Goldman Sachs Forecasts Gold at $5,400 on Central Bank Demand Surge

Goldman held its $5,400 gold target after the metal's worst monthly drop in 17 years, and the math behind the call tells employees exactly what to watch.

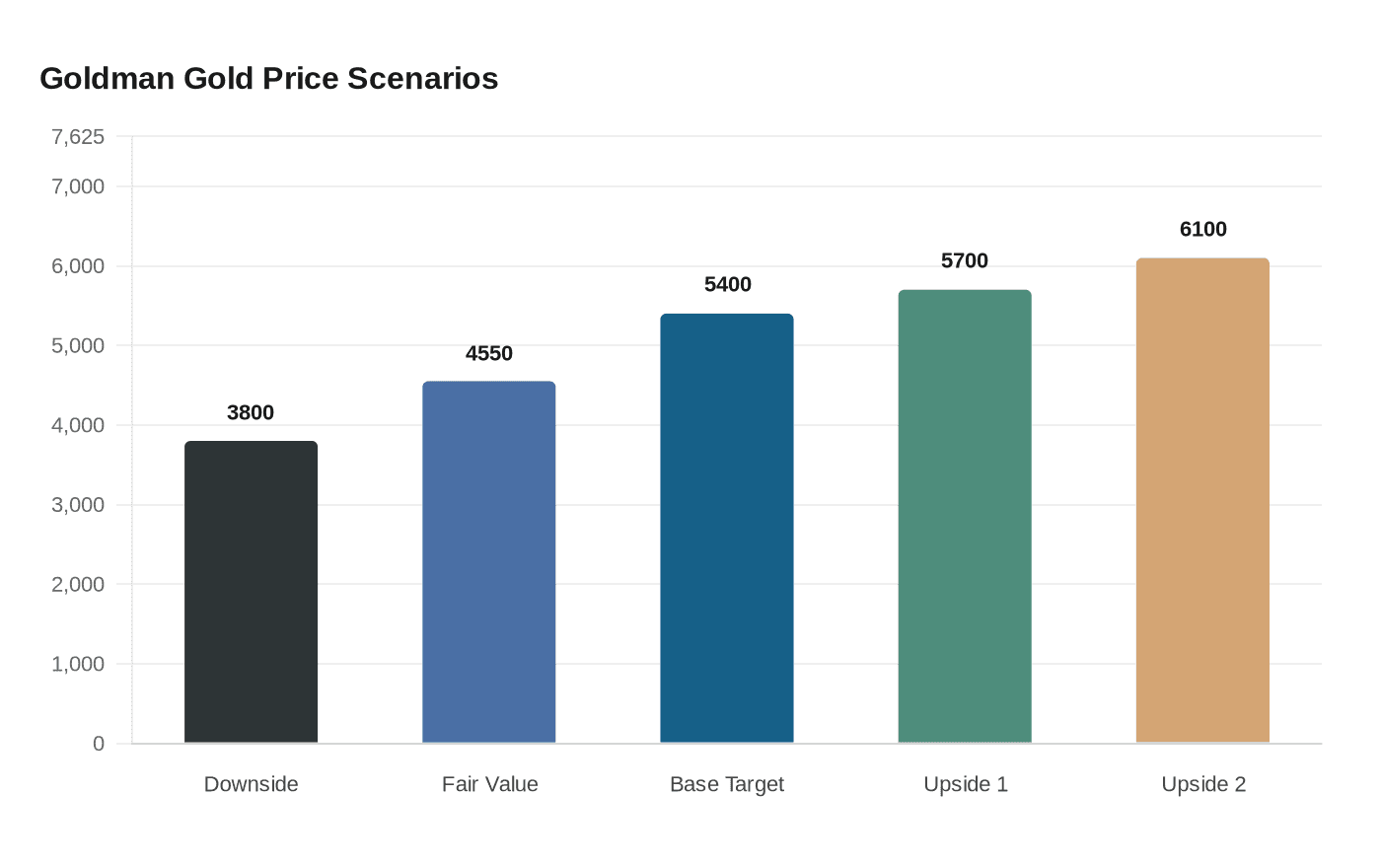

After gold fell 13% in March, its worst monthly decline in 17 years, Goldman Sachs analysts Lina Thomas and Daan Struyven held their $5,400 per troy ounce year-end target. The decision to stand firm, rather than trim, turns on two drivers with specific, quantifiable thresholds, and each one is a direct signal about how far the world has drifted from dollar-anchored reserve management.

The biggest single variable in the model is a re-acceleration of official sector buying to 60 tonnes per month. Goldman estimates that factor alone contributes approximately $535 per troy ounce to the target, accounting for more than half the distance between the firm's current fair value estimate of $4,550 and the $5,400 call. The underlying assumption: emerging-market central banks continue diversifying foreign-exchange reserves away from U.S. Treasuries, a structural shift that accelerated after Western sanctions on Russia in 2022. Monthly World Gold Council purchase figures are the most direct read on whether that pillar holds. Any sustained drop below 60 tonnes would shave the single largest contributor out of the model.

The second driver is the persistence of private-sector hedging built around doubts about fiscal sustainability and central bank independence. Thomas and Struyven described these allocations as "stickier" than the event-driven bets that unwound after the November 2024 U.S. election: longer-term concerns do not resolve on a known date. Western ETF holdings have already added roughly 500 tonnes since the start of 2025, running ahead of what Fed rate cuts alone would justify. Goldman expects two more rate cuts in 2026, worth an estimated $120 per ounce, but the more consequential signal is whether those hedge positions survive the current geopolitical turbulence. Sanctions activity and reserve-management announcements from major emerging-market authorities are the headlines most likely to either reinforce that allocation or accelerate its unwind.

The March selloff itself is where Goldman's framework gets precise. "Like in 2022, gold typically underperforms initially in supply disruption episodes," Thomas and Struyven wrote, drawing a direct line between the current Middle East conflict and the dynamic that briefly crushed gold four years ago. Supply-shock inflation benefits commodities broadly; gold specifically outperforms when inflation fears center on central bank credibility. For Goldman employees tracking the cross-asset read in real time, the 10-year TIPS yield is the most useful single input: a sustained climb in real rates would simultaneously erode the Fed-cut contribution and weaken the debasement trade, the two pillars that together account for $655 per ounce of the target.

Following the selloff, net speculative positioning on Comex had fallen to the 39th percentile, which Goldman characterized as a "more attractive entry point." The firm's risk distribution is asymmetric: upside scenarios stretch to $5,700 or $6,100 if private-sector call-option buying accelerates, while the stated downside of $3,800 requires both a prolonged Strait of Hormuz disruption and a broad equity liquidation occurring simultaneously. Goldman separately dismissed concerns that Gulf central banks would follow Turkey, which sold roughly 52 tonnes, noting that Gulf nations hold far smaller gold shares and operate through dollar-pegged currency systems.

For anyone running a cross-asset book at Goldman, the $5,400 call functions less as a price prediction than as a verdict on the dollar's durability as a reserve anchor. Gold's more than 70% gain over the past 12 months, if it continues, will reflect not just a commodity trade but a sustained institutional judgment that U.S. Treasuries alone no longer provide sufficient reserve diversification. That is the reading with direct implications for Treasury demand, real rates, and USD positioning far beyond any single commodities desk.

Know something we missed? Have a correction or additional information?

Submit a Tip