M&A Supercycle Brings Bigger Bonuses but Longer Hours for Bankers

Goldman's M&A head Stephan Feldgoise is seeing nearly double the deals in the $5B-$10B range; for bankers, that means bigger bonus pools and longer hours ahead.

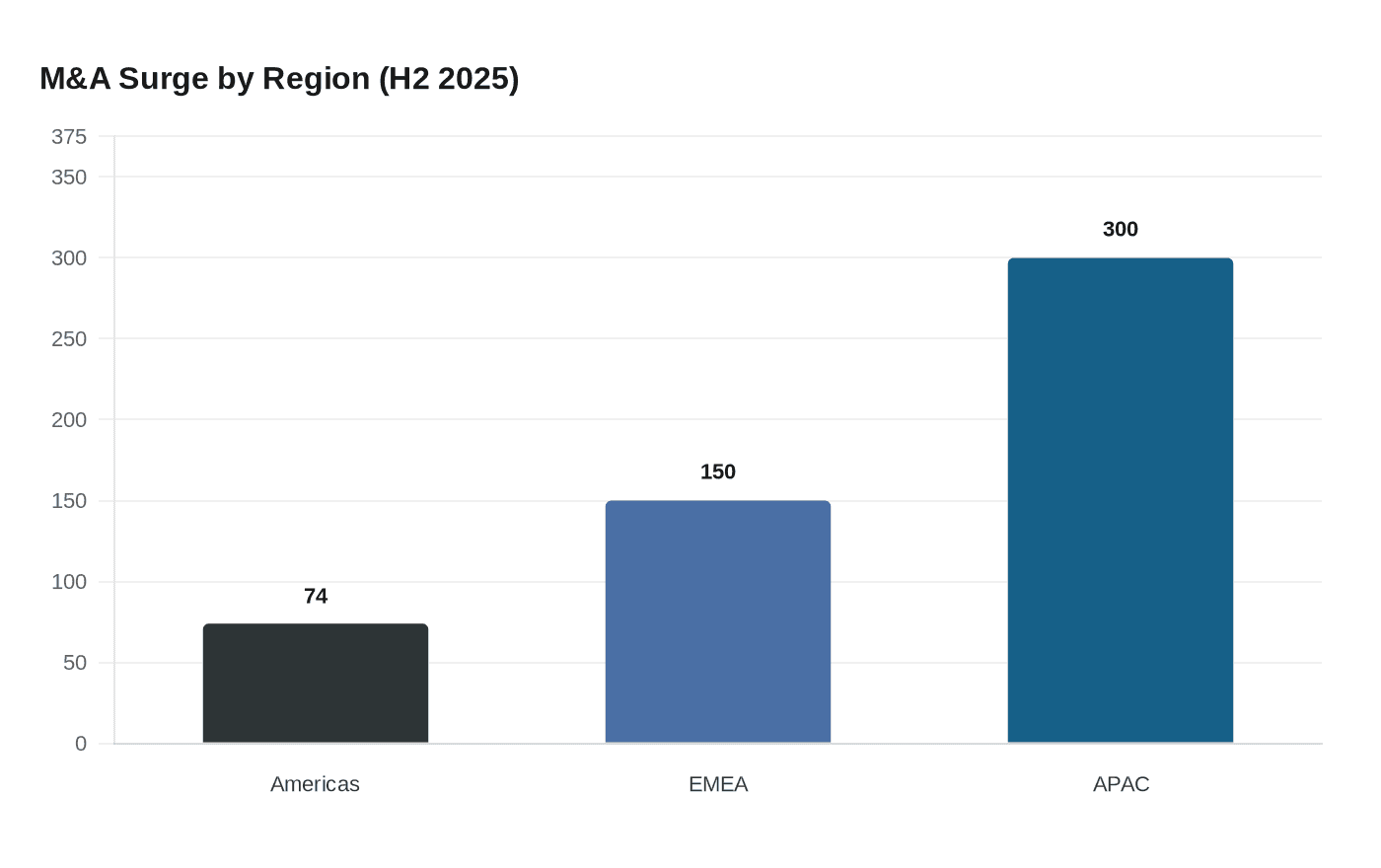

Wall Street's deal machine is running at a pace that Goldman Sachs's own head of global M&A, Stephan Feldgoise, described as rivaling the activity levels of 2021, a year many dealmakers thought was a once-in-a-generation peak. His case is grounded in hard data: globally, M&A volumes rose 40% year over year in the second half of 2025, with deals above $500 million surging 74% in the Americas, 150% in EMEA, and 300% in APAC. Feldgoise told Bloomberg TV he is seeing "almost double" the number of transactions in the $5 billion to $10 billion range, a cadence he compared to the deal cycles of the early 2000s and 2010s. Leveraged buyouts, he added, are at all-time highs.

For Goldman's advisory teams, the practical translation of those numbers is already familiar: longer hours, compressed deal sprints as closings cluster, and variable compensation pools that will grow if that pipeline converts into closed fees. The firm's advisory units are currently working a wave of $10 billion-plus megadeals concentrated in data centers and energy infrastructure, the sectors most directly exposed to the AI investment cycle. Goldman has forecast a 15% increase in U.S. M&A activity for 2026, and analysts tracking the firm project full-year earnings per share between $57.70 and $58.64, a figure that assumes advisory momentum holds through year-end.

The structural tailwinds backing that forecast are a softer regulatory posture in Washington, easing macro conditions, and what Feldgoise called "massive pools of capital" that are too large and too restless to stay sidelined. The AI-driven innovation supercycle is disrupting entire industries and broadening the rationale for strategic deals, accelerating consolidation among companies that might otherwise have spent another year watching from the sidelines.

For analysts and associates, the upside is real but uneven. Discretionary bonus pools for dealmakers are expected to be meaningfully stronger than in the trough years of 2023 and 2024, when the deal drought squeezed pools across the Street. Distribution, however, will skew sharply toward originators and execution stars. That makes deal attribution crediting, the internal accounting of who gets credit for bringing in and closing a mandate, consequential in ways it was not during slow years. Coverage, product, and execution roles should track those formal crediting systems carefully, because they determine how pools get divided across teams.

The staffing math also cuts differently depending on where you sit. In high-volume deal environments, banks historically pause front-office cost reduction while continuing to seek efficiencies in support and operational functions. Senior resources get pulled asymmetrically onto high-fee mandates, which can create workload imbalances across geographies and coverage groups. Teams covering sectors with the most active sponsor or strategic activity will feel the compression first.

There are episodic risks to this trajectory. Geopolitical shocks and commodity supply disruptions can accelerate and then abruptly stall deal cycles, creating volatility in both workload projections and year-end bonus expectations. The second-half calendar will tell most of the story: conversion of the current pipeline into closed transactions before December is what ultimately moves compensation outcomes, promotion timetables, and near-term attrition rates in high-demand coverage areas.

For junior bankers weighing a buy-side exit, the timing calculus has shifted. Elevated deal experience on large mandates, combined with stronger bonus numbers, improves marketability with private equity and growth funds. Supercycle windows tend to close faster than they open. League table rankings, announced sell-side mandates, and internal staffing communications over the next 60 to 90 days will be the clearest signals of how much of this momentum is holding.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?