Goldman Sachs Report Contradicts Trump, Highlights US Dependence on Gulf Refined Products

Goldman's March research finds 60% of Gulf crude has no global substitute for diesel and jet fuel, exposing the gap between Trump's independence claim and daily fuel prices.

Nearly 60% of crude exports from the Arabian Gulf are medium-heavy grades, the feedstock primarily used to produce jet fuel and diesel, and there are few replacement producers of these refined products outside the Middle East. That structural fact, drawn from a Goldman Sachs research note, is what makes President Trump's April 2 energy-independence argument incomplete in the ways that matter most to American consumers.

In his primetime address, Trump tried to quell fears by downplaying the stakes in the Strait of Hormuz, insisting the U.S. doesn't depend on the critical trade chokepoint. "The United States imports almost no oil through the Hormuz Strait and won't be taking any in the future. We don't need it. We haven't needed it and we don't need it," he said. On crude imports alone, that argument has some standing. On refined products, it falls apart under Goldman's numbers.

Goldman characterized the Middle East disruption as the largest oil market shock on record, and the bank's analysis found it would hit products such as jet fuel and diesel far harder than crude. Strategists Yulia Zhestkova Grigsby and Daan Struyven identified the mechanism: a mix of shutdowns driven by both direct damage and precautionary measures has taken roughly 2.2 million barrels per day of global refining capacity offline. The effective closure of the Strait of Hormuz has simultaneously choked off exports from the world's densest concentration of refineries processing exactly the crude grades that produce distillates.

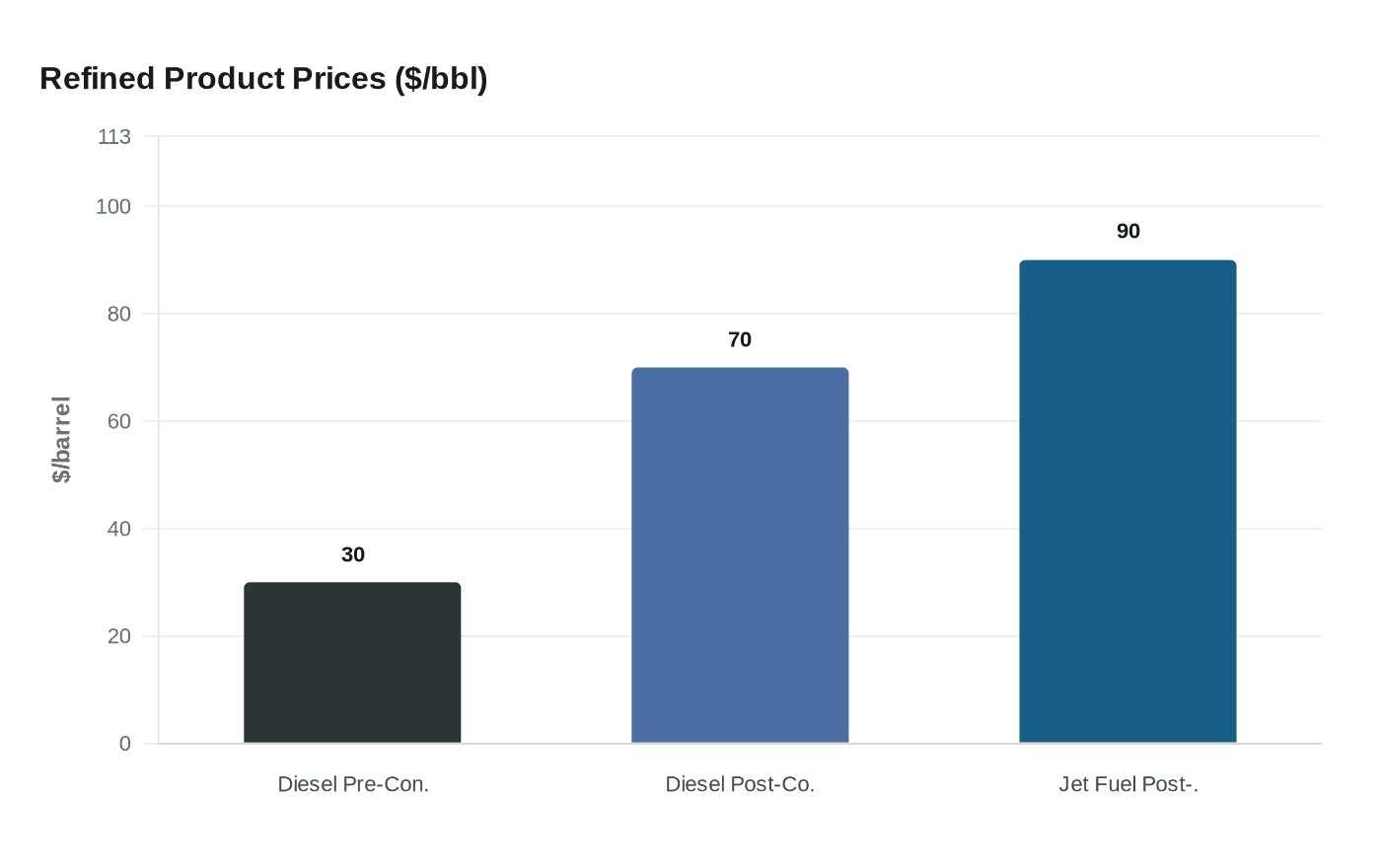

The price data confirmed the gap. Diesel crack spreads more than doubled, from approximately $30 per barrel before the conflict to above $70, and jet fuel premiums hit records above $90 per barrel in some markets. "Prices have rallied much more for many refined products than for crude," Grigsby and Struyven wrote. Crude prices surged more than 40% since the first attacks, with Brent topping $100 a barrel, but refined products have rallied far more; in parts of Asia, fuel costs roughly doubled, with South Korea, China, and Thailand all capping exports to protect local markets. For Goldman's energy and commodities clients those numbers represent a directional trade. For trucking companies repricing freight contracts, airlines revising capacity, and drivers at the pump, they represent a durable cost increase.

The Strategic Petroleum Reserve does not solve the specific problem. Goldman warned that the IEA's 400 million-barrel coordinated release, the largest in history, may be insufficient to cover the Hormuz disruption, projecting a potential shortfall exceeding 10 million barrels per day. The firm modeled a scenario requiring 254 million barrels from global strategic reserves alongside 31 million barrels of additional Russian crude supply just to reduce the hit to commercial inventories by roughly 50%. The core issue is that the SPR holds crude, not the refined distillates in shortest supply; releasing it addresses feedstock without replacing the refining capacity that went offline.

The fastest available policy levers are each constrained by the same underlying problem. U.S. refineries can push utilization toward maximum capacity, but American shale is predominantly light and sweet, poorly suited to producing the middle distillates now in shortage. Import substitution faces the same barrier globally; "no products or regions are fully immune," the Goldman analysts concluded. With infrastructure damage to Gulf refineries expected to require years of repair, the disruption carries the profile of a structural repricing of freight and air travel costs rather than a commodity spike that fades when the headlines do.

Know something we missed? Have a correction or additional information?

Submit a Tip