Goldman Sachs BDC cuts NAV as non-accruals rise in private credit portfolio

Goldman Sachs BDC marked down NAV 3.7% as non-accruals climbed to 4.7% of amortized cost, with stress concentrated in pre-2022 loans.

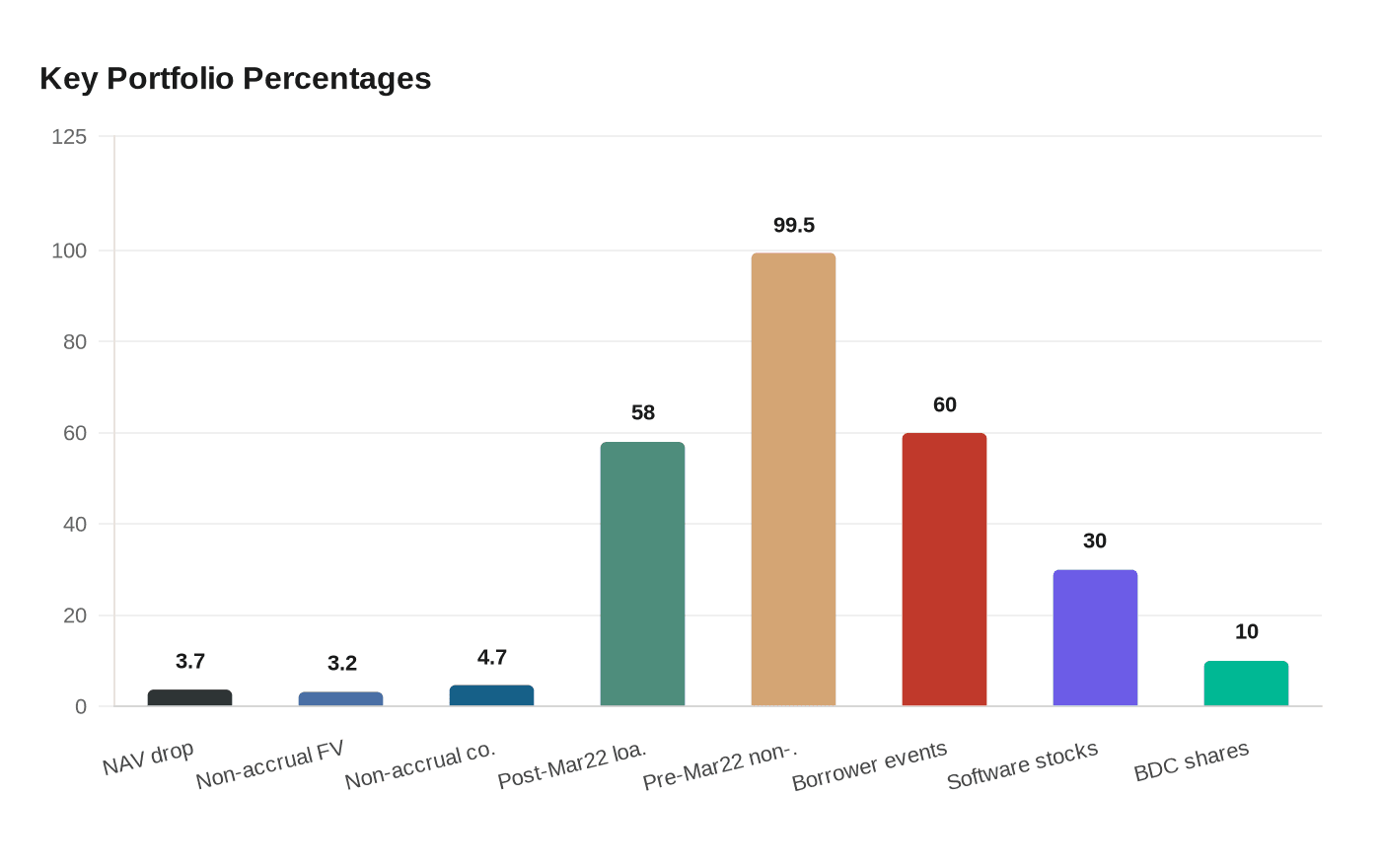

Goldman Sachs BDC cut its net asset value per share to $12.17 at March 31 from $12.64 at the end of 2025, a 3.7% drop that put fresh scrutiny on how tightly private credit managers are marking loans and policing underwriting quality. The portfolio held $3.8038 billion of investments at fair value and unfunded commitments, spread across 173 companies in 40 industries, but 11 of those companies were on non-accrual status by quarter-end, up from a level that already looked elevated a year earlier.

The pressure was concentrated in older deals. Goldman said two positions, One GI LLC and 3SI Security Systems, were placed on non-accrual in the quarter because of financial underperformance, and it said roughly 58% of the portfolio consisted of loans originated after the March 2022 management overhaul and were performing as expected. Even so, 99.5% of the non-accrual balance was tied to loans underwritten before March 2022, and about 60% of portfolio mark-downs stemmed from borrower-specific events, most notably the two legacy credits. That split matters inside Goldman Sachs Alternatives and Goldman Sachs Asset Management, where credit teams are being judged not just on deployment pace but on whether their marks, vintages and workout decisions hold up when borrowers stumble.

The fund said non-accruals represented 3.2% of the portfolio at fair value and 4.7% at amortized cost, a level that puts a spotlight on valuation discipline in a market still sensitive to spread moves. Goldman argued that the markdowns reflected broader market spread widening more than a wave of generalized credit deterioration, a distinction that will matter to fundraisers and clients comparing managers across the private credit shelf. The Bank for International Settlements has already flagged a sharp rerating in adjacent markets, saying software stocks fell almost 30% between October 2025 and February 2026 while BDC shares fell about 10% on average and discounts to net asset value widened.

Goldman was still putting money to work, but at a measured pace. It made about $46.5 million of new commitments in the quarter, funded $16.3 million of that amount, and reported $82.8 million of loan repayments and sales. The board declared a second-quarter 2026 base dividend of $0.32 per share, and the company had a $75 million stock repurchase authorization in place, though it bought back no shares in the first quarter. Net debt to equity rose to 1.37x from 1.27x at year-end, underscoring that even in a senior-secured book, leverage and credit selection remain central as internal workout teams push to maximize recoveries.

Know something we missed? Have a correction or additional information?

Submit a Tip