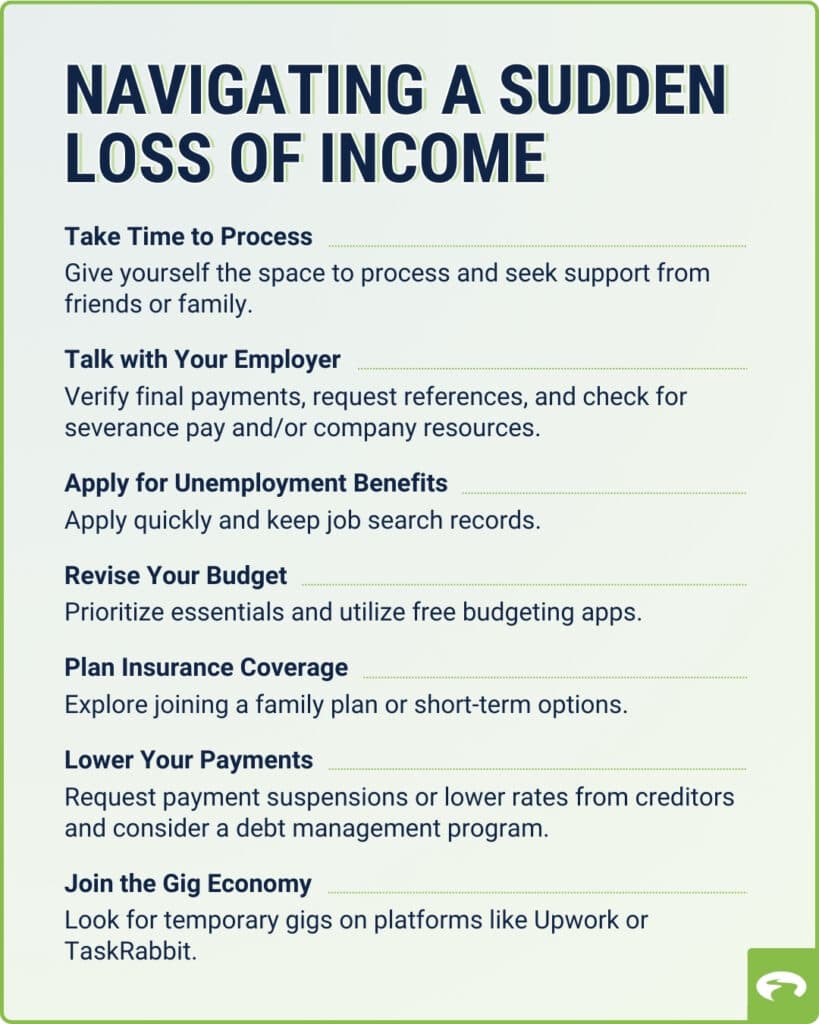

CFPB checklist helps KPMG workers navigate sudden job loss

A KPMG layoff turns urgent fast. The CFPB checklist helps workers protect cash, health coverage, and benefits before deadlines start costing money.

The first 72 hours decide how hard a layoff hits

A sudden job loss at KPMG is not just a career disruption. Within three days, it can affect cash flow, health coverage, severance paperwork, unemployment timing, and how much momentum you keep in your job search. The CFPB’s checklist works because it turns a disorienting event into a sequence of moves, and that matters in a firm where advisory demand can soften, audit staffing can shift, and professionals often assume the next busy season will look like the last one.

Waiting a week can be expensive. A delayed unemployment filing can push back the first payment, and for someone staring at a mortgage due date, rent deadline, or credit-card bill, that delay can be the difference between staying current and starting a spiral of late fees. The point of the checklist is not reassurance. It is triage.

Start with the money that arrives, and the money that stops

The first task is to file for unemployment as quickly as possible. The CFPB says unemployment benefits are typically weekly payments of a few hundred dollars, and those payments are taxable income. The U.S. Department of Labor says unemployment insurance is a joint state-federal program, with each state administering its own system, and eligibility usually depends on being unemployed through no fault of your own and meeting state wage and work requirements.

That state-by-state structure matters more than many workers realize. USAGov says there is no federal unemployment program, and claims should be filed in the state where you worked. For KPMG employees who may have moved between offices, projects, or client sites, that detail can be easy to miss in the first fog of a layoff. Filing in the right state, and filing immediately, helps avoid losing days of benefit time you cannot get back.

