Warsh Revives Fed Debate Over Which Inflation Measure to Trust

Kevin Warsh is forcing the Fed’s inflation debate back to basics: the measure it trusts most still runs above target, while other gauges point lower or higher.

Kevin Warsh has reopened a fight at the Federal Reserve over a question with immediate stakes for borrowers and investors: which inflation measure should guide interest-rate decisions when the readings do not line up.

The central bank says its longer-run objective is 2% inflation as measured by the annual change in the personal consumption expenditures price index, or PCE, the monthly gauge published by the Bureau of Economic Analysis. Fed officials favor that measure because they say it best fits their mandate for maximum employment and price stability. Its core version strips out food and energy to show the underlying trend, and it is the figure policymakers watch most closely when judging whether inflation is truly easing.

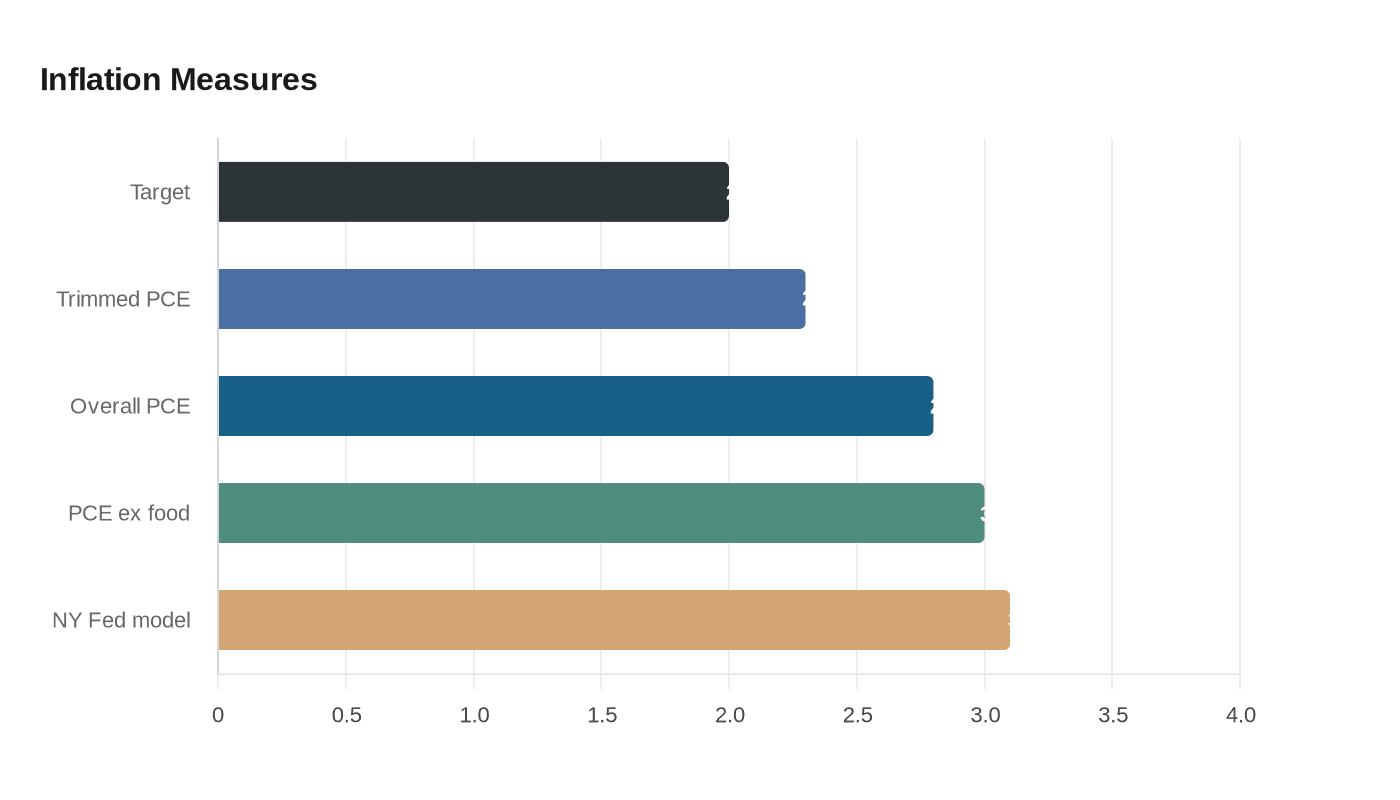

The problem is that the inflation landscape looks different depending on which yardstick is used. The Dallas Fed said its trimmed-mean PCE inflation rate for the 12 months ending in February 2026 was 2.3%, while overall PCE inflation was 2.8% and PCE excluding food and energy was 3.0%. A Cleveland Fed median-price measure was closer to headline inflation, while a New York Fed model pointed to a hotter underlying pace of about 3.1%. That spread helps explain why some analysts say there is no single clean read on price pressures.

Warsh, testifying before the Senate Banking Committee on April 21 during his confirmation hearing, pushed that uncertainty back into the spotlight. Reuters reported that he favored using “trimmed averages” and wanted a broader overhaul of how the Fed measures inflation, while giving few details on the near-term path for rates. His argument goes beyond statistical housekeeping. If policymakers misread the data, they can tighten too much, slow hiring and credit growth, or ease too soon and risk reigniting inflation.

The Fed itself has acknowledged that inflation policy depends not only on the current reading but on expectations. Its 2025 strategy statement said well-anchored longer-term inflation expectations at 2% support price stability and moderate long-term interest rates. That matters because the credibility of the target affects everything from mortgage pricing to credit-card debt costs and the room the central bank has to cut rates if the economy weakens.

The last formal rate decision before Warsh’s hearing came on December 10, 2025, when the Federal Open Market Committee lowered the federal funds rate target range to 3.5% to 3.75% and said it would carefully assess incoming data, the evolving outlook and the balance of risks. Warsh’s challenge is that the data itself is part of the risk, and the Fed’s next move will depend as much on which inflation story it believes as on the target it is trying to hit.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?