IRS rollover rules could help Big Lots workers protect 401(k)s

Big Lots workers can avoid taxes and penalties if they move a 401(k) the right way, but the 60-day clock and withholding rules can turn a simple rollover into a trap.

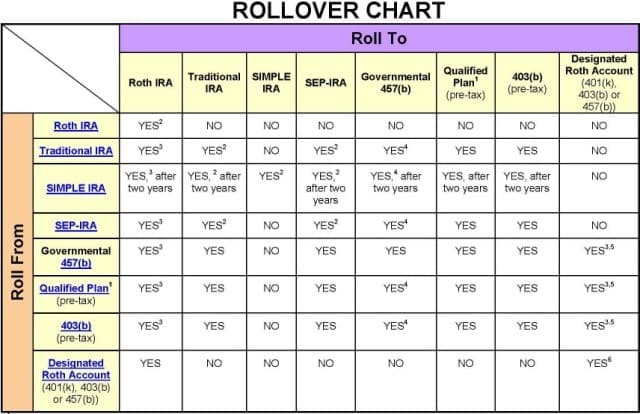

A former Big Lots worker who receives a 401(k) distribution generally has 60 days to roll it into another eligible retirement plan or IRA. If the transfer is handled correctly, it is generally not taxable, even though it still has to be reported on a federal tax return.

Start with the decision, not the deadline

For anyone leaving Big Lots, the first question is not whether the money exists but where it should go next. You can usually leave the account where it is, move it into a new employer’s plan, or send it to an IRA. Cashing out is the option with the most immediate sting: it can trigger taxes, and it can also wipe out years of compounding growth that would otherwise keep working for you.

That choice matters even more during a company breakup, when paychecks, benefits portals and plan paperwork can all become harder to track. Big Lots and its subsidiaries filed voluntary Chapter 11 cases in Delaware bankruptcy court on September 9, 2024, after entering a sale agreement with an affiliate of Nexus Capital Management LP. Court documents list about 9,600 full-time employees and about 18,100 part-time employees, along with about 1,300 stores across 48 states and about $556 million in long-term debt.

Why a direct rollover is usually the cleanest move

Direct rollovers, sometimes called trustee-to-trustee transfers, avoid withholding from the transfer amount. That is the easiest path if you are trying to protect every dollar, because the money moves straight from one retirement account to another instead of bouncing through your bank account first.

The alternative is messier. If a retirement-plan distribution is paid directly to you, the 60-day clock starts on the date you receive it, and you generally must roll it over into another eligible retirement plan or IRA within that window. If taxes are withheld from the distribution, you may need to replace that withheld amount from another source to complete a full rollover. A check that looks like the full balance may not be the full balance once withholding comes out.

The 60-day rollover deadline can be waived in some circumstances beyond the participant’s control, but that is not a safety net to count on.

The paperwork that keeps people from missing the window

IRS 401(k) rules require the plan administrator to notify participants in writing that a distribution may be transferred to another individual retirement plan.

Once money leaves the old plan, save every page that came with it. Keep the distribution statement, the plan notice, the date you received any check, and confirmation from the receiving IRA or plan that the rollover landed. If the account is tied to a former employer record, make sure the destination institution has the same name and account details you intended, because a simple mismatch can slow the deposit long enough to become a 60-day problem.

A simple order of operations can prevent expensive mistakes

1. Locate the old Big Lots account and confirm whether it is still in the company plan or has already been distributed.

2. Compare the new employer’s plan and an IRA before asking for any payout.

3. Choose a direct rollover or trustee-to-trustee transfer if the plan allows it.

4. If a check is already in your hands, mark the receipt date immediately and count the 60-day deadline from there.

5. Confirm whether withholding was taken and whether you have outside funds available to make the rollover whole.

Why Big Lots workers may need to move faster than they think

In 2024, the company announced plans to close up to 315 stores and later added more closures as part of the restructuring. Former workers can be left with a narrow window to trace down retirement paperwork before the plan administration, mailing address or point of contact changes again.

Court documents put the workforce at roughly 27,700 employees when full-time and part-time workers are combined, spread across a national chain with about 1,300 stores.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?