Strait of Hormuz standoff rattles oil markets as talks stall

Hormuz carries 20 million barrels a day, and stalled U.S.-Iran talks have already pushed oil to a two-week high as shipments stayed limited.

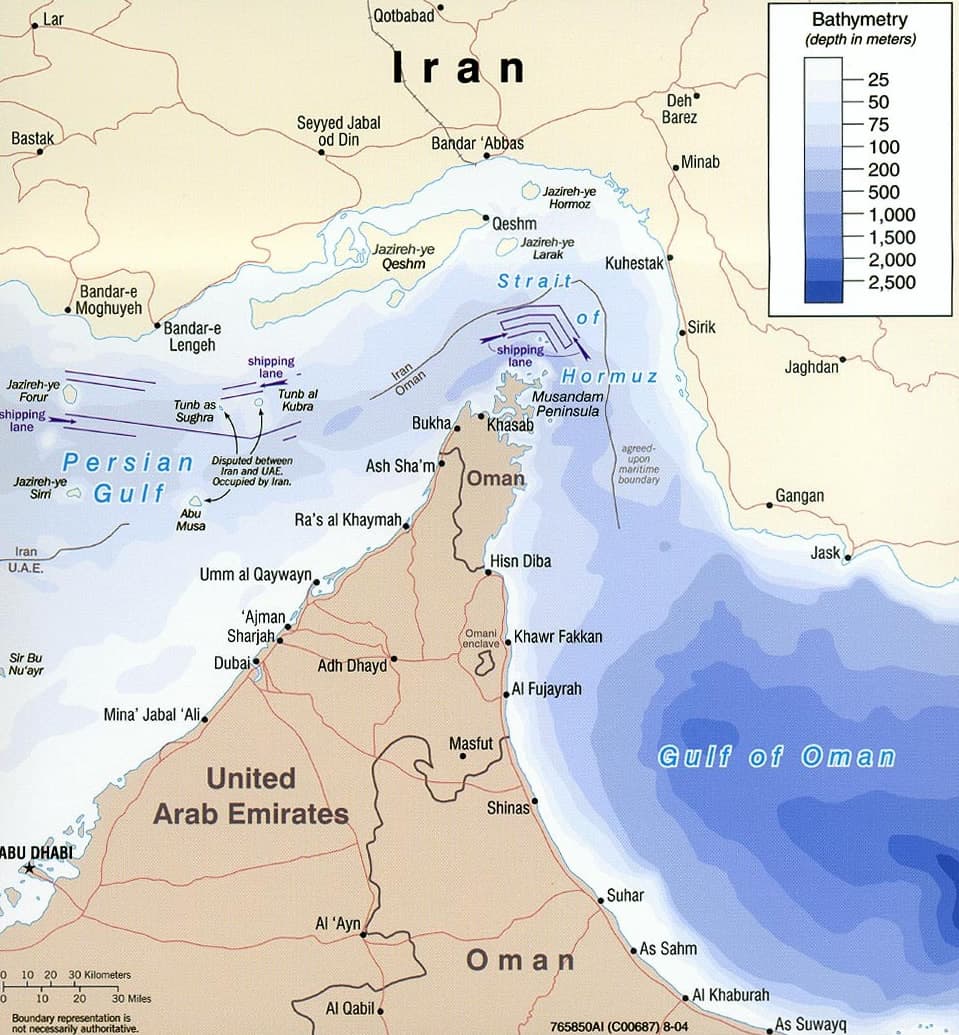

The Strait of Hormuz moves more than oil. It carries an average 20 million barrels a day of crude and petroleum products, plus about one-fifth of global liquefied natural gas trade, and its narrowest point is just 29 nautical miles across. Two 2-mile-wide shipping lanes and a 2-mile buffer leave almost no room for error if access is restricted.

That is why the current U.S.-Iran standoff has become such a dangerous bet on time. Both capitals appear to be assuming the other side will blink first, but the market is already punishing that calculation. Oil prices jumped about 3% to a two-week high on April 27 as peace talks stalled and shipments through Hormuz remained limited, then extended their rally on April 29 as reports of a U.S. blockade of Iranian ports fed expectations of longer supply disruption. Even a partial closure can do damage: it forces cargoes onto longer routes, slows deliveries and raises the cost of doing business across the entire shipping chain.

