IRS guidance lets KPMG workers get retirement match on student loan payments

KPMG workers paying down student debt could be missing out on employer match money if the firm’s plan allows it. The IRS just made that design clearer.

Employees at KPMG who are sending cash to student lenders instead of a 401(k) may still be able to capture the company match, if the firm’s plan is designed to credit those loan payments. That is the overlooked compensation angle in new IRS guidance: student debt no longer has to mean forfeiting retirement dollars.

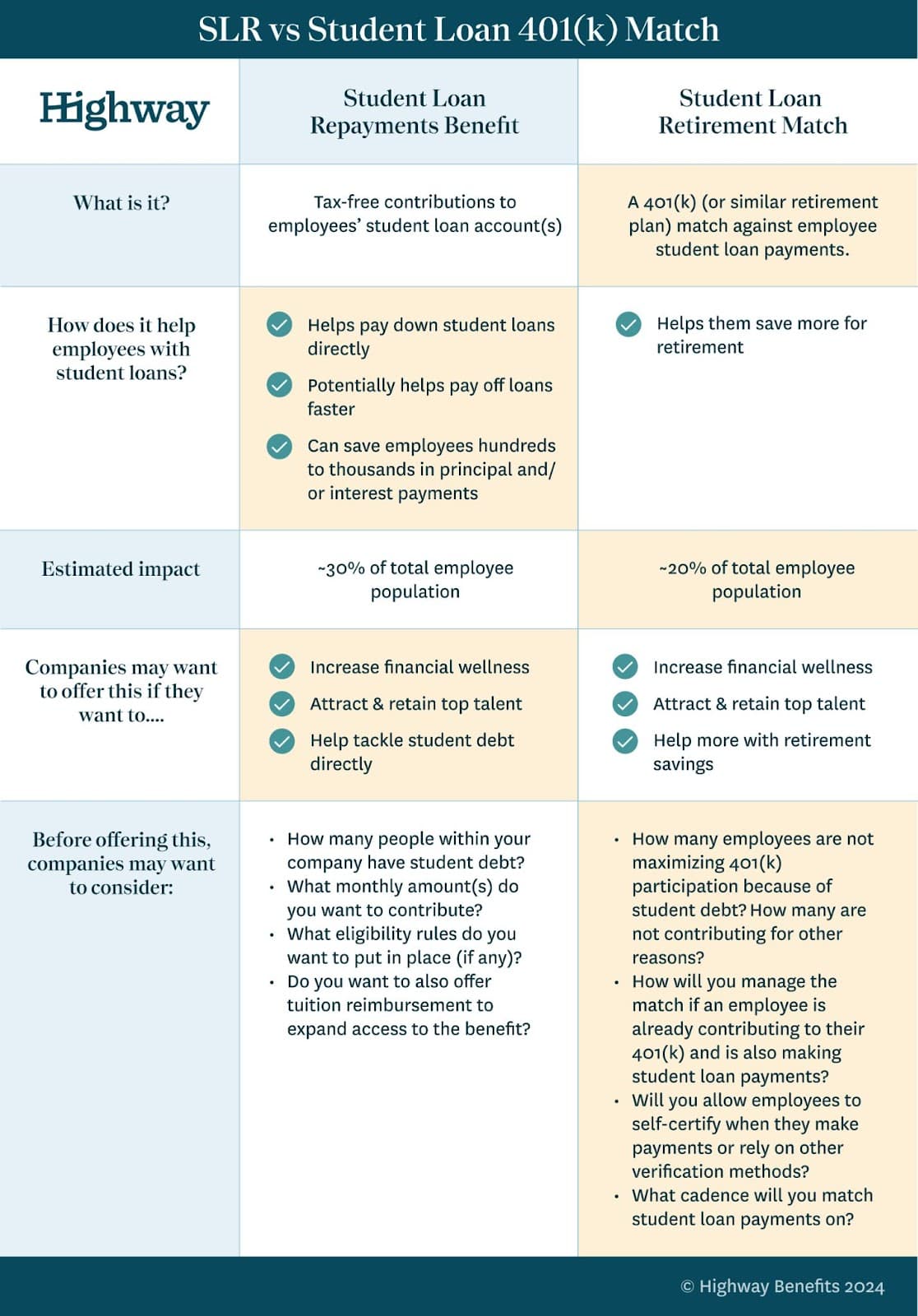

IRS Notice 2024-63 says employers may make matching contributions based on qualified student loan payments under 401(k), 403(b), SIMPLE IRA and governmental 457(b) plans. The feature is optional, not mandatory, and it applies to contributions made for plan years beginning after Dec. 31, 2023. The IRS issued the interim guidance on Aug. 19, 2024, in IR-2024-217, while Treasury and IRS move toward proposed regulations.

For KPMG’s early-career consultants, audit staff and analysts, the timing matters. Federal student loan payments resumed in October 2023 after more than three years of pause, and the U.S. Department of Education held about $1.5 trillion in federal loans for nearly 43 million borrowers as of January 2024. The Federal Reserve said most borrowers with outstanding student debt owed less than $25,000, and the median amount of education debt among people with any outstanding debt for their own education was between $20,000 and $24,999. That is a lot of people carrying manageable but still monthