UnitedHealth raises profit forecast as medical costs stay controlled

UnitedHealth lifted 2026 profit guidance to as much as $20 a share as Optum and tighter medical-cost control eased investor nerves, sending the stock up more than 10%.

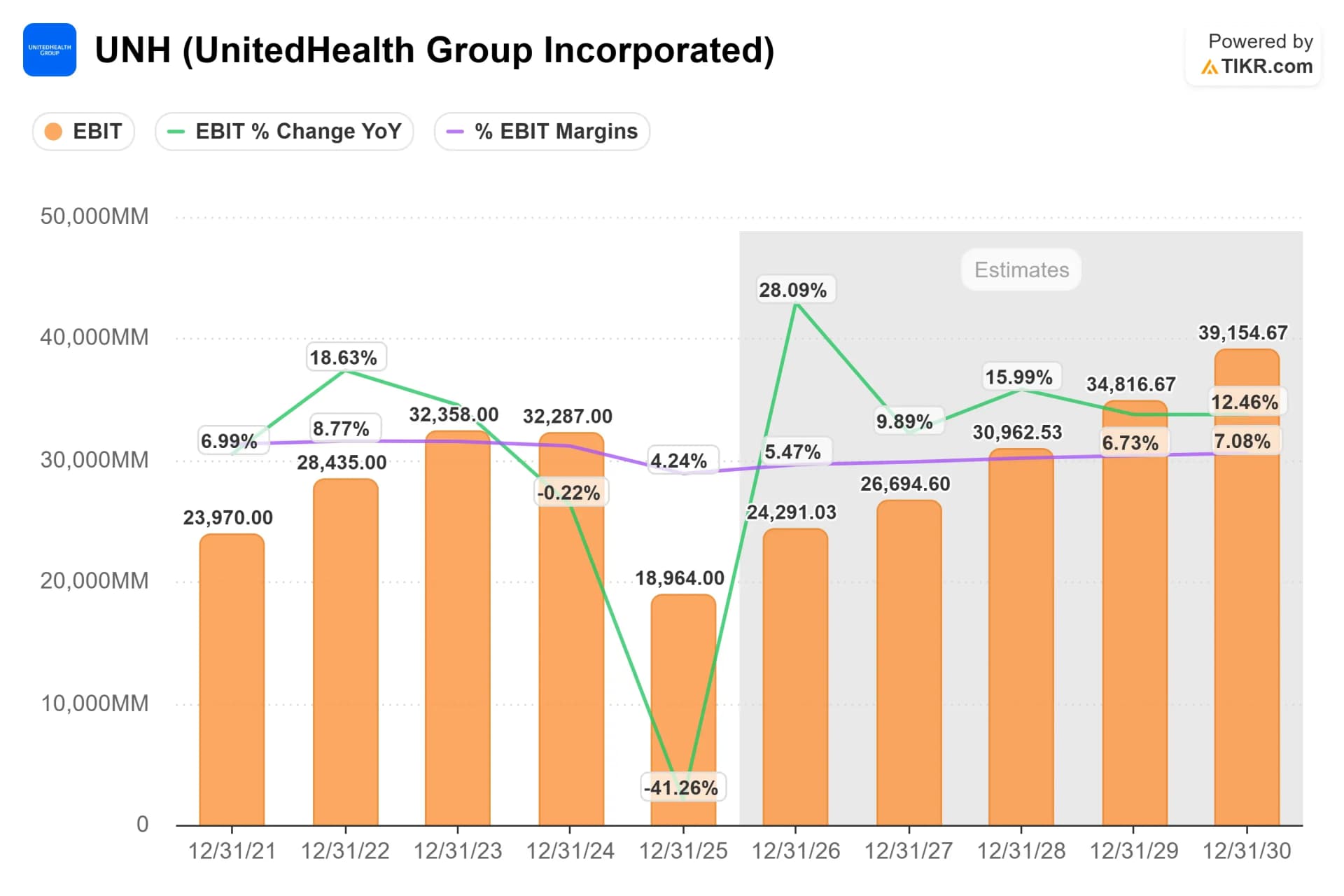

UnitedHealth Group lifted its full-year 2026 adjusted profit outlook to $19.50 to $20.00 per share on July 16, a sign that the nation’s largest private insurer sees medical spending staying contained even as it pays claims across a vast membership base. The revised range came in above the roughly $18.47 per share analysts had expected and helped send the stock up more than 10%.

The forecast raise goes straight to the central question in health insurance: is UnitedHealth truly controlling costs, or is it merely absorbing pressure in ways that still leave employers and patients exposed to higher premiums and tougher access? In managed care, guidance matters because it reveals whether claims costs and utilization are tracking inside the company’s plan or threatening margins. UnitedHealth’s new outlook says management sees enough stability in medical expense trends to improve earnings rather than brace for a cost spike.

Second-quarter 2026 adjusted earnings came in at $6.38 per share, a result that supported the stronger outlook and reinforced Wall Street’s focus on how the company is balancing premiums collected against medical claims paid. UnitedHealth said the increase reflected performance year to date and expectations for continued improvement, with tighter management of medical costs and better operating income in Optum helping drive the revision. Optum, the company’s health services arm, has become a key lever in UnitedHealth’s financial performance and a major reason investors watch the group’s margins so closely.

The new outlook also marks a notable step up from the 2026 guidance UnitedHealth issued on Jan. 27, after it reported full-year 2025 revenue of $447.6 billion, adjusted earnings of $16.35 per share and earnings of $13.23 per share. The company’s investor relations calendar listed July 16 as the date of its second-quarter update, making the release the main moment for assessing whether utilization and medical-cost pressures were easing or merely being managed quarter by quarter.

For the broader health-care economy, the message is mixed but important. A stronger forecast suggests UnitedHealth is seeing steady demand for care without an abrupt jump in cost trends, which can reassure investors after a stretch of concern about insurance margins. It does not erase the pressure facing the system, where premium growth, provider negotiations and patient utilization still determine whether insurers can keep profits expanding without pushing more of the burden onto customers.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?