Goldman Sachs Warns US Labor Market Cooling May Persist Into 2026

Goldman economists see unemployment holding near 4.5% through 2026 with no meaningful decline in sight, even as AI threatens to pull forward job losses for entry-level knowledge workers.

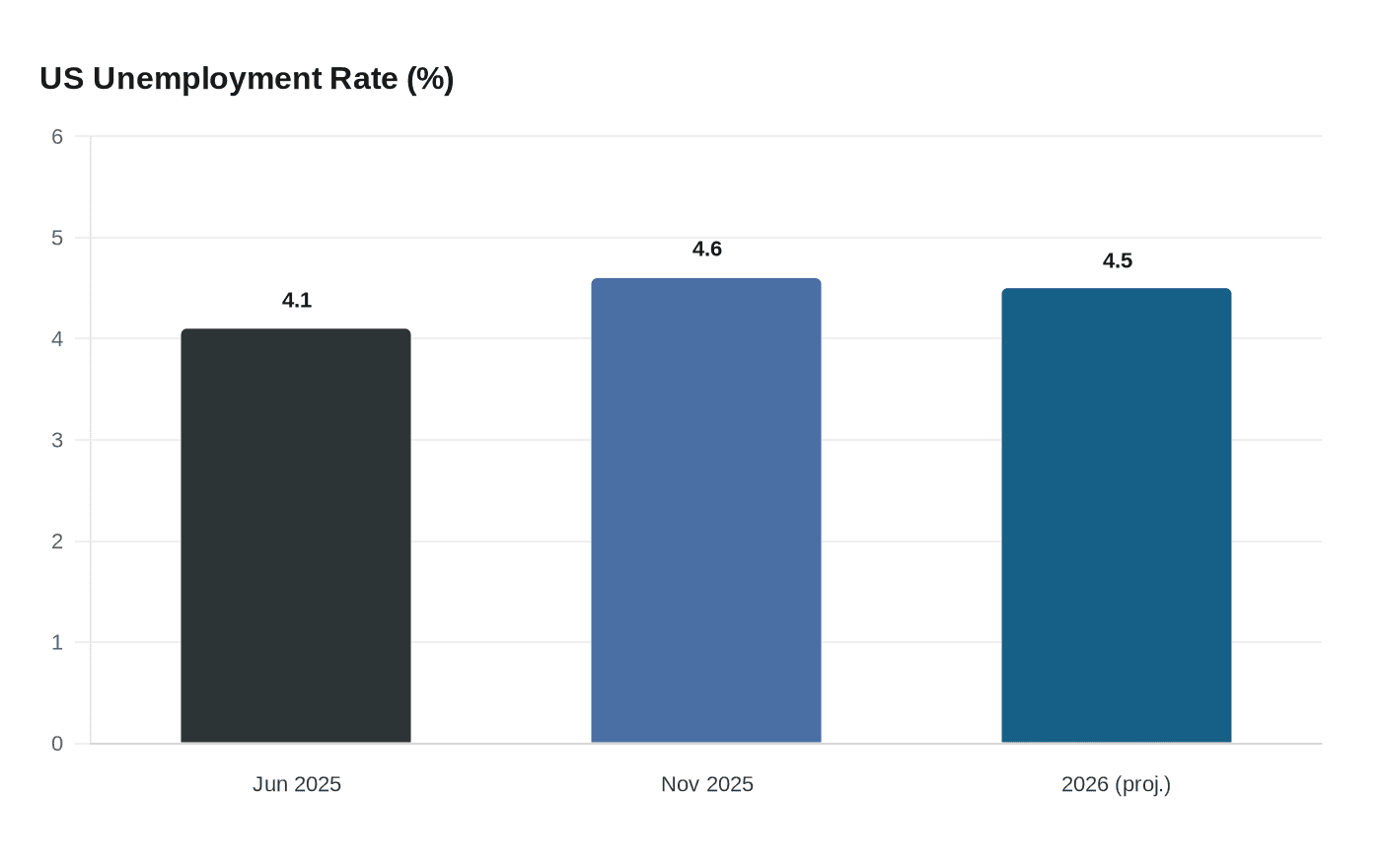

Goldman Sachs economists warned that the US labor market's prolonged cooling is unlikely to reverse in the near term, projecting unemployment will stabilize around 4.5% through 2026 even as the firm's own macro outlook called for stronger GDP growth, and flagging AI as the wildcard that could push conditions further in the wrong direction.

The slowdown took hold in the second half of 2025, when job growth began decelerating in ways that proved durable. "The labor market in the US has been in sharp focus over the past nine months or so," said Goldman economist Briggs, citing the stretch "ever since we started to see job growth slow in the second half of 2025." By November, the unemployment rate had climbed to 4.6%, up from 4.1% in June. February brought a nonfarm payrolls reading that subtracted 92,000 jobs from the economy, and annual revisions confirmed the damage was cumulative: the US added only 181,000 jobs over the prior year, down from 1.4 million the year before.

Goldman identified two structural shocks behind the 2025 deceleration. The first was tariff uncertainty, which eroded employer confidence in hiring. The second was a sharp slowdown in immigration after a fast pace in 2023 and 2024, a headwind Goldman expected to persist as net immigration continued to slow. The 11-percentage-point increase in the average effective tariff rate shaved 0.6 points from US GDP in the second half of 2025, though Goldman projected that drag would fade if tariff rates remained broadly unchanged.

For 2026, Goldman's outlook identified faster GDP growth driven by the reduced tariff impact and tax cuts and reforms embedded in the One Big Beautiful Bill Act, but the firm was explicit that growth would not translate into labor market relief. "We do not see a meaningful decline anytime soon," the firm's economists wrote of unemployment, adding that further increases were plausible "if either productivity-enabling AI applications arrive more quickly than expected or company management teams increase their focus on lowering labor costs in 2026."

Briggs named AI as the defining labor story of the year. Goldman's research found that roughly 300 million jobs globally are exposed to AI automation, and that in the US, AI could potentially automate tasks accounting for 25% of all work hours. Entry-level workers in their 20s and 30s in knowledge and content creation were identified as the group most likely to absorb the early impact of new AI deployments. Management consultants, call center workers, and graphic designers had already seen some displacement, Goldman noted, though no broad shift had yet registered in aggregate labor data. "The big story in 2026 in labor will be AI," Briggs said. "If we see some job losses pulled forward, that sets stage for potential underperformance relative to our forecast, and that may lead the Federal Reserve to cut rates."

The picture at the margin was partly obscured by a surge in gig work. Goldman's analysis found that 20% of workers who lost pay, lost a job, or had hours cut turned to platforms including Uber, DoorDash, and Instacart. But gig wages ran only 50% to 65% of what those workers previously earned, and Goldman cautioned that the cushion had limits: "The support available to some workers in normal times would likely be inadequate for all job losers in a recession." Companies had already announced more than 1.1 million layoffs in 2026, a 44% increase over 2024's total, with Amazon, Target, and UPS among the largest contributors.

Goldman's near-term payroll forecast sat materially below consensus, projecting roughly 45,000 new jobs for January against a market expectation of around 70,000, citing updates to the Bureau of Labor Statistics birth-death model and weak underlying data. Goldman still sees the largest productivity benefits from AI as several years away, which means the current softness reflects structural realities rather than a brief cyclical dip; the base case is a prolonged holding pattern on both jobs and Fed policy.

Know something we missed? Have a correction or additional information?

Submit a Tip