Goldman Sachs Declares April 2026 Preferred Stock Dividends Across Ten Series

Goldman Sachs declared up to $1,187.80 per preferred share on Thursday, the latest in a steady chain of capital returns that carries weight well beyond the treasury floor.

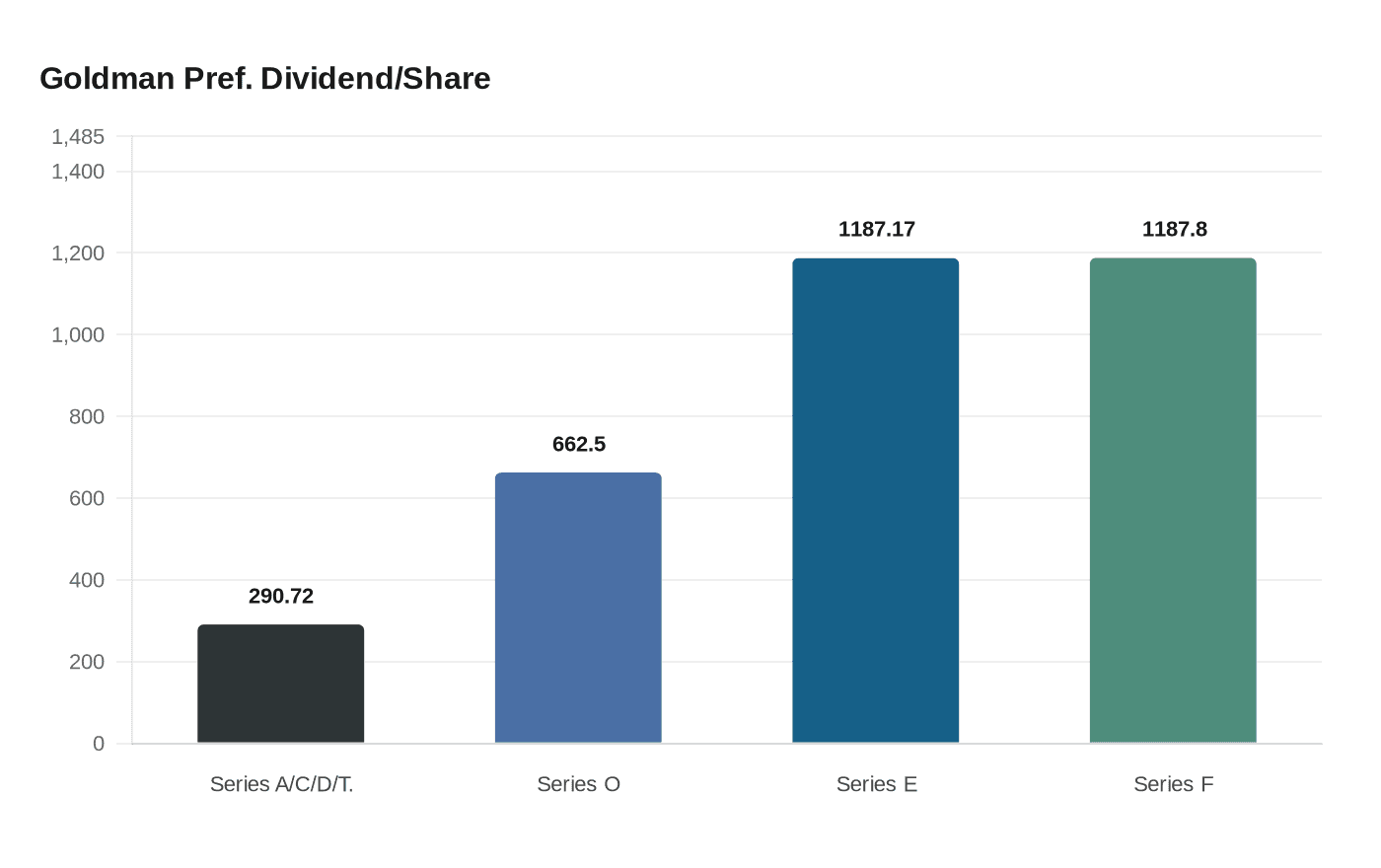

The numbers on Goldman Sachs' preferred stock declarations run larger than most people on the trading floor would guess. The firm committed $1,187.80 per share on its Perpetual Non-Cumulative Preferred Stock Series F and $1,187.17 on Series E, the headline figures in a ten-series dividend announcement made Thursday. Both represent a modest step down from January's quarterly declarations of $1,219.39 and $1,218.76 on the same two series, a narrowing that tracks the gradual drift in the floating-rate benchmarks underlying both instruments.

The full declaration covered Series A, C, D, O, T, V, X, Y, E, and F. Shareholders of record on April 26 will receive payment on May 10; a second tranche of series carries a record date of May 17 and a payment date of June 1.

| Series | Rate Structure | Dividend per Share | Record Date | Payment Date |

|---|---|---|---|---|

| Several floating-rate series (A, C, D, T, V, X, Y) | Floating-rate | $290.72 | April 26 or May 17 | May 10 or June 1 |

| O | Fixed-to-floating (5.30% until Nov. 2026; then SOFR + 4.096%) | $662.50 | April 26 or May 17 | May 10 or June 1 |

| E | Perpetual Non-Cumulative | $1,187.17 | April 26 or May 17 | May 10 or June 1 |

| F | Perpetual Non-Cumulative | $1,187.80 | April 26 or May 17 | May 10 or June 1 |

Preferred dividends occupy a structurally different place in Goldman's capital return stack than the $4 quarterly common stock dividend the firm locked in after last year's Fed stress tests, or the share repurchase programs that draw most of the analyst attention. Preferred holders sit above common shareholders in the payment hierarchy, and because Goldman's preferred stock is non-cumulative, any decision to skip a payment would be permanent: missed dividends do not accumulate for future recovery. That makes a steady declaration cadence a concrete signal of balance-sheet confidence, not a formality. Institutional investors and ratings analysts read an uninterrupted preferred payment history as a first-tier stability cue, and for Goldman, maintaining it carries direct implications for the cost of future preferred issuances.

