Goldman Sachs benefits as Wall Street pushes for capital-rule relief

Wall Street’s latest capital push could make Goldman’s lending and financing businesses cheaper to run, while lifting pressure on returns, payouts and balance-sheet strategy.

Wall Street banks are making another push to trim capital charges on credit-card lines and on the largest U.S. lenders, a fight that goes straight to how much balance sheet Goldman Sachs can devote to lending, prime brokerage and structured financing.

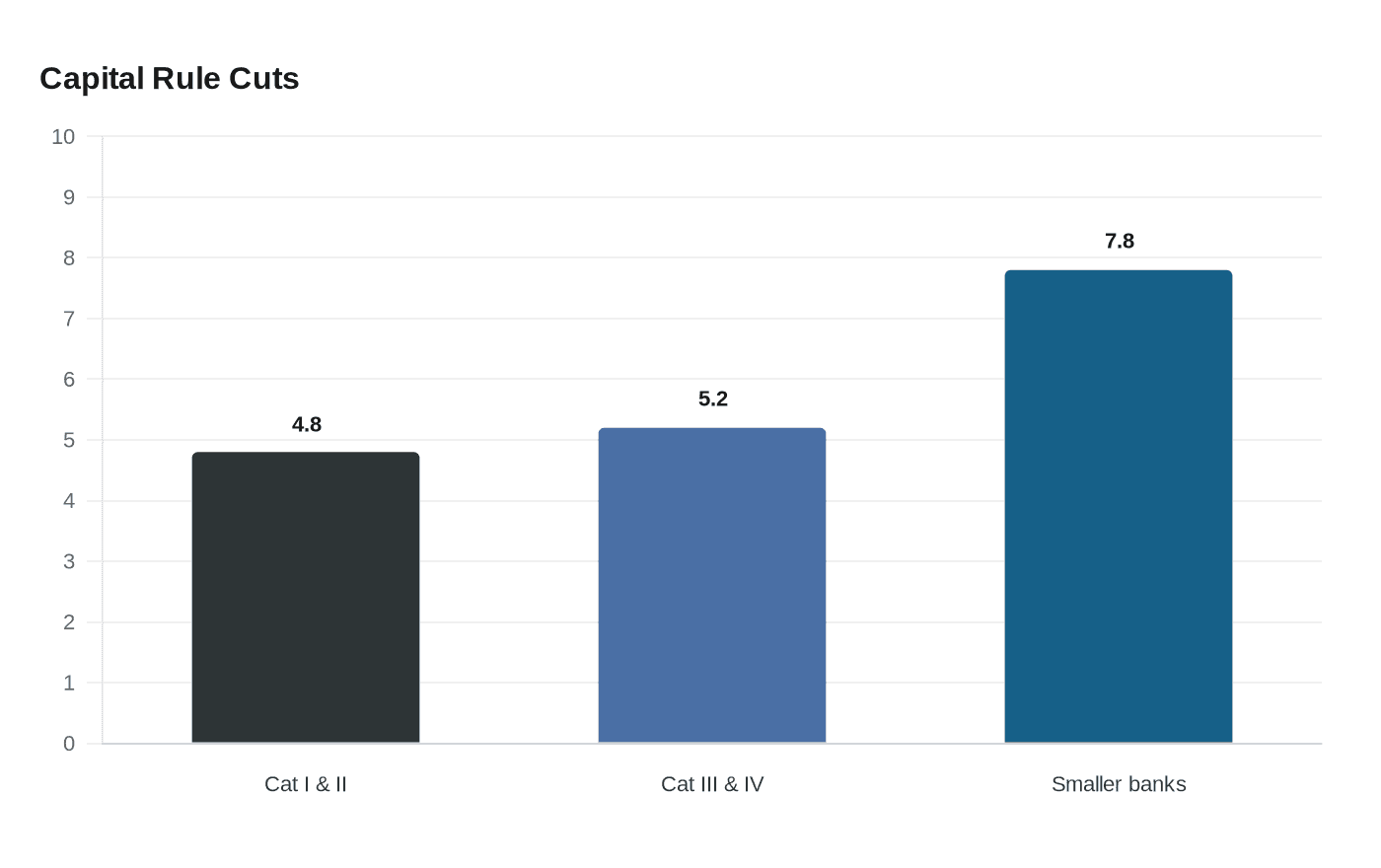

The Federal Reserve, the Federal Deposit Insurance Corporation and the Office of the Comptroller of the Currency jointly released capital proposals on March 19, 2026, after months of industry pressure. Federal Reserve staff estimated the package would cut aggregate common equity tier 1 requirements by 4.8% for Category I and II banks, 5.2% for Category III and IV banks, and 7.8% for smaller banks. The plan also included a separate proposal to revise the GSIB surcharge framework, which would amend the FR Y-15 reporting used to calculate extra capital for the biggest and most complex lenders.

For Goldman, that is not an abstract regulatory fight. The bank said in its 2025 annual report that it created a Capital Solutions Group to combine financing, origination, structuring and risk management across public and private markets, a sign that balance-sheet deployment has become more central to strategy. Goldman also reported 2025 net revenues of $58.3 billion, up 9%, earnings per share of $51.32 and return on equity of 15.0%, numbers that make capital efficiency a direct driver of how aggressively the firm can grow.

The economics matter because lower charges would make some activities cheaper to hold. Unused credit-card lines are one flashpoint: the industry wants relief on the roughly 10% capital treatment now tied to commitments that can be canceled at any time. If that burden eases, bankers can be more willing to extend credit, keep commitments open and price deals more aggressively, instead of pulling back limits when markets turn choppy. That would affect corporate lending, consumer credit, structured finance and the financing that supports major client relationships.

Goldman’s first-quarter 2026 results showed how much cushion still matters. The firm reported net revenues of $17.23 billion, net earnings of $5.63 billion and annualized ROE of 19.8%. Its CET1 ratio stood at 12.5%, which Goldman said was 110 basis points above its current capital requirement of 11.4%. On April 10, 2026, the board declared a quarterly dividend of $4.50 per share, payable June 29, a reminder that every extra point of regulatory headroom can affect not just lending capacity but distributions as well.

Michelle W. Bowman, who leads supervision at the Fed, has cast the overhaul as a modernization of bank-capital rules. Even with the March package, Wall Street is still pressing for more relief before the next political and regulatory cycle closes, and Goldman’s risk, financing and capital teams will be watching closely. If the rules move further, the bank could tilt more capital toward the businesses that produce the best returns, sharpen its pricing on big transactions and widen the gap between the firms that can afford to lend and the ones that cannot.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?