JPMorgan Tracks Junior Bankers' Hours, Pressuring Goldman on Talent Retention

JPMorgan's new pilot tracks junior bankers' keystrokes, video calls, and meetings weekly — and Goldman now has to decide if its own monitoring approach is enough to win the talent war.

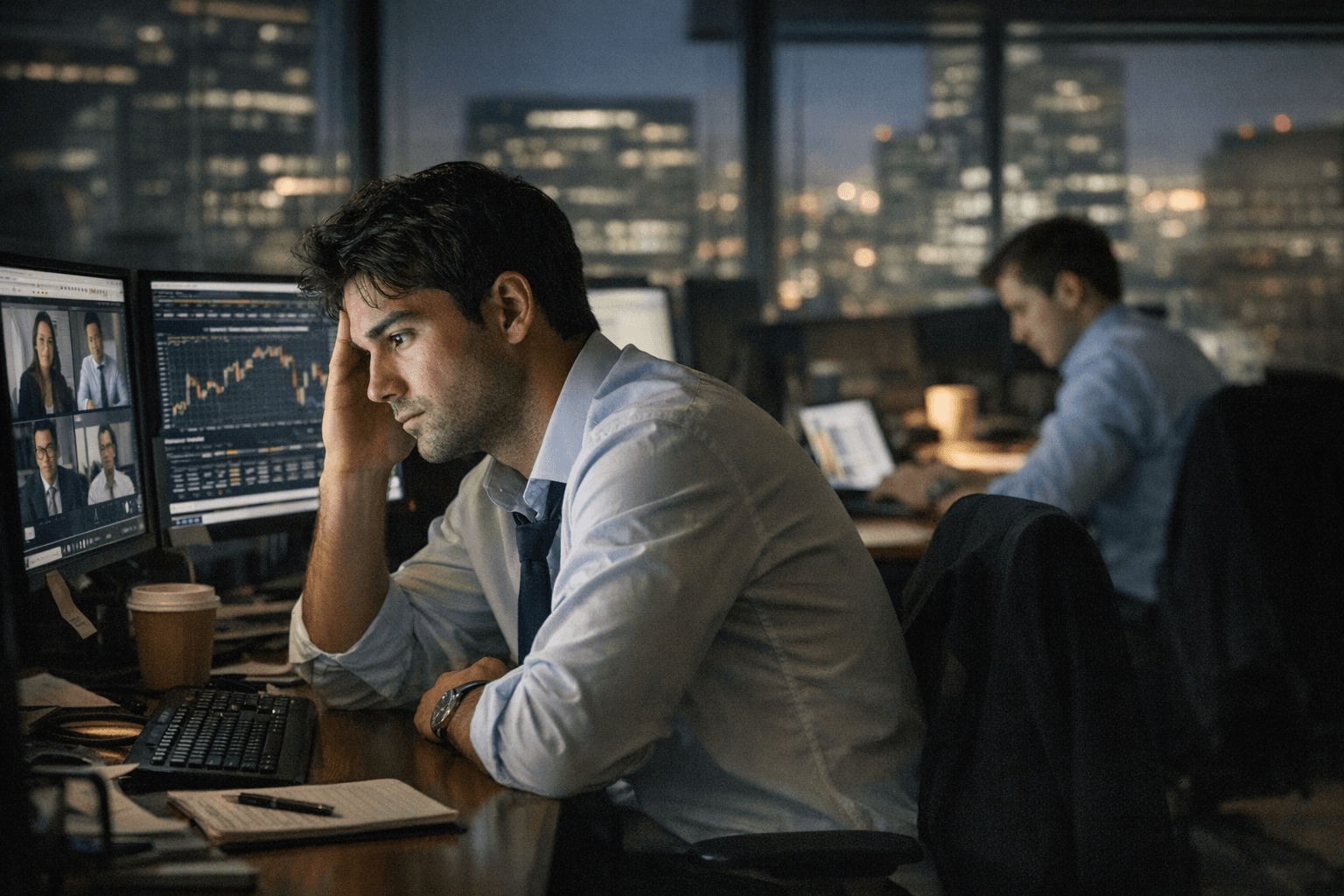

JPMorgan Chase launched a pilot program in mid-March 2026 to monitor the working hours of its junior investment bankers, matching hours they claim on time sheets against their digital activity. Each week, employees receive reports showing a comparison between their self-reported time and a figure derived from their computer footprint, including video calls, desktop keystrokes, and scheduled meetings. The bank plans to expand the program across its investment bank, and the move is already recalibrating how Goldman Sachs thinks about the arms race for junior talent.

JPMorgan's public framing is deliberate. "Much like the weekly screen time summaries on a smartphone, this tool is about awareness — not enforcement," JPMorgan said in a statement to the Financial Times. The tool won't be used for evaluation purposes, but is designed to provide a better estimate of employee workloads. Whether junior bankers at Goldman read that framing as reassuring or ominous is another matter.

Goldman is not a bystander here. The firm already runs its own internal monitoring, and its public position is measured: "Management monitors junior banker staffing and activity levels and regularly adjusts the workloads of our teams," the bank said in a statement. Goldman Sachs has been tracking employee work as well, though junior analysts have reported tensions with the surveillance system, with some calling it "inhumane" on the anonymous corporate message board Blind. The firm has at times asked junior bankers to take breaks when internal monitoring flagged high activity levels — a reactive mechanism rather than the proactive, data-sharing model JPMorgan is now piloting.

The distinction matters for recruiting. The rollout comes as major banks continue to navigate the long-standing tension between high compensation and demanding hours, where junior roles can pay as much as $200,000 early in a career. At Goldman, where prestige has historically served as its own retention mechanism, that logic is under pressure. The economics of junior banker retention are stark: by most estimates, it costs a major investment bank between $150,000 and $300,000 to recruit, train, and onboard a single analyst, factoring in recruiting events, interview processes, training programs, and lost productivity during ramp-up. When an analyst leaves after 18 months for a buy-side job, that investment walks out the door.

JPMorgan's pilot also arrives with a known flaw built in. The Financial Times, which first reported the program citing people familiar with the matter, noted that the system has inherent limitations: some junior bankers misreport their hours, often logging fewer than they actually worked to avoid being pulled from live deals or to stay eligible for new assignments. The monitoring technology can track keystrokes; it cannot change the incentive structure that makes under-reporting rational in the first place.

The industrywide reckoning with working hours accelerated after Leo Lukenas III, a Green Beret who joined Bank of America as an investment banker, died of a blood clot after working extremely long days. While the coroner's report did not establish a connection between his death and his workload, the case spurred renewed attention to overwork in investment banking. JPMorgan had already capped junior bankers' working hours at 80 hours a week in 2024, a policy layered on top of a "pencils down" period between 6 p.m. Friday and noon Saturday, and a guarantee of one full weekend off every three months, with live deals exempt. Bank of America, meanwhile, faced a 2024 Wall Street Journal investigation that found many junior bankers there were routinely told by superiors to lie about their hours to skirt limitations.

The Goldman context traces back further. In 2021, a group of 13 first-year Goldman Sachs analysts created an internal survey that leaked widely, revealing respondents were averaging 95 hours of work per week, sleeping roughly five hours a night, and reporting sharp declines in mental and physical health. The presentation became a flashpoint, forcing Goldman's leadership, including CEO David Solomon, to publicly acknowledge the problem.

Experts who study workplace surveillance are skeptical that monitoring alone closes that gap. "If employers genuinely want to reduce overwork, they need to go beyond surveillance and address job design, management capability and culture," said Haig, speaking to People Management. Chris Preston, founder and director of consultancy The Culture Builders, added a related concern: the additional monitoring of employees can create a culture that prioritizes presenteeism over output. Employee-monitoring tools, often referred to as "bossware," have become far more common across financial services, a shift accelerated by the rise of remote work during the pandemic. A Chartered Management Institute survey found that a third of all UK organizations are now using bossware technology to monitor staff.

For Goldman analysts and associates watching JPMorgan's rollout, the more immediate question is whether Goldman will follow with a comparably transparent system — one that shares the data with the employees being watched, rather than using it solely as a management lever. Goldman has already moved to launch a retention program aimed at keeping junior talent from defecting to private equity, as the recruitment timeline has compressed dramatically: PE firms that in 2010 typically waited about 11 months before approaching junior bankers now sometimes start recruiting within weeks of analysts starting work. Hours monitoring, framed correctly, could be another card to play. Framed incorrectly, it becomes one more reason to take the PE interview.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?