Goldman Sachs Flags Nvidia's Valuation Reset, Now Matching S&P 500 Despite Strong Growth

Nvidia's forward P/E fell to match the S&P 500 for the first time since 2013, even as the company drove 73% revenue growth and is set to fuel 21% of S&P earnings in 2026.

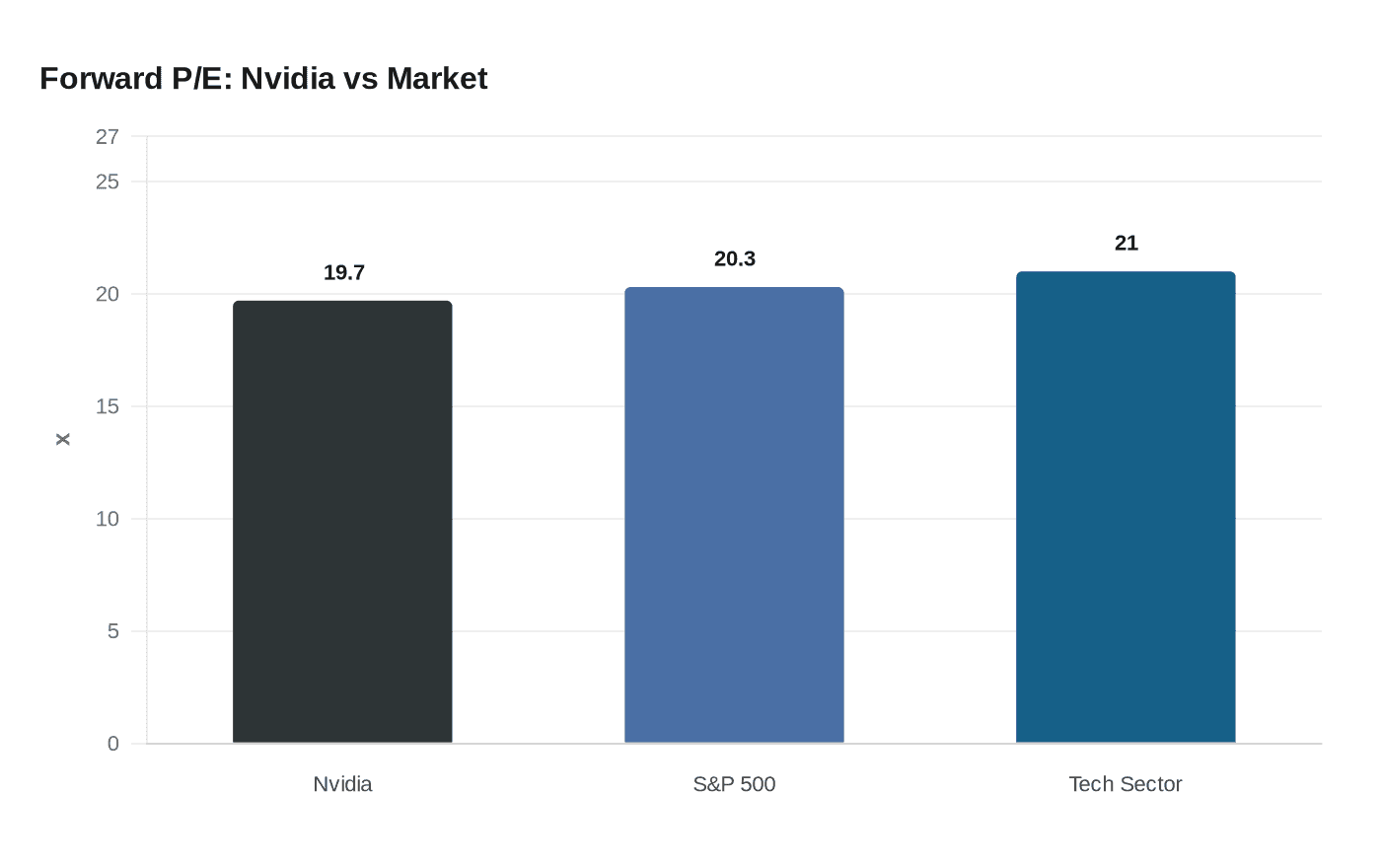

For the first time in more than 13 years, Nvidia is no longer rewarded with a premium valuation over the broader market. Goldman Sachs circulated a trading desk note on Monday flagging that Nvidia's forward price-to-earnings ratio had fallen to approximately 19.7 times, slightly below the S&P 500's roughly 20.3 times — a convergence the note described as a "growth disconnect" given that the company remains one of the most powerful earnings engines in the index.

The last time Nvidia failed to command a premium multiple over the S&P 500 was before 2013, a period that predates the company's transformation into the dominant force in AI infrastructure. That context makes the reset all the more striking: Nvidia reported Q4 revenue of $68.1 billion, up 73% year over year, with data-center revenue of $62.3 billion rising 75% in the same period. Full-year revenue reached $215.9 billion. The company guided its current quarter to a midpoint of approximately $78 billion, above Wall Street consensus, and analysts expect Nvidia to drive roughly 21% of S&P 500 earnings growth in 2026.

Goldman's note did not call the stock cheap in absolute terms. Rather, it flagged a relative anomaly: a company producing outsized earnings growth is no longer being rewarded with an outsized valuation. Wall Street price targets remain aggressive — Goldman's own sits at $250, implying roughly 49% upside from recent levels, while JPMorgan holds a $265 target, Morgan Stanley $260, and UBS $245.

The multiple compression traces back to several compounding shocks. On January 27, 2025, Chinese startup DeepSeek released its R1 model, which reportedly matches the performance of leading Western AI systems at a fraction of the development cost: roughly $5.6 million over approximately two months, compared with over $100 million for OpenAI's GPT-4. The revelation raised fundamental questions about whether the scale of GPU demand underpinning Nvidia's growth thesis was sustainable. Nvidia shed approximately $589 billion in market capitalization in a single session, the largest single-day market cap loss in U.S. stock market history, with shares falling nearly 17% to close at $118.58 — their worst single-day performance since March 16, 2020.

Pressure has not relented. Nvidia disclosed a $5.5 billion charge in its first quarter of fiscal 2026, tied to U.S. export controls on its H20 chips to China, a market that accounted for more than 10% of fiscal 2025 sales. Broader tariff uncertainty has weighed on the semiconductor sector; the tech sector's aggregate forward P/E dropped to around 21, its lowest level in three years.

CEO Jensen Huang has pushed back on the bearish narrative. At a company conference in 2025, Huang projected $1 trillion in combined sales across Nvidia's Blackwell and Vera Rubin platforms between 2025 and 2027, and called a $10 trillion company valuation "not far-fetched." Over the past decade, Nvidia returned approximately 19,334% to shareholders, against roughly 213% for the S&P 500 over the same period, which makes it all the more notable that the two now trade at the same multiple.

Whether the convergence represents a genuine re-rating opportunity or a value trap turns on a narrow set of variables: margin durability as Blackwell scales, the trajectory of hyperscaler capital expenditure, and whether earnings revision momentum can reassert itself against intensifying competition from AMD and custom silicon projects at Amazon and other large cloud providers.

Know something we missed? Have a correction or additional information?

Submit a Tip