Big Lots workers face sharper value demands as shoppers stay deal-focused

Deal-seeking is still the rule, but Big Lots workers are being asked to prove value in every aisle, every tag and every interaction.

Big Lots workers are being asked to do more than sell low prices. Deloitte’s 2026 retail outlook, built from a survey of 330 retail executives, points to a market where shoppers are still hunting bargains, but are also judging stores on how easy, clean and trustworthy the trip feels.

Value is no longer just a price tag

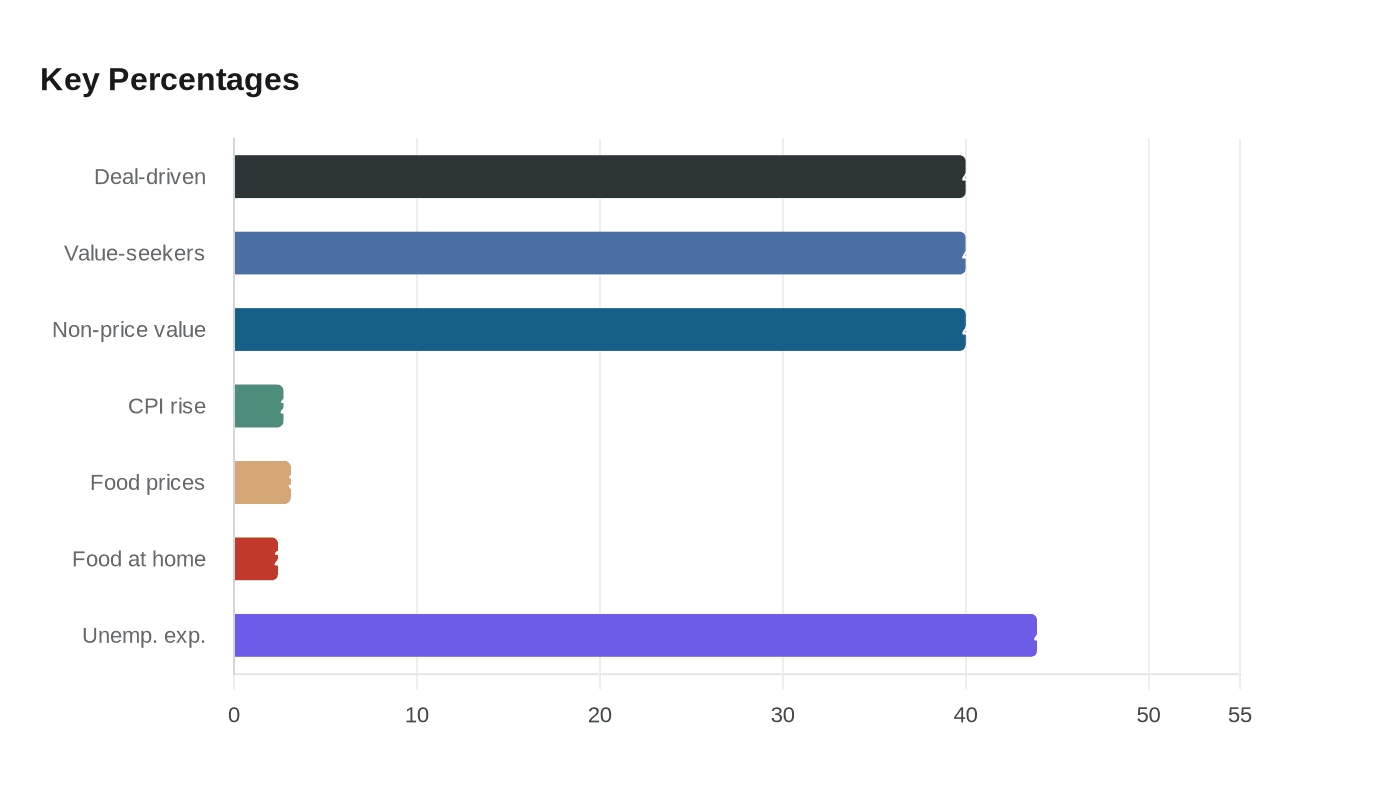

The biggest takeaway for a Big Lots shift is that “value” has become a full-store test. Deloitte says four in 10 Americans are now deal-driven or cost-conscious, and its separate consumer research says 4 in 10 American consumers are value-seekers. That matters in discount retail because it confirms something workers already see on the floor: customers are still looking for savings, but they are looking harder and comparing more carefully before they spend.