The practical move in the first 72 hours looks like this:

- File for unemployment right away in the state where you worked.

- Save every layoff-related document, including separation letters and severance terms.

- List the next 30 days of bills in order of urgency, starting with housing, utilities, and transportation.

- Stop nonessential spending before it becomes a habit.

That sequence is dull, but it is the difference between a controlled transition and a cash crunch.

Treat health coverage as a deadline, not a background task

Health insurance can become one of the most expensive surprises after a layoff. The CFPB notes that coverage can usually continue at the worker’s own expense, which sounds manageable until the monthly bill lands next to unemployment income that is often only a few hundred dollars a week. For many people, the better move is to look immediately at other coverage options rather than assume the old plan is the only bridge.

HealthCare.gov says losing job-based coverage opens a special enrollment period for a Marketplace plan, and you generally have 60 days to apply. Coverage can begin on the first day of the month after job-based coverage ends. That timing gives KPMG workers a narrow but workable window to compare a Marketplace plan with COBRA and with a spouse’s or partner’s employer coverage, if that option exists.

Massachusetts is the big exception in the national landscape. The Massachusetts Division of Unemployment Assistance says the state is the only one in the country with a health care plan for unemployment insurance claimants. That does not change the general rule for most KPMG workers, but it is a reminder that state rules can materially change the safety net. For anyone separated from a Boston or other Massachusetts office, that difference is not trivia. It affects real monthly costs.

Use the layoff to reprioritize debt and benefits, not just the job search

The CFPB’s checklist specifically calls out rent or mortgage payments, student loans, bills, spending, credit, and retirement savings. That is the right order because a layoff is not just a work problem. It is a full financial transition, and the first few days are when workers are most likely to make expensive mistakes out of stress.

Housing comes first because the consequences of missing a payment are immediate and hard to unwind. Student loans need a separate look because the relief options are not the same as for rent or utilities, and some borrowers can benefit from understanding what happens before they miss a payment. Retirement savings should be reviewed before anyone moves money around impulsively, because a rushed rollover or cash-out can create taxes, penalties, and a long-term hole just as the job market gets uncertain.

For KPMG professionals, that discipline matters even more because compensation is often layered with deferred incentives, promotion timing, and the possibility of moving back onto a client team quickly. A layoff can tempt people to treat the event as temporary and postpone the boring admin work. That is exactly when the most damage happens.

Know what the unemployment rules actually say

Unemployment insurance sounds universal, but it is not. The U.S. Department of Labor says each state runs its own program, and USAGov is explicit that there is no federal unemployment program that works the same way everywhere. The common thread is that benefits generally go to people who lost work through no fault of their own, not to workers who quit voluntarily or were dismissed for misconduct.

That distinction is especially important in professional-services environments, where people may leave because a role changed, a team was restructured, or work was cut back. If the separation was effectively a layoff or job elimination, the unemployment filing deserves immediate attention. If there is any uncertainty, the separation paperwork and state rules become the deciding documents, not office chatter or assumptions from colleagues.

A week of delay can also create a second problem: it can slow the entire recovery rhythm. The earlier a worker files, the earlier the administrative clock starts, and the faster the first check can arrive. In a profession built around deadlines, that administrative lag is often the first real financial hit.

Why this lands differently inside KPMG

The urgency is not abstract. Bloomberg Tax reported that KPMG told partners it planned to cut about 10% of its U.S. audit partners, and earlier reporting said the firm had already eliminated 195 audit jobs in the prior fall to address low turnover. The firm has also been trimming U.S. advisory roles amid weaker demand. Even if the total number of affected employees is small relative to the whole firm, the shock lands hard because Big Four jobs are often sold as stable, structured, and promotion-driven.

That is why a layoff checklist matters in a firm like KPMG. People do not just lose a paycheck. They lose the cadence of busy season, the internal visibility that supports promotion, and the assumption that the next review cycle will reset the story. A fast response protects cash, preserves health coverage options, and keeps the job search moving before panic takes over.

The real lesson is simple: a layoff is not a single event, it is a countdown. The workers who act in the first 72 hours keep more options open, lose less money to avoidable delays, and put themselves in a better position to land the next role before the gap becomes bigger than it needed to be.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)