Big Lots workers could boost savings with expanded HSA rules

Big Lots workers can carry HSA money from job to job while 2026 limits raise the ceiling to $4,400 for self-only coverage. The catch is simple: you need an HSA-eligible high-deductible plan first.

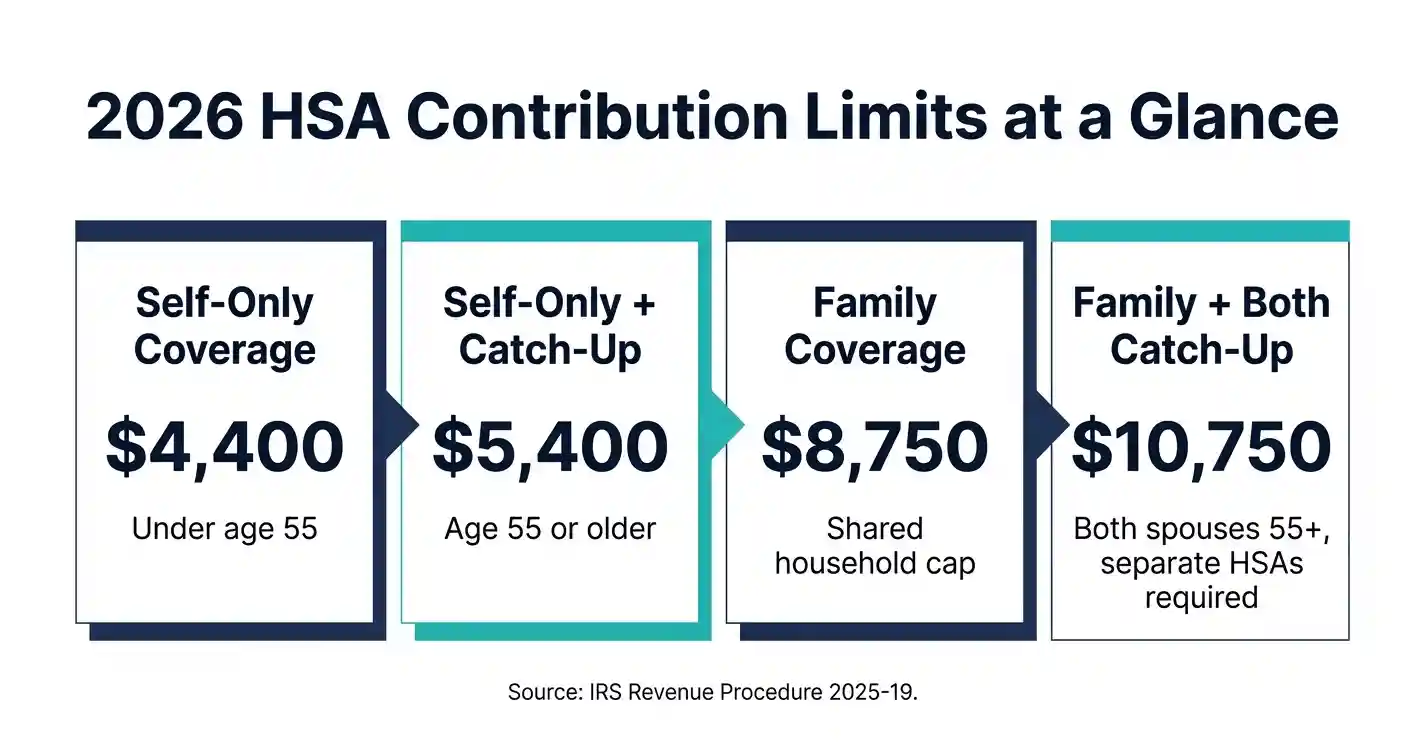

The IRS set 2026 HSA contribution limits at $4,400 for self-only coverage and $8,750 for family coverage. For Big Lots workers, portability matters because store schedules, job status, and even employers can change fast, but the account stays with the worker instead of disappearing with the job.

What changed for 2026

The One, Big, Beautiful Bill Act, signed on July 4, 2025, expanded HSA availability under section 223, and IRS Notice 2026-05 translated that change into the numbers people use during open enrollment. Telehealth and other remote-care coverage can be disregarded for HSA eligibility for plan years beginning after 2024, so virtual visits do not knock a qualifying HDHP out of HSA status by themselves. For calendar year 2026, the HDHP floor is a minimum deductible of $1,700 for self-only coverage and $3,400 for family coverage, with annual out-of-pocket ceilings of $8,500 and $17,000.

Who can actually contribute

An HSA is a tax-exempt trust or custodial account set up with a qualified HSA trustee, and only an eligible individual can contribute. Month by month, that means you must be covered by an HDHP on the first day of the month, have no other disqualifying health coverage, not be enrolled in Medicare, and not be claimable as someone else’s dependent. If you have a plan that looks cheap on the premium side but does not meet the HDHP rules, it may not open the HSA door at all.

What the 2026 limits mean in paycheck terms

If your contributions come out biweekly, maxing a self-only HSA means roughly $169.23 per paycheck, while family coverage means about $336.54 per paycheck; workers 55 and older can add another $38.46 per check through the catch-up contribution. On weekly payroll, those figures are about $84.62, $168.27, and $19.23. These amounts reset each year through annual revenue procedures and Internal Revenue Bulletin notices instead of staying fixed.

Why portability is the retail advantage

The HSA is owned by the individual, and if that person changes employers or leaves the workforce, the account stays with them rather than with the old job. That makes it different from benefits that reset with each employer decision or each enrollment cycle. If you move from one Big Lots store to another company, or even from part-time hours to full-time work, the HSA balance does not need to start over.

The Big Lots comparison trap

The most likely mistake when comparing Big Lots health-plan options is assuming that any plan with telehealth or remote-care coverage is disqualified, or that a lower premium automatically means better savings. Telehealth and other remote-care services can be disregarded coverage, but the plan still has to meet the HDHP deductible and out-of-pocket thresholds to allow HSA contributions.

How to use the account without losing the tax break

The safest way to use an HSA is to verify the plan first, then set the payroll amount to match your contribution target, then keep records of qualified medical spending. The money can be used tax-free for qualified medical expenses, and workers often treat the account as a mix of health emergency fund, tax shelter, and longer-term savings tool.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?