Trump Accounts make it easier for parents to invest for children

Trump Accounts give children a federally backed investment start, but the biggest gains may still flow to families with cash to add. The real test is whether they widen access or deepen the advantage of households already set up to save.

Parents, guardians, and other authorized individuals can now establish a child’s Trump Account under the 2025 reconciliation law, and eligible children start with a $1,000 government deposit. That lowers one of the oldest barriers in family finance: simply getting started. It does not erase the gap between households that can keep contributing and households that cannot.

What Trump Accounts are

Trump Accounts are a new form of traditional IRA created for children. Under IRS rules, the account can be opened for a child who has not turned 18 by the end of the calendar year in which the election is made and who has a valid Social Security number. The Congressional Research Service classifies them as a children’s retirement vehicle, which places them in a different category from school-savings products and ordinary custodial accounts.

The account is meant to sit alongside other child-focused savings tools, but it is built around decades of compounding, not immediate tuition bills or a teenager’s first car.

How the money gets in

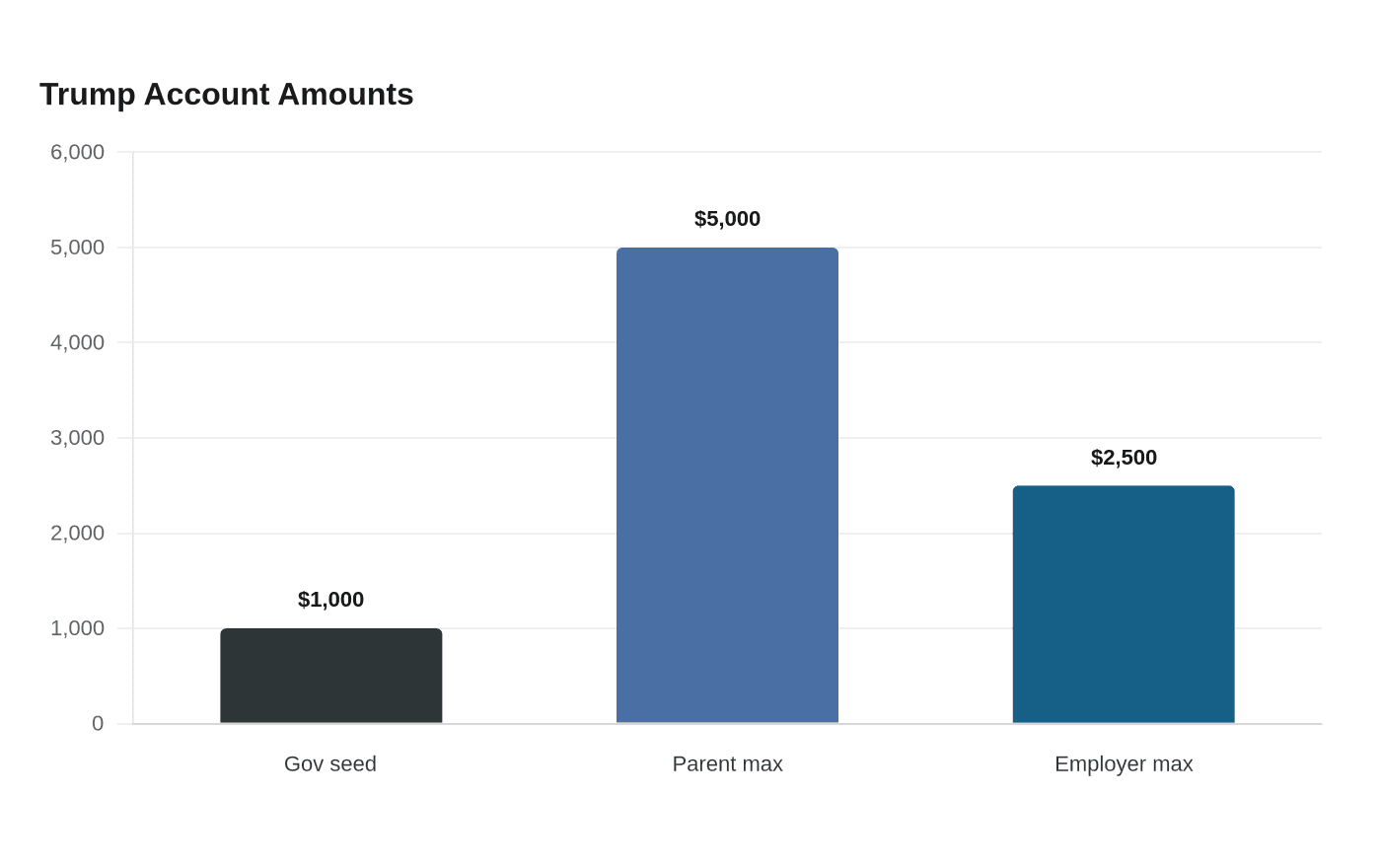

The federal pilot program supplies the first $1,000 for eligible children. Under IRS form instructions, the child generally must have been born in 2025 through 2028, be a U.S. citizen, and have a valid Social Security number to receive that pilot contribution. Treasury and IRS guidance allows parents to contribute up to $5,000 per year, while employers may contribute up to $2,500 annually without affecting the employee’s taxable income.

A family can rely on the government seed alone, but the real wealth-building power comes from continued contributions, especially when employers add money on top.

When families can use them

On March 31, 2026, the IRS said more than 4 million children had already been signed up for Trump Accounts, and more than 1 million of those children were covered by elections for the $1,000 pilot program contribution. Under Treasury and IRS guidance, savers can begin contributing to Trump Accounts starting July 4, 2026, and taxpayers can now view and submit Trump Account elections in their individual IRS accounts.

Who is most likely to benefit

The inequality question sits at the center of the Trump Account debate. The account’s government seed gives every eligible child a starting point, but the largest gains will go to families able to add their own money year after year. A household that can contribute the full $5,000 annually, especially if an employer also adds up to $2,500, will build a much larger balance than a household that can only rely on the initial $1,000.

Financial literacy also shapes outcomes. Families that understand compounding, investment options, and account rules are better positioned to use the structure well, while families with less time or fewer financial resources may open the account but leave much of its potential unused.

How they compare with older child-saving tools

Early investing for a child’s future can maximize long-term growth potential, and that principle applies here as well. FINRA points to 529 plans as a key option for education savings, with contribution and withdrawal rules that vary by plan. UGMA and UTMA custodial accounts remain another established way to transfer assets to minors without creating a trust.

Those alternatives serve different goals. A 529 is built around education, and custodial accounts can be more flexible, but both have long been used by families already familiar with investment products. Trump Accounts broaden the menu by creating a retirement-style option specifically for children, with a federal seed deposit and employer participation built into the structure.

What the policy change means in practice

Trump Accounts reduce the friction of starting early. A child can receive an initial government-funded deposit, and families can add money through payroll or direct contributions without needing to build a separate trust or navigate a more complicated legal setup.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?