Goldman Sachs sees yuan 20% undervalued, forecasts further strengthening

Goldman says the yuan is more than 20% cheap, a call that could reshape Asia financing, exporter margins and cross-border deal flow if Beijing keeps letting it climb.

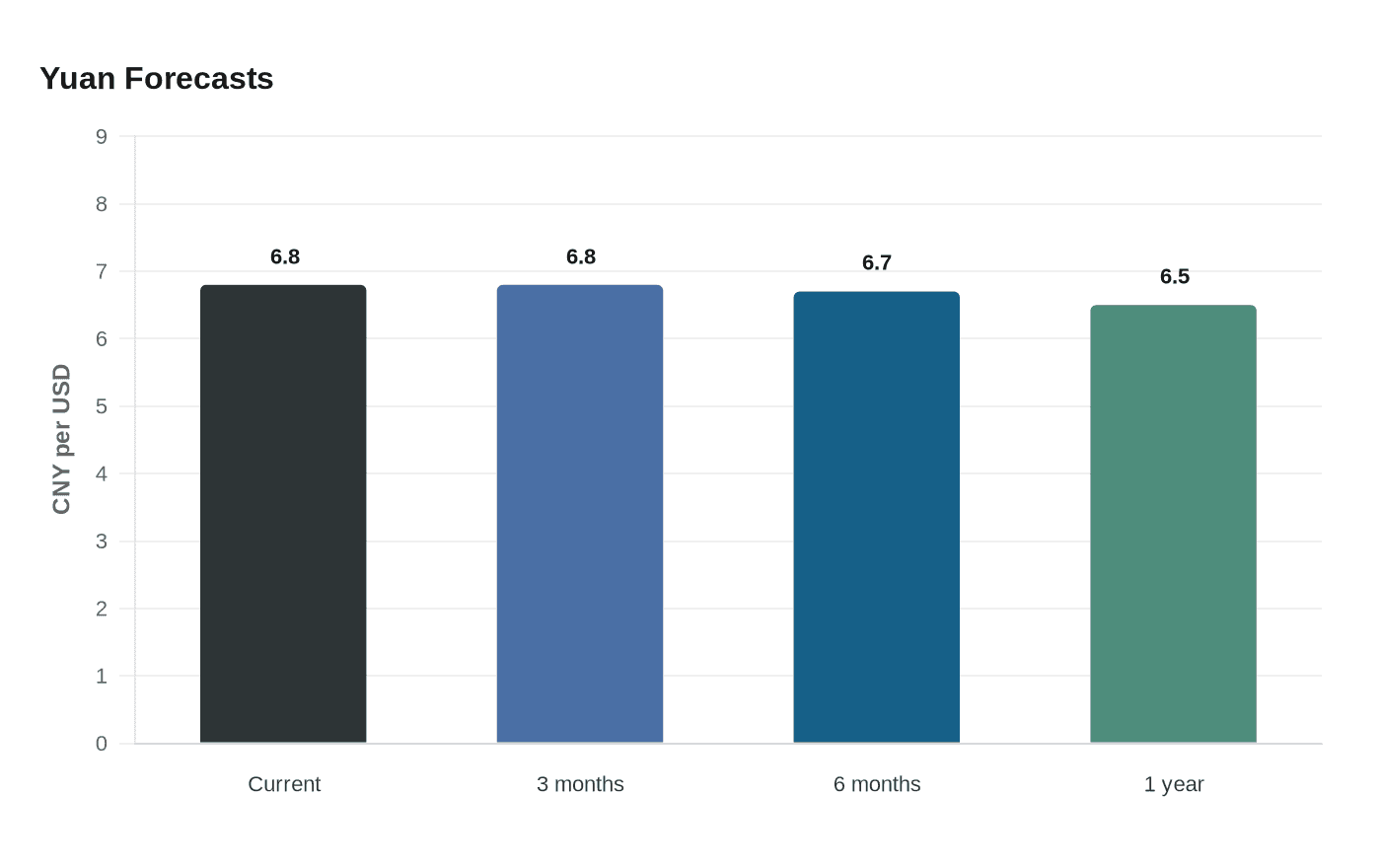

Goldman Sachs is betting that the yuan still has room to run, and the call matters well beyond currency traders. In a May 8 note, the bank said the renminbi was more than 20% undervalued against the US dollar and lifted its forecasts to 6.80 in three months, 6.70 in six months and 6.50 in one year. At the time, the yuan was already trading around 6.80, near its strongest level against the dollar since early 2023.

For Goldman’s Asia business, the consequence gap is clear: the forecast only works if Beijing keeps allowing appreciation while US-China tensions do not reverse the recent tone. Goldman said the currency remained below levels justified by China’s export strength and external surplus, a sign that the bank sees the move as more than a tactical trade. The People’s Bank of China set the midpoint at 6.8487 per dollar on May 7, its strongest fixing since March 24, 2023, while still managing the pace of gains. That leaves Goldman’s currency desks and Asia coverage bankers watching whether policy makers permit further strength or step in to slow it.

A stronger yuan would cut both ways for clients. Multinationals with China revenue or procurement exposure would gain purchasing power and could see the value of China-linked cash flows improve in dollar terms. Exporters, especially firms selling into the United States and other overseas markets, would face margin pressure and potential foreign-exchange losses as invoices translate into fewer yuan. That is the first-order impact Goldman’s corporate clients would feel, and it is where hedging demand could rise fastest if the currency keeps appreciating.

The macro backdrop gives Goldman cover for the call. The bank said China’s external surplus is approaching unprecedented levels as a share of global GDP, which it sees as evidence of deep export competitiveness and an equilibrium case for a stronger currency. Goldman Sachs Research projected China’s real GDP growth at 4.8% in 2026 and a current account surplus of 4.2% of GDP, up from 3.6% in 2025. In practical terms, that puts the bank on the side of a China story built on surplus, not stimulus, and it gives Goldman a chance to position ahead of peers if Beijing lets the yuan keep moving toward fairer value.

Know something we missed? Have a correction or additional information?

Submit a Tip