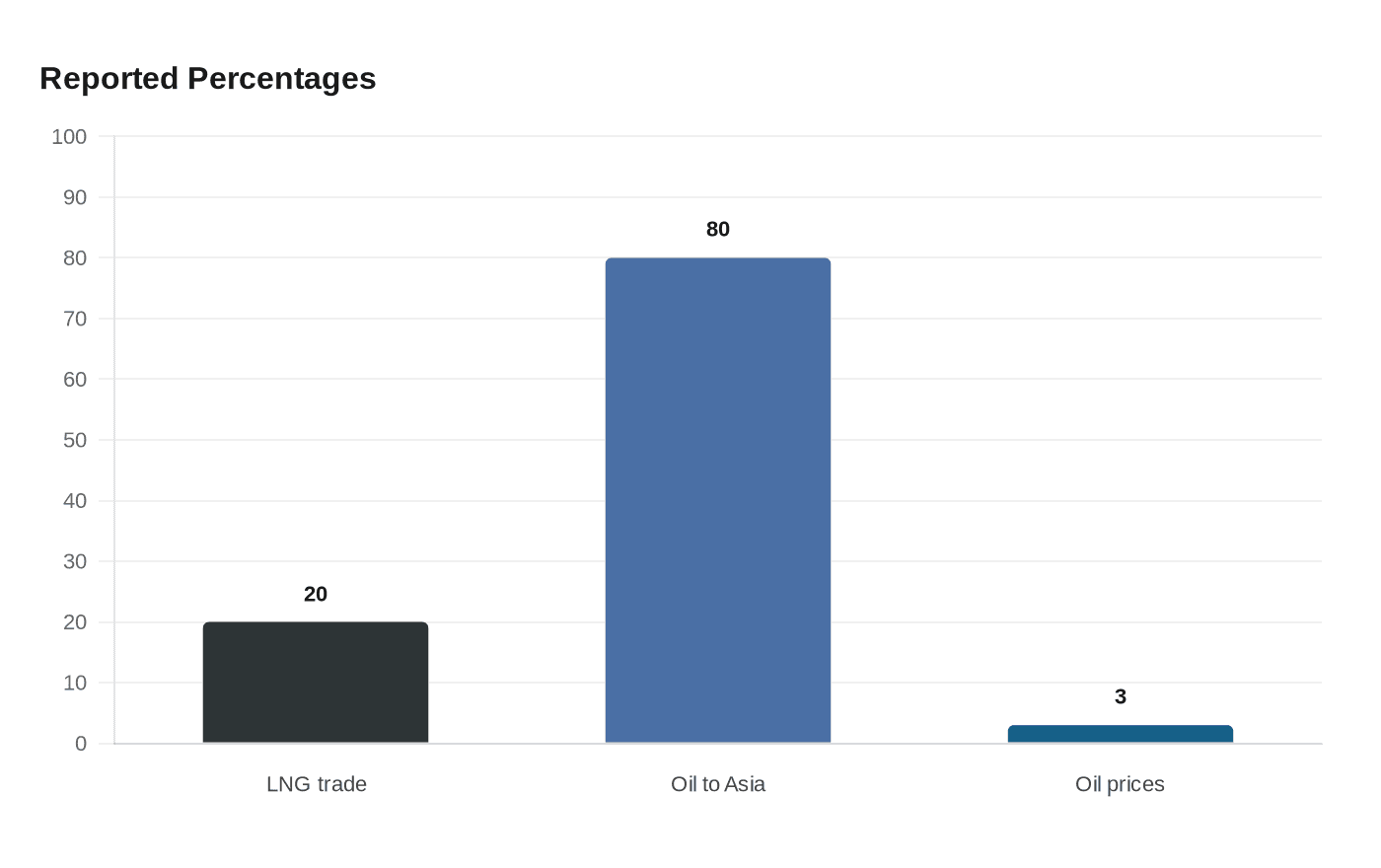

The pressure does not end when tankers start moving again. Shipping insurance could cost 20 times more than before the war even if the strait reopens, a sign that traders and underwriters may treat the risk as persistent rather than temporary. One report said liquefied natural gas transit through the strait has been effectively halted, while an Abu Dhabi National Oil Company-managed ship still managed to cross, according to maritime data from Kpler. About 80% of the oil and oil products that moved through Hormuz in 2025 were headed for Asia, which leaves importers in China, India, Japan and South Korea especially exposed to any prolonged disruption.

History suggests the stakes are larger than either side may be admitting. The Congressional Research Service says Iran’s earlier attempts to disrupt energy commerce in the Gulf brought it into direct conflict with the United States in 1987 and 1988, during the Tanker War. It also says a prolonged disruption of Middle East oil trade would create market conditions with no historical precedent. That matters because deterrence can fail when leaders believe they have more room than they really do, or when domestic politics rewards escalation over compromise.

Hormuz does not need to be fully closed to shock energy markets. If shipping insurers, refiners and tanker operators conclude the danger will last, they can keep rerouting and charging more long after any formal reopening. The deeper risk in this standoff is not just a supply hit, but a breakdown in confidence that the global oil system can absorb it.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?