Applied Systems says Canadian personal auto rates climb 11.1% in Q1 2026

Canadian personal auto rates rose 11.1% in Q1, even as auto pricing cooled quarter over quarter and provinces split sharply.

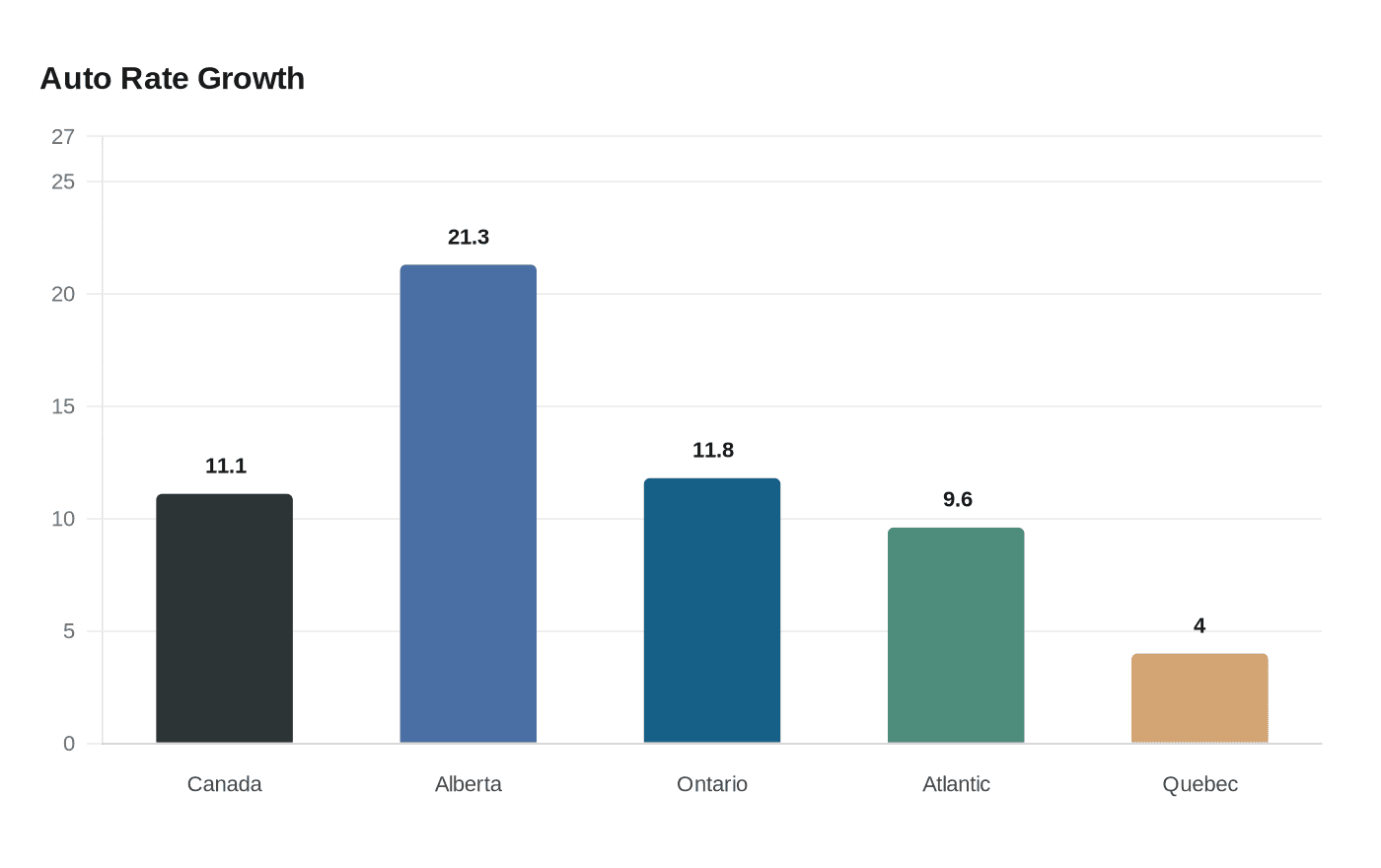

Canadian personal auto pricing kept climbing, but the pace started to soften. Applied Systems said its Applied Rating Index showed personal auto premiums up 11.1% year over year in Q1 2026, while personal property premiums rose 8.6%, a reminder that personal lines remain under pressure even as some quarterly moves begin to moderate.

The quarterly benchmark, published May 5 from Toronto, Ontario, is built from rates generated in Applied Rating Services and is designed to track personal auto and personal property pricing across provinces. Applied’s own framing matters here: this is not just a market temperature check, it is a tool for spotting where competitive rates and renewal opportunities are shifting before those changes show up in a carrier’s book.

Alberta again stood apart. Personal auto rates in the province rose 21.3% year over year, and personal property climbed 16.2%, the highest increases in the country. Quebec posted the slowest personal auto gain at 4.0%, while British Columbia and Quebec had the lightest property increases at 1.6% and 4.0%. Nationally, personal auto rates fell 0.8% quarter over quarter versus Q4 2025, while personal property rose 2.4%.

That provincial split is the part carriers, brokers, and rating teams should care about most. Applied said auto rates fell quarter over quarter in every province except Alberta, while property rates rose in every province except British Columbia and Quebec. Ontario’s personal auto rates were up 11.8% year over year, the Atlantic provinces were up 9.6%, and Quebec’s auto gain was 4.0%. On the property side, Saskatchewan and Manitoba rose 11.2%, the Atlantic provinces 10.8%, Ontario 6.2%, Quebec 4.0%, British Columbia 1.6%, and Alberta 16.2%.

Steve Whitelaw, senior vice president and general manager of Applied Systems Canada, said the Q1 2026 results showed a growing divergence across provinces and said Alberta continued to lead rate increases while moderation was emerging in Quebec. That split is where benchmarking earns its keep: carriers can tighten pricing strategy in provinces with hotter inflation, brokers can calibrate renewal conversations with more precision, and rating platforms can surface where quoting pressure is easing before it becomes obvious in loss ratios.

The catch is that a quarterly benchmark is still a rearview mirror, not a live steering wheel. Severe weather and rising claims costs continued to shape the market, and 2025 insured losses from severe weather exceeded C$2.4 billion, according to CatIQ and the Insurance Bureau of Canada. With Alberta’s Care-First auto reforms scheduled for January 1, 2027, the provincial picture will keep shifting. Applied’s Q4 2025 index had already shown personal auto up 14.4% year over year and personal property up 7.8%, so Q1 2026 looked more like a slowing climb than a clean turn.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?