Goldman Sachs warns oil price drop may mask deeper supply risks

Oil’s slide looked like relief on Iran, but Goldman says stocks are still near an eight-year low and barrels may stay tight for weeks.

Jerome Dortmans is warning Goldman clients not to mistake a softer oil tape for a solved supply problem. Prices fell as investors bet the Iran conflict could ease soon, but the co-head of Global Oil and Products Trading in Goldman Sachs Global Banking & Markets said the market is more complicated than the headline suggests.

Goldman posted Dortmans’ conversation on May 8 as part of The Markets series, a roughly 54-second update that reads more like a desk-level market check than a long research note. That matters for traders, sales staff, and macro teams because the discussion focuses on crude and refined products, not just the direction of Brent and WTI, and points to where trading opportunities may emerge as the curve reacts to shifting headlines.

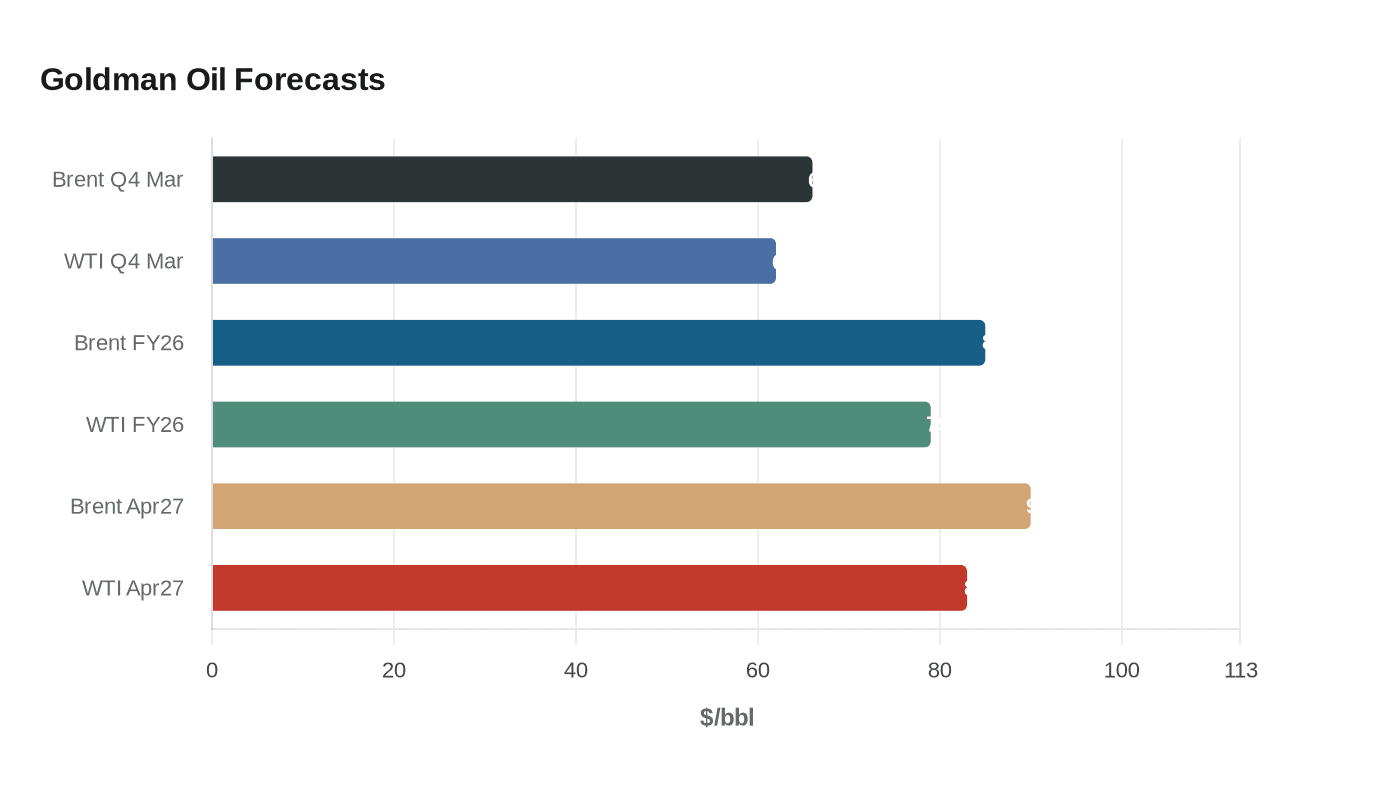

The deeper issue is structure. Goldman said in March that the outlook for energy prices would hinge on disruptions through the Strait of Hormuz, the chokepoint through which around one-fifth of global oil and LNG supply normally flows. Since then, the firm’s price calls have moved quickly. In March, Goldman lifted its fourth-quarter 2026 Brent forecast to $71 a barrel from $66 and its WTI forecast to $67 from $62. Later, it raised its full-year 2026 estimates to $85 for Brent and $79 for WTI on expectations of a prolonged disruption. By April 27, Goldman had pushed its fourth-quarter forecasts again, to $90 for Brent and $83 for WTI, citing lower Middle East production and a large inventory draw.

Those revisions line up with a tighter physical backdrop. Goldman said global oil stocks were approaching their lowest level in eight years, with total stockpiles at about 101 days of global demand. Even if a peace deal ended the fighting, supplies were expected to tighten further because it would take weeks for shipments from the Middle East Gulf to resume and reach refiners around the world. In the meantime, storage tanks could keep drawing down just as peak summer demand builds.

For Goldman employees, the message is bigger than one commodity call. A move in crude can flow into inflation expectations, consumer spending, airline and transport margins, European industrial costs, and rate-cut assumptions. It also reaches refined fuels such as jet fuel, naphtha, and LPG, which can matter even when crude itself looks less impaired. For the analysts, associates, and VPs turning these moves into client advice, the real edge is separating the day’s geopolitical noise from the market architecture underneath it. That distinction can shape the pitch, the trade, and, by year-end, the story told about who saw the risk early.

Know something we missed? Have a correction or additional information?

Submit a Tip.png&w=1920&q=75)