UK gilt yields surge as investors fear political turmoil

Britain’s 30-year gilt yield hit its highest since 1998, reviving fears that bond traders can still overrule ministers on taxes and spending.

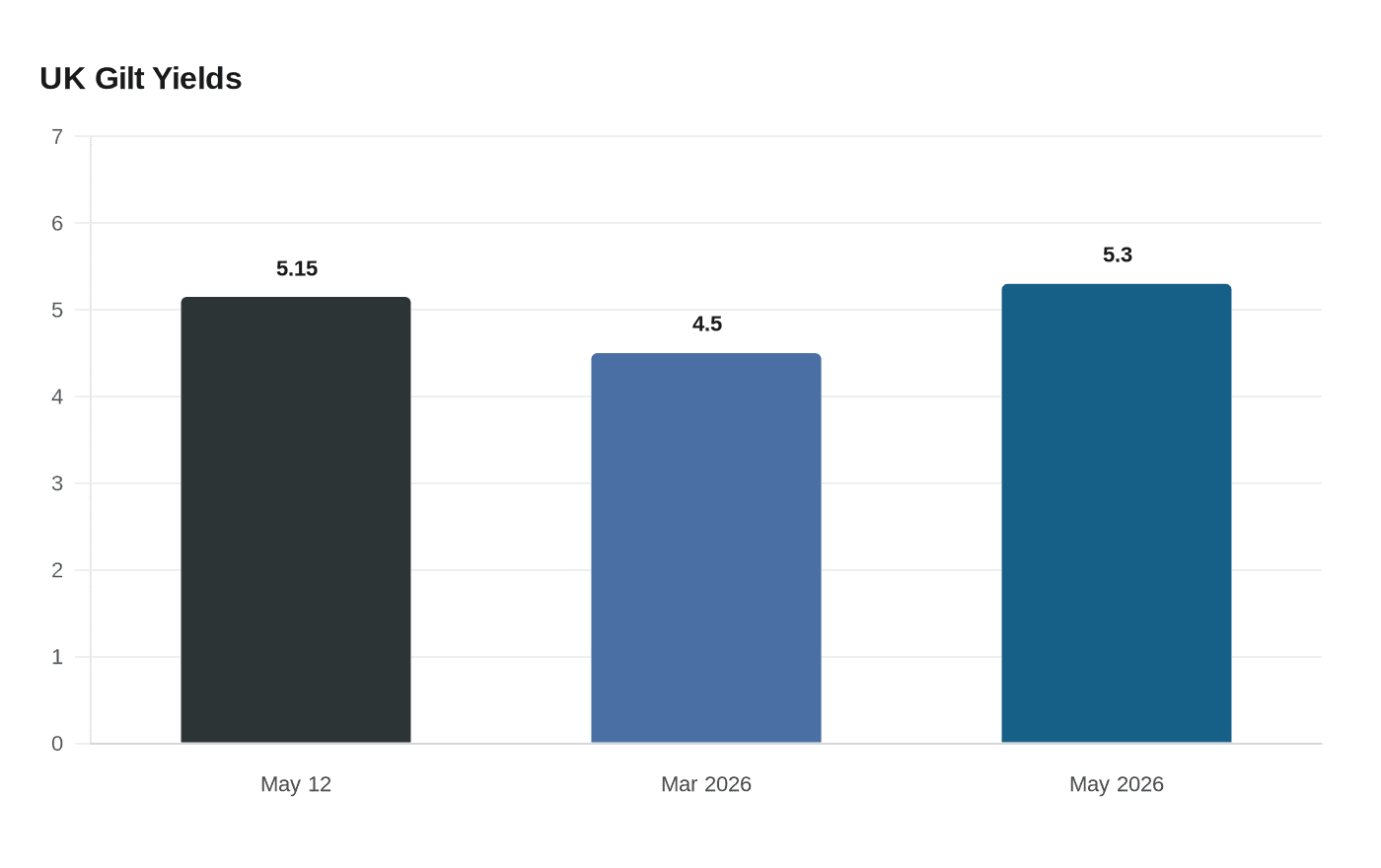

Britain’s bond market is once again acting like a political referee. The 30-year gilt yield climbed to its highest level since 1998 in May 2026, while the benchmark 10-year gilt was around 5.15% on May 12 before easing slightly, a move that reflected investor nerves about political instability and the possibility of weaker fiscal discipline.

Those fears matter because higher gilt yields are not an abstract trading story. They raise the government’s debt-interest bill, narrow the room Rachel Reeves has to manoeuvre on tax and spending, and can feed through to mortgages, business borrowing and sterling. When long-term borrowing costs rise, every promise about growth, public services or tax relief becomes more expensive to keep.

The latest pressure comes against a backdrop that is not one of fiscal collapse, but of fragile credibility. The Office for National Statistics said UK public sector net borrowing in the financial year ending March 2026 was initially estimated at £132.0 billion, equal to 4.3% of GDP. That was £0.7 billion below the Office for Budget Responsibility’s forecast and the lowest share of GDP since the financial year ending March 2020.

Even so, markets are trading the politics, not just the arithmetic. The OBR’s March 2026 Economic and Fiscal Outlook assumed a 10-year gilt yield of 4.5% and a 30-year yield of 5.3% in its forecast window, with borrowing expected to fall over the forecast horizon. The government’s Spring Forecast said borrowing had dropped by nearly £18 billion compared with autumn, that this year’s total was set to be the lowest in six years, and that borrowing had fallen below the G7 average for the first time in 22 years.

The Bank of England is adding to the supply of gilts that investors must absorb. In September 2025, the Monetary Policy Committee voted to reduce the stock of gilts held in the Asset Purchase Facility by £70 billion over the 12 months from October 2025 to September 2026. The Bank confirmed in May 2026 that it was proceeding with those sales, meaning the market has to take in both fresh government issuance and central bank disposals at the same time.

That is why Britain keeps being compared with the 2022 mini-budget under Liz Truss and Kwasi Kwarteng, when gilt yields spiked, sterling fell and the Bank of England was forced into temporary gilt purchases to steady pension funds and the wider market. The National Institute of Economic and Social Research says the central 2026 outlook is still for yields to decline gradually, but warns that a sharp jolt remains possible if volatility in US Treasuries spills into Britain. For Keir Starmer and Reeves, the message from bond traders is blunt: political turmoil has a price, and the bond market will keep setting it.

Know something we missed? Have a correction or additional information?

Submit a Tip