Circana report shows protein brands gaining share in tough market

Private label and smaller protein brands took share in 2025 as Circana tracked a 3% rise in food and beverage sales and sharp gains in yogurt, cottage cheese and energy drinks.

Protein brands are still finding ways to grow, but the path is narrower and more competitive than it was a year ago. Circana’s 14th annual U.S. CPG Growth Leaders report, released April 9, analyzed more than 700 manufacturers and showed retail food and beverage sales rising 3% in 2025, while non-food sales slowed to 2%. It was also the first time Circana compared public and private CPG performance in the same ranking, a sign of how much the market has shifted toward value, scale and sharper execution.

The biggest message for protein is that demand is not the problem. The market is, increasingly, a fight over share. Private label reached $330 billion in U.S. sales in 2025 and held 24% of retail food and beverage dollar share, up 0.4 percentage points from the prior year. The club channel accounted for 47% of all private-brand growth, while mass and grocery added 25% and 21%. That matters because protein has become a mainstream value cue, not just a sports-nutrition label, with private brands increasingly tied to claims like protein and low sugar.

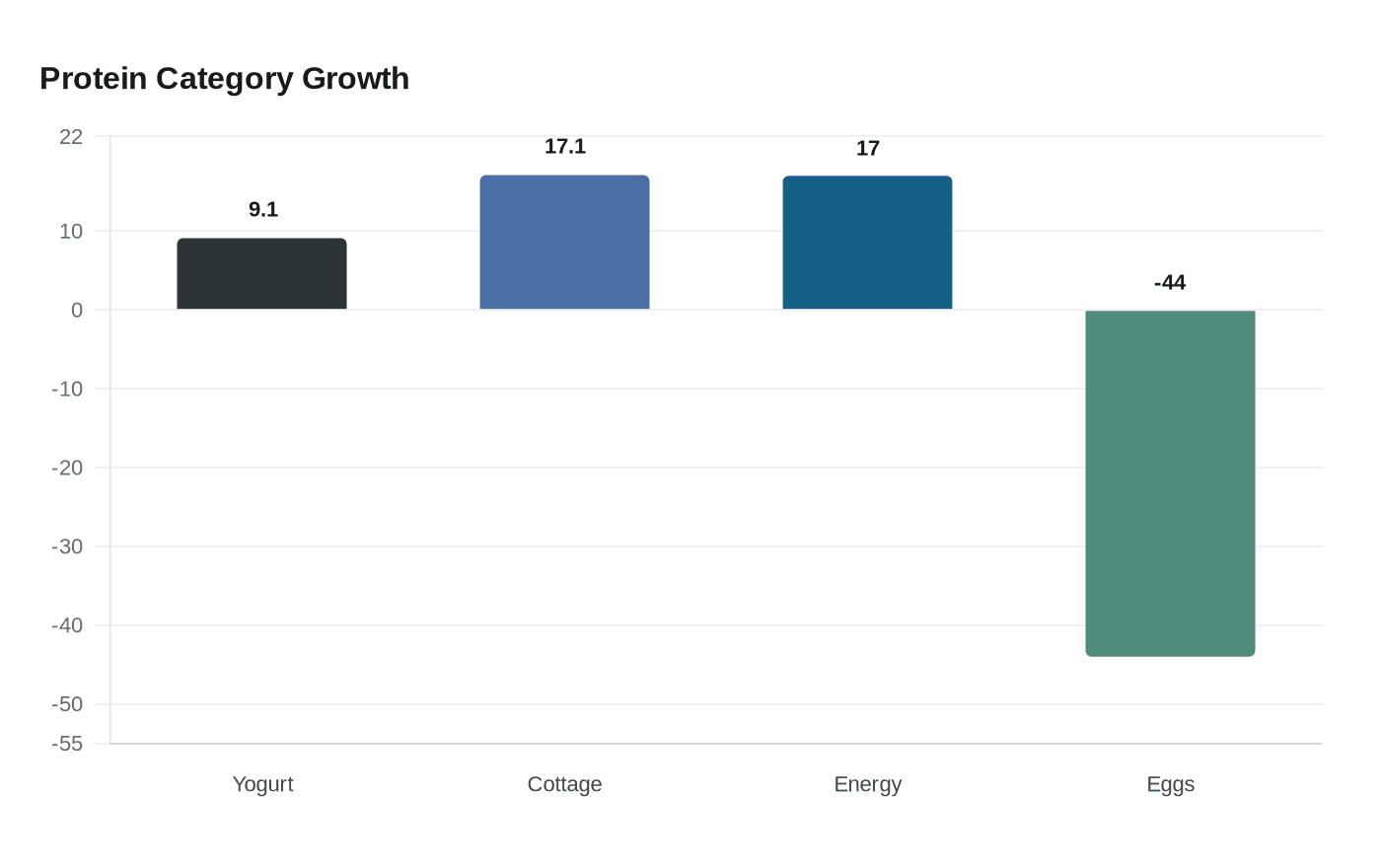

The growth is showing up across more than one aisle. Circana’s center-store and frozen-foods data showed yogurt sales up 9.1%, cottage cheese up 17.1% and energy drinks up 17.0%, while fresh eggs fell 44.0% in the same ranking. That spread says protein is not living in one refrigerated bunker anymore. It is moving through center store, frozen and fresh, wherever shoppers are chasing satiety, convenience and a functional boost without paying for excess.

The standout brands also point to the playbook. Chobani, Celsius and BellRing Brands were among the top performers in Circana’s $2.5 billion to $8 billion revenue tier, while Red Bull North America, Unilever, Kimberly-Clark, L’Oreal and The Coca-Cola Company led the $8 billion-plus group. Circana also highlighted Premier Protein and Chomps in a March 2026 webinar, saying both brands expanded distribution, navigated supply challenges and used innovation to win new consumers. That is the difference between a hot product and a durable protein business: shelf presence, velocity and enough retail visibility to keep turning over.

The winners were not just raising prices and hoping shoppers stayed loyal. They were working price-pack architecture, adding smaller packs for affordability and larger value packs for household stocking. They were combining trust, value, relevance, innovation, competitive pricing and distribution. Sally Lyons Wyatt has said growth leaders were expanding reach as much as they were expanding margins, and the data backs that up. For protein brands trying to keep gaining share, the formula is becoming clearer: build around consumer-perceived value, keep the brand visible, and make sure the product fits the shopping mission at the right price.

Know something we missed? Have a correction or additional information?

Submit a Tip