Whey Emerges as Profit Driver, Reshaping Dairy Pricing and Investment

Whey is no longer a leftover stream. Protein demand has turned it into a pricing lever that now shapes milk values, plant investment, and export strategy.

Whey is now part of the milk price, not just a byproduct of it

Whey is no longer the scrap left after cheese making. It has become one of the clearest signals of how protein demand is rewriting dairy economics, from the farm gate to the finished product aisle. What used to be a secondary stream now carries strategic weight because whey protein isolates and concentrates command attention, and money, in a market that wants more protein per serving.

That shift matters because whey is influencing more than ingredient pricing. It is changing how processors think about product mix, how they allocate capacity, and how they judge where the next dollar of capital should go. In practical terms, the value attached to protein-rich dairy streams is starting to pull milk economics in new directions.

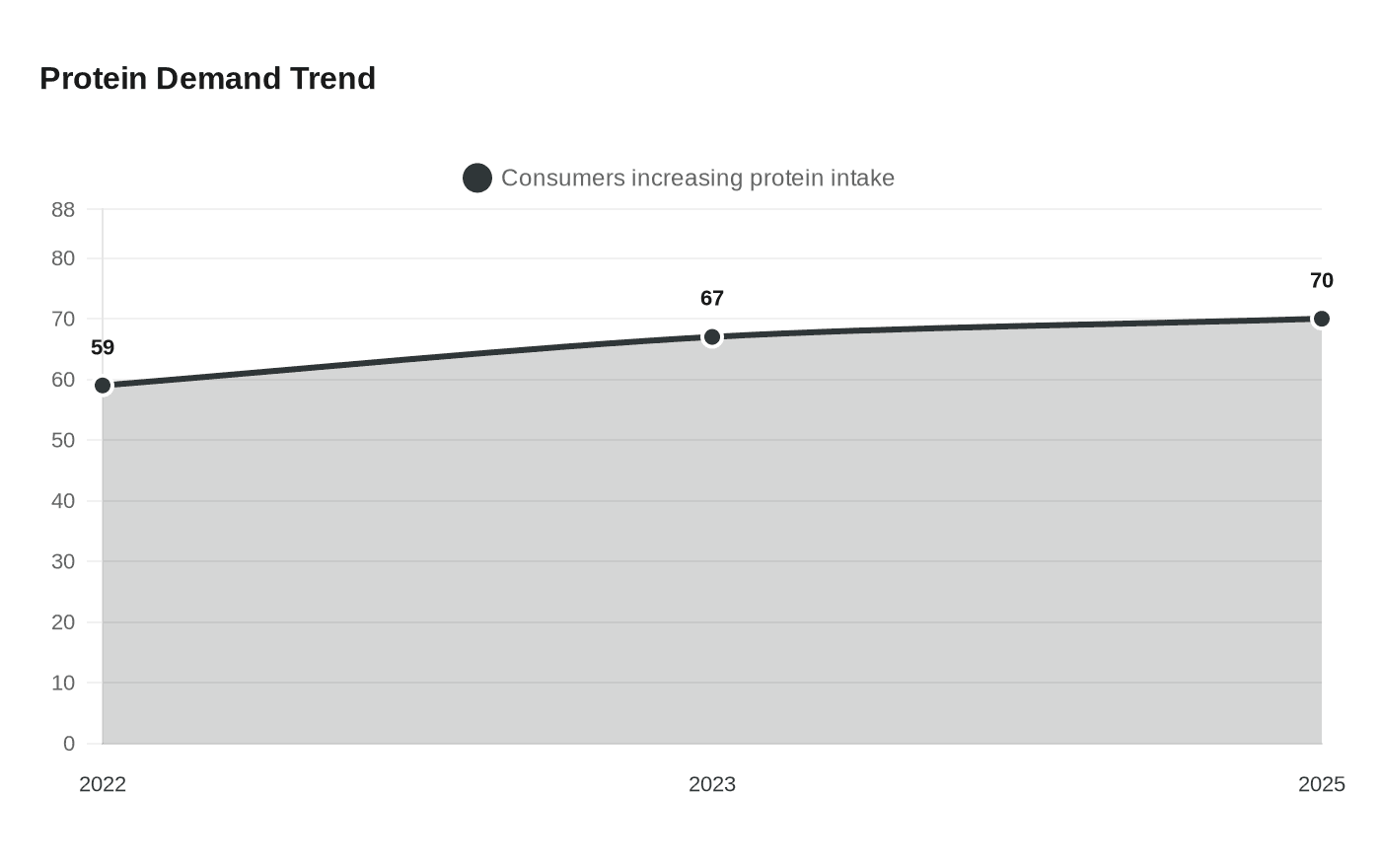

Consumer protein demand is the engine behind the change

CoBank, citing the International Food Information Council, said 70% of American consumers reported trying to increase protein intake in 2025, up from 67% in 2023 and 59% in 2022. That is not a minor preference swing. It is a sustained demand signal that helps explain why whey, especially higher-value forms like WPI and WPC, has moved to the center of dairy strategy.

CoBank also said high-protein claims on food and beverage products can command a price premium of as much as 12%. That premium changes the math for brands and processors alike. If a higher-protein formulation can lift shelf price, then the ingredient mix, the sourcing plan, and the processing line all start to matter more, because they determine whether that premium survives the cost of doing business.

For product developers, the takeaway is simple: whey is not just a functional ingredient anymore. It is a margin ingredient. If a formulation depends on whey for texture, solubility, or a protein claim, then ingredient cost swings can quickly turn into a packaging, labeling, and pricing problem.

The market is being priced like a core commodity

The whey story is easiest to understand when you look at the USDA data series built around it. The National Dairy Products Sales Report tracks weekly prices for butter, cheddar cheese, dry whey and nonfat dry milk, which puts whey in the same pricing frame as the staples that anchor dairy economics. USDA’s monthly Dairy Products report adds production, stocks, and shipments for dry whey and modified whey, giving the market a fuller picture of supply flow and inventory pressure.

That reporting structure matters because it shows whey is not an afterthought in the data. It is monitored like a core market, and that is exactly how processors now treat it. The National Agricultural Library Economics, Statistics, and Market Information System, along with USDA’s NASS Dairy Products reports, gives the industry the official numbers that help turn whey from a byproduct into a price-bearing category.

The result is a different pricing logic across the supply chain. If whey prices rise, the value of the milk stream changes. If a plant can extract more value from whey components, it may choose one product mix over another. That is why whey now affects not only what gets made, but what gets prioritized.

Exports are the pressure valve, and sometimes the accelerant

StoneX reported in January 2025 that U.S. dry whey and whey protein isolate prices had moved sharply higher, with WPI breaking records. That is the kind of move that gets processors’ attention fast, because the U.S. market is not isolated. StoneX also noted that anywhere from 25% to 85% of U.S. whey is exported, which means global supply and demand shifts can quickly feed back into domestic pricing.

ThinkUSADairy said the United States was the leading single-country producer and exporter of whey ingredients, with total U.S. whey exports reaching 564,000 metric tons in 2023. It also said combined U.S. production of WPC and WPI rose 5% versus 2019 to 292,000 metric tons in 2023, which accounted for about 41% of total whey production excluding permeate. Those numbers show how deeply the U.S. industry is tied to higher-value whey categories rather than just bulk dry whey.

That export channel acts like a pressure valve for domestic production, but it can also tighten the market when overseas demand gets stronger. In a commodity with that much export exposure, a pricing rally in one region can show up quickly in the United States.

China is pushing the market toward premium protein

USDA Foreign Agricultural Service said demand for high-protein whey in Asia is most visible in China, where U.S. WPC80+ exports more than doubled year over year from January through October 2023 to 2024. Over the same period, other U.S. whey products declined by 2%, which is a sharp signal that buyers are moving up the value chain rather than simply taking more volume.

The FAS also said Chinese manufacturers were pushing for product differentiation and premiumization. That matters because it changes what processors want to make. If the strongest demand is for more specialized, higher-protein ingredients, then the industry is nudged toward the equipment, filtration, and packaging needed to serve that market.

This is also where whey stops looking like a side story and starts looking like a strategic commodity. When export demand favors premium protein formats, the pricing logic shifts away from volume alone and toward composition, purity, and performance.

Capital is following the protein premium

Once a commodity begins to earn a premium, investment follows. Wisconsin dairy processors had $151 million earmarked for whey and dairy ingredients facilities within a broader $1.13 billion wave of new capacity projects scheduled for 2025 through 2028, according to IDFA reporting. That is not speculative money. It is a concrete sign that processors expect the protein market to keep rewarding capacity built for whey ingredients.

FrieslandCampina Ingredients reinforced that point when it said its acquisition of Wisconsin Whey Protein was part of a broader strategy to lead the global protein market and expand WPI capacity. That is a clear example of how the capital story and the pricing story have merged. Companies are not just reacting to whey prices, they are building around them.

The historical comparison is hard to miss. Whey has gone from an often-undervalued cheese byproduct to a globally traded ingredient with record pricing, export pull, and direct influence on plant investment decisions. Protein demand has not merely lifted one niche ingredient. It has changed the economics of milk itself, and the processors who understand that shift are already planning differently.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?