Series O sits at an inflection point. Currently paying at a fixed annual rate of 5.30%, it converts to a floating rate of three-month SOFR plus 4.096 percentage points starting November 10, 2026, which means the effective yield on that series will move with wherever the Fed's rate path settles by year-end. That transition is arriving at a moment of genuine uncertainty; Fed officials have signaled caution about cutting rates too quickly, and a higher-for-longer posture would push Series O's post-November payments meaningfully above the current semi-annual fixed rate.

Inside 200 West Street, Thursday's release triggered a specific sequence of operational tasks: payment operations teams confirm shareholder records by the applicable dates, investor relations updates its creditor briefing materials, and legal and compliance staff process the associated regulatory disclosures. For those in treasury, the exercise is routine but consequential; preferred dividend declarations require board authorization and sit within the broader annual capital plan reviewed by the Federal Reserve.

The wider message for Goldman employees watching the capital allocation picture is that disciplined, continuous capital return and selective strategic investment are not mutually exclusive. CEO David Solomon said in January that there is "no job apocalypse" coming from AI, and the firm has been explicit that it sees AI infrastructure as a central pillar of its hiring and investment thesis for 2026. Capital discipline, including the uninterrupted cadence of preferred payments, preserves Goldman's funding cost advantages and investor confidence at precisely the moment the firm is making the case to clients, counterparties, and prospective hires that it is a stable platform in a volatile macro environment.

The Q1 2026 earnings call, scheduled for April 13, will give management its first formal opportunity to frame how the firm's financial performance translates into headcount and compensation decisions. Thursday's preferred dividend declaration, arriving three days before that call, sets a clean baseline: Goldman's obligations to its most senior equity claimholders are met, on schedule, and the discretionary math can proceed from there.

Know something we missed? Have a correction or additional information?

Submit a Tip