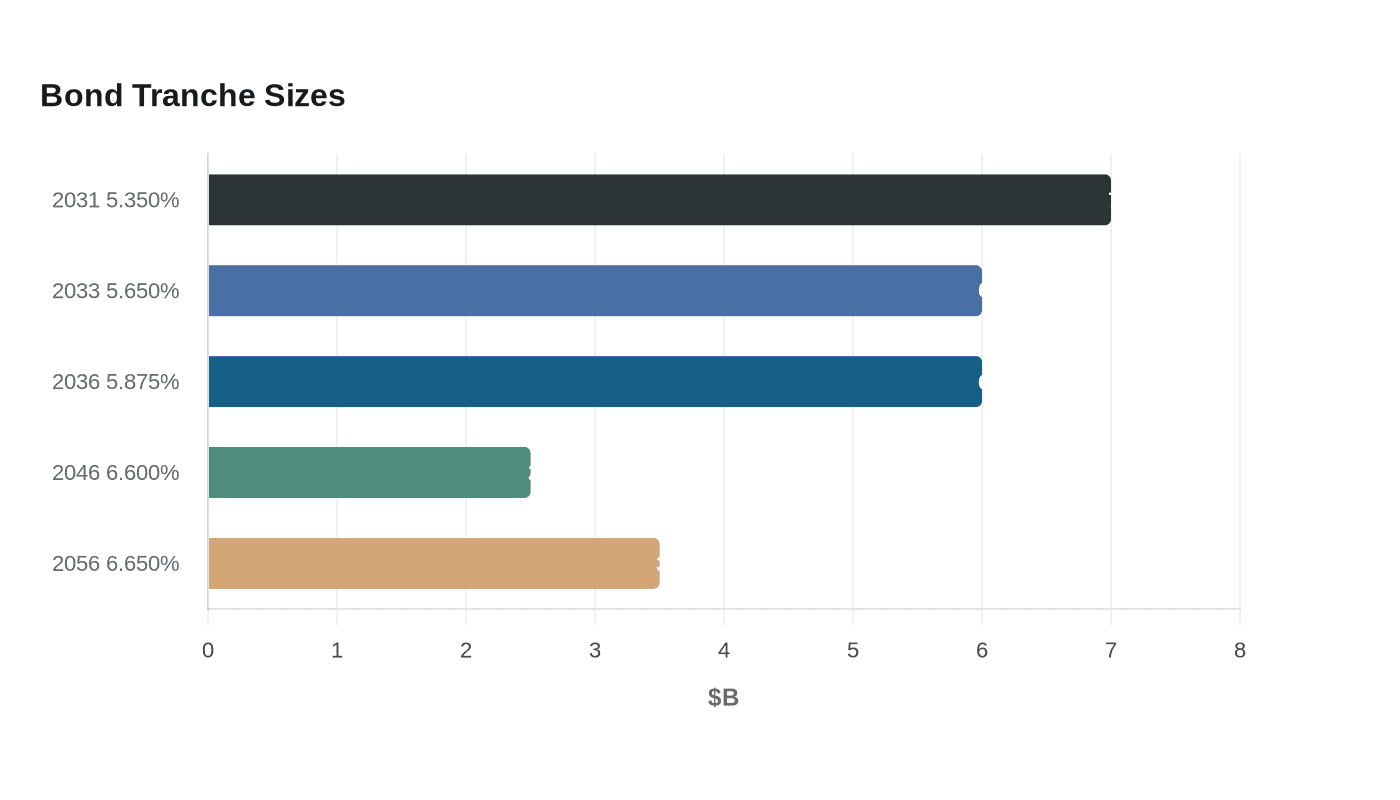

The company had initially weighed a $20 billion offering before upsizing the sale to $25 billion after demand accelerated. It divided the debt into five tranches: $7 billion of 5.350% notes due 2031, $6 billion of 5.650% notes due 2033, $6 billion of 5.875% notes due 2036, $2.5 billion of 6.600% notes due 2046 and $3.5 billion of 6.650% notes due 2056. SpaceX disclosed about $100.8 billion in cash and cash equivalents as of June 19, just before it launched the notes offering on June 22.

The bonds quickly became a test case for how much fixed-income portfolios want private-market champions once they enter public credit. SpaceX is no ordinary industrial borrower: its business depends on launch cadence, regulatory approvals, satellite services and heavy capital spending, even as it expands into the kind of rockets-to-AI story that has made it one of the most closely watched companies in the world. The company’s appeal is obvious to investors looking for a Musk-linked growth asset with scale; the risk is that scale and valuation aura can obscure how concentrated the exposure really is.

The proceeds were used to refinance costly debt tied to Musk’s acquisition of X, then Twitter, along with loans and bonds associated with xAI. That refinancing angle helped explain the speed of demand, but it did not erase the broader credit debate. Investors also appeared to make duration judgments inside the deal itself, with the shorter-dated notes drawing the strongest interest. The market reaction after pricing was less forgiving, with secondary-market weakness quickly surfacing and one estimate putting paper losses at roughly $305 million by late Thursday.

Bank of America, Citigroup, JPMorgan Chase, Goldman Sachs and Morgan Stanley managed the sale. The deal’s scale, the five-tranche structure and the rush to buy it all point to the same conclusion: private-market darlings can become mainstream credit trades fast, but popularity does not eliminate concentration risk.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?