Goldman Sachs: Hedge Funds Suffer Worst Monthly Drawdown in Four Years

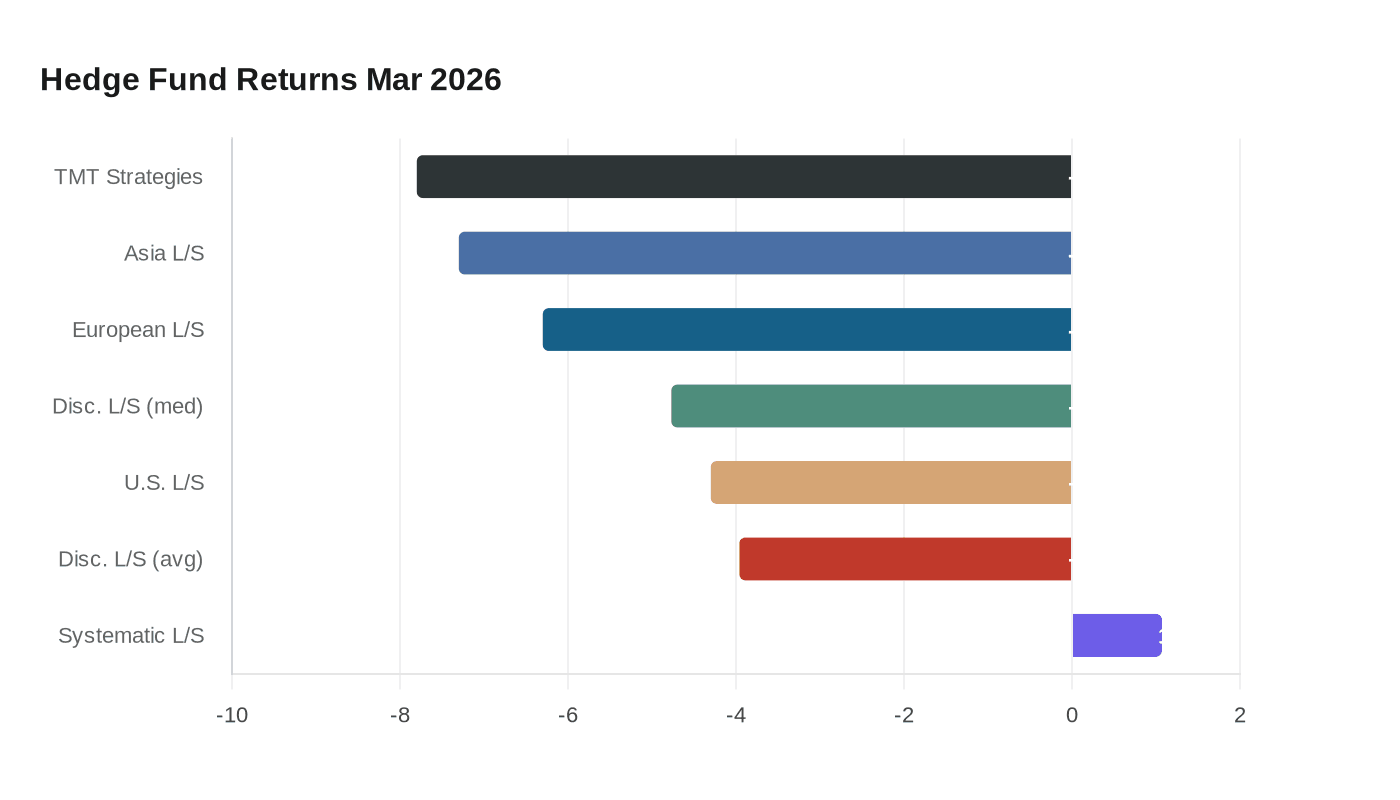

Systematic funds bucked a brutal March, gaining 1.07% while discretionary long/short managers lost an average 3.96% in the worst hedge fund month since January 2022.

Goldman Sachs prime clients sold global equities for the fourth straight month in March, at the fastest pace the bank had recorded in years, as a Prime Services client note revealed hedge funds had just endured their worst monthly drawdown since January 2022.

The note, circulated to clients April 1, put precise numbers to the damage. Discretionary long/short managers posted an equally weighted average loss of roughly 3.96% in March, with the median fund down 4.77%, a spread that signals concentrated pain rather than a uniform market move. Asia-focused long/short managers led regionally at down roughly 7.3%; European funds fell approximately 6.3%; U.S. long/short funds shed about 4.3%. Technology, media and telecom strategies absorbed the worst of it: down approximately 7.8% in March and 11.8% for the full first quarter. The note described March 2026 as "one of the more demanding months for the hedge fund industry in recent years," attributing the losses to elevated geopolitical risk tied to the Iran conflict, rapid market repricings across asset classes, and a sharp spike in cross-asset volatility.

One cohort did not suffer. Systematic long/short strategies finished March up roughly 1.07%, a divergence that echoes what happened during the January 2022 de-grossing episode. Then, as now, concentrated discretionary books built around momentum and growth exposures absorbed the worst of a rapid leverage unwind, while quant strategies with shorter holding periods and diversified factor tilts stayed insulated from headline-driven selling.

The January 2022 comparison matters beyond the performance numbers. That episode was defined by crowding, leverage, and a self-reinforcing de-grossing loop: as prime financing conditions tightened and crowded factor positions moved against funds, forced selling begat more selling. The four-month consecutive net selling streak Goldman's prime clients are now in, at the fastest pace in years, suggests the same mechanics are running in March 2026.

Three indicators will signal whether this is a positioning reset or the start of a deeper unwind. Prime financing rates: if borrowing costs for equity long/short strategies rise, re-leveraging stalls and the rebound in gross exposures is delayed. Short interest concentration in TMT names: with the sector down 11.8% for the quarter, it remains the most exposed pocket if a second wave of crowded exits materializes. Crowded factor unwind risk: the gap between March's average and median long/short returns (3.96% vs. 4.77%) suggests not all concentrated positioning has cleared.

On the desk, the implications are immediate. Prime brokerage and sales teams face elevated settlement volumes, margin calls, and urgent client requests for temporary financing and liquidation support. Trading desks must balance the opportunity in distressed bid-ask spreads against short-squeeze risk from rapid short covering across risk books. Structuring teams are already fielding demand for downside protection and liquidity solutions as clients seek ways to hedge into Q2. If the deleveraging persists through the second quarter, bonus pools for prime services and trading businesses face real pressure.

Research and macro desks are on an accelerated production schedule, working to deliver situation analyses for institutional clients navigating a market environment where systematic strategies are the only clear winners. For analysts and associates on the prime desk, extended client-service hours across time zones are not a near-term possibility; they are already the reality.

Know something we missed? Have a correction or additional information?

Submit a Tip