Goldman Sachs: Widespread AI could displace about 6% of U.S. workers

Goldman Sachs research estimates widespread AI adoption could displace about 6% of U.S. workers, even as the bank says measurable GDP gains may not arrive until 2027.

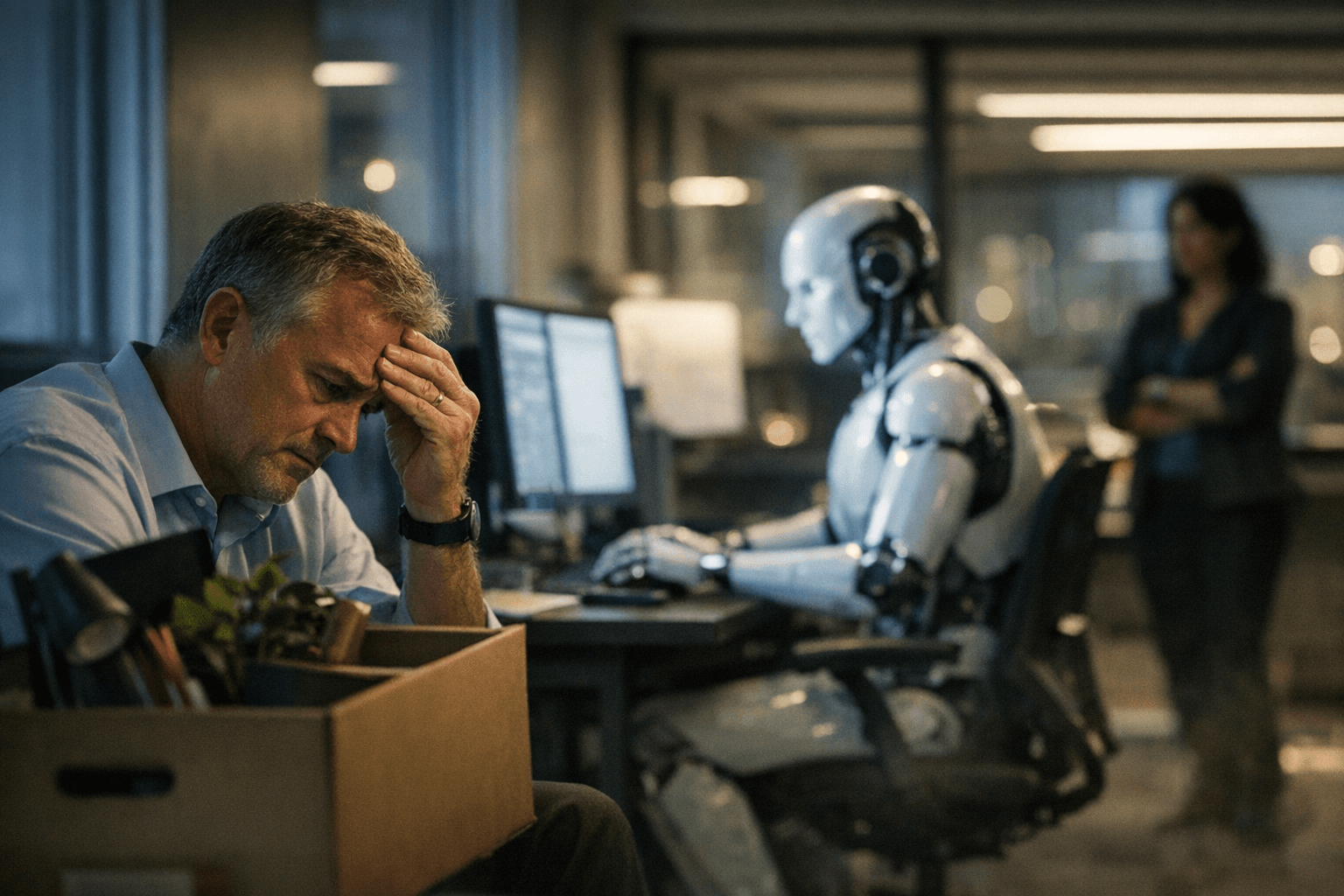

Goldman Sachs’ research has put a specific number on the labor risk of broad AI adoption: a 2025 report cited by analysts says “innovation related to artificial intelligence could displace 6-7% of the US workforce if AI is widely adopted,” and the bank expects the impact to be transitory. Market coverage on March 3, 2026, referenced that Goldman analysis, summarizing a baseline scenario of roughly 6% displacement as investors parsed the macro implications.

The bank’s multi-year view is more optimistic on productivity than on near-term growth. A 2023 Goldman Sachs Research estimate projected that “AI could increase US productivity growth by 1.5 percentage points annually assuming widespread adoption over a 10-year period.” Goldman economists forecast measurable GDP and labor productivity effects starting in 2027, a timeline that underpins the firm’s modeling of long-run benefits.

That future-facing forecast sits against a muted contribution from AI investment in 2025. Goldman Sachs chief economist Jan Hatzius said AI investments contributed “basically zero” to US economic growth in 2025. Analysts translated the contribution into numbers, noting US GDP grew 2.2% in 2025 and that only about 0.2 percentage points of that growth came from AI investment, a shortfall explained in part by heavy imports of AI equipment from Taiwan and South Korea.

The gap between heavy spending and immediate returns is stark. Industry projections cited by market analysts put tech company spending on AI infrastructure at $700 billion in 2026, yet profitability at scale remains elusive. MLQ Agent and MLQ Ai commentary highlight that the current period of heavy investment may not show returns until Goldman’s 2027 inflection point, raising questions about capital allocation and near-term corporate performance.

Analysts say several constraints will determine whether Goldman’s timeline proves accurate: “whether AI companies can achieve profitability at scale, whether domestic semiconductor manufacturing increases to reduce import dependency, and whether productivity gains actually materialize in practice,” MLQ Ai wrote. That analysis warned explicitly that “the lack of immediate returns raises the risk that capital allocation to AI infrastructure could be suboptimal if these future benefits fail to materialize at expected levels.”

For Goldman Sachs employees and business-line leaders, the numbers frame internal and client conversations. The firm’s forecasted 1.5 percentage-point productivity boost over a 10-year adoption period, the 6-7% workforce-displacement scenario from the 2025 study, Jan Hatzius’ “basically zero” description of 2025 impact, and the projected $700 billion in 2026 spending together present a policy and operational challenge: how to manage workforce transitions and supply-chain dependencies while betting on a productivity payoff that the bank expects to appear beginning in 2027.

The tension between large near-term investment and a delayed GDP impact makes the coming 12 to 24 months critical for companies and policymakers focused on domestic semiconductor capacity, workforce retraining programs, and metrics of AI profitability.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?