That shift is not limited to lower-income households either. Deloitte’s consumer report found that higher-income earners surveyed planned to spend 50% to 60% less in many discretionary categories than their peers. For a chain like Big Lots, that is a reminder that bargain traffic does not disappear when shoppers have more income. It just becomes more selective, more skeptical and more willing to wait for the right deal.

For associates, the practical result is simple. A customer may still come in for value, but they now expect the whole visit to prove it. If the price is right but the shelf is messy, the tag is wrong or the item is hard to find, the value story weakens fast.

What that means for schedules, freight and merchandising

Deloitte’s outlook is useful because it translates into the kind of pressure workers feel in scheduling and backroom work. A market built around value-seeking usually means tighter labor plans, more attention to freight flow and less patience for clutter on the sales floor. Stores are asked to look sharper with fewer mistakes, because customers shopping for bargains tend to notice every miss.

The report also says up to 40% of brand value perception comes from non-price factors such as quality, service, checkout ease, loyalty and employee interactions. That is a big clue for retail workers. It means store execution is not a side issue, it is part of the business case for why shoppers return.

On a Big Lots shift, that translates into a few daily realities:

- clean shelves and accurate signage matter as much as markdowns

- freight has to move quickly enough to keep value items visible

- checkout speed and problem-solving shape whether the trip feels worth it

- merchandising has to make deals obvious, not hidden

- friendly, informed help can keep a customer from walking out

Deloitte’s framing around customer centricity, financial discipline, operational excellence and data-driven insight is the corporate version of what the floor experiences as pressure to execute. Workers are not setting the strategy, but they are the ones who determine whether the strategy looks real in the store.

Inflation keeps shoppers cautious

The demand for value is showing up against a stubborn cost backdrop. The U.S. Bureau of Labor Statistics said overall CPI rose 2.7% from December 2024 to December 2025. Food prices rose 3.1% over that stretch, including a 2.4% increase for food at home. That kind of inflation does not produce panic, but it does keep households alert to price changes and more sensitive to every shopping trip.

The New York Fed’s April 2026 Survey of Consumer Expectations adds another layer. Mean unemployment expectations reached 43.9%, the highest reading of the series since April 2025. Even before a shopper steps into a store, that kind of labor-market anxiety can make them more cautious about discretionary spending.

For Big Lots workers, that likely means more comparison shopping, more questions about whether a price is really a deal and more pressure to justify every item on the shelf. Shoppers may still buy, but they are likely to buy with a calculator mindset. That can make baskets smaller, trips more deliberate and stockouts more frustrating.

Big Lots is carrying this shift from a weaker starting point

The Deloitte findings hit differently at Big Lots because the company has already been through a brutal reset. Big Lots filed for Chapter 11 bankruptcy protection on Sept. 9, 2024, in the U.S. Bankruptcy Court for the District of Delaware. Earlier that year, the company reported fiscal first-quarter 2024 net sales of $1.009 billion, down 10.2% from a year earlier, with comparable sales down 9.9%. CEO Bruce Thorn said at the time that the company was seeing a continued pullback in consumer spending, especially on high-ticket discretionary items.

By December 2024, the company had announced going-out-of-business sales at remaining locations and 555 corporate layoffs. Bankruptcy records showed the store-closure plan had expanded to 497 locations by Oct. 8, 2024. That history means Big Lots is not dealing with a routine retail slowdown. It is operating in a post-bankruptcy environment where every remaining store has to prove it can deliver value efficiently and consistently.

That background makes the Deloitte report more than a broad industry forecast. It helps explain why value alone is not enough. In a distressed chain, customers want low prices, but they also want confidence that the item will be in stock, correctly priced and easy to buy. Workers feel that pressure in the most ordinary parts of the day: unloading freight, fixing a mis-tagged shelf, keeping aisles shoppable and answering whether a deal is really a deal.

The store-level takeaway

For Big Lots, the market message is blunt. Shoppers are still deal-focused, but the definition of “good value” has widened. It now includes clean presentation, accurate pricing, fast checkout, reliable inventory and employees who can solve problems without making the customer work for it.

That is why the best Big Lots shifts in 2026 will not be measured only by what gets marked down. They will be measured by whether the store makes value feel easy, consistent and trustworthy. In a market where shoppers are counting every dollar, that is the difference between a visit that looks cheap and one that actually feels worth it.

Know something we missed? Have a correction or additional information?

Submit a Tip