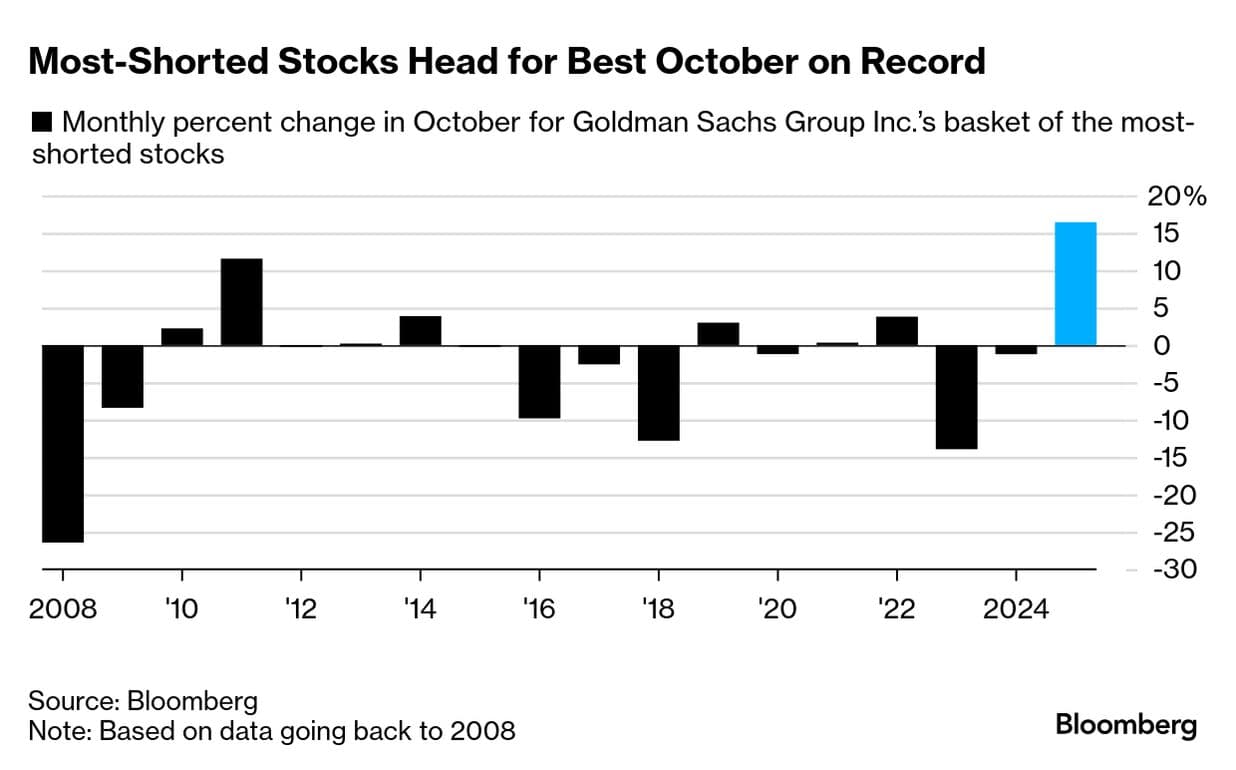

Goldman Sachs Most-Shorted Basket Surges 7.1% in Positioning-Driven Rally

Goldman's basket of the 50 most-shorted U.S. stocks surged 7.1% on April 1, driven by forced covering and gamma dynamics, not Iran de-escalation headlines.

The 7.1% surge in Goldman Sachs's basket of the 50 most-shorted U.S. stocks on April 1 was not a peace dividend; it was a positioning unwind dressed in geopolitical clothing.

Initial headlines that day suggested de-escalation in the Iran conflict had triggered the sharp rebound in U.S. equities. Traders at Goldman Sachs and JPMorgan told a different story. The actual engine was forced deleveraging and short covering, amplified by options expiries and month-end rebalancing flows that had been accumulating since late March. The most-shorted names absorbed that pressure first and fastest, producing the 7.1% spike that dwarfed broader index moves.

The sequence matters. Geopolitical news provided the ignition, but the fuel was already loaded: stop-runs on heavily shorted positions, gamma covering by dealers whose options books had skewed toward short-delta exposure, and pension-fund rebalancing flows that added systematic buying pressure. When those three mechanics converged intraday, Goldman's most-shorted basket became the release valve.

For traders and risk managers, the episode illustrates the gap between the headline narrative and actual flow composition. Detecting the difference in real time requires watching intraday breadth divergences: when the most-shorted names outperform broad indices by a multiple, covering mechanics rather than fundamental re-rating are almost certainly the driver. Prime brokerage utilization rates and borrow cost spikes in the hours before a squeeze, combined with dealer gamma positioning data, are the earliest available signals that a mechanical move is loading. When all three converge near an options expiry or month-end window, the probability of an intraday shock of the April 1 variety climbs sharply.

Risk and portfolio teams that treated last week's move as a fundamental event would have made structurally incorrect decisions: adding risk into a covering-driven bounce that had no earnings or macro catalyst underpinning it. The practical response is to flag flow-versus-fundamental divergence explicitly at the time of the move, suspend position additions until the covering cycle exhausts, and document that determination for compliance review given the concentrated and rapid activity in shorted names.

For junior analysts and associates in sales and research, the event created immediate demand for rapid-turnaround client explainers that parse mechanical drivers from macro developments. Senior bankers were distributing those notes the same afternoon; associates who produced the clearest breakdown of positioning mechanics versus geopolitical signal earned direct visibility in front of clients.

Legal and compliance teams face a separate deliverable: concentrated, rapid activity in heavily shorted names requires post-event surveillance review and best-execution documentation. With prime brokerage data feeding into those reviews, the paper trail from April 1 needs to be complete.

The positioning dynamics that produced that move have not fully resolved. Options expiries, ETF flows, and prime-brokerage deleveraging cycles that accumulated through late March remain active variables. Cross-desk coordination between trading, risk, prime services, and client coverage is the organizational response that will be tested again when those mechanics next converge.

Know something we missed? Have a correction or additional information?

Submit a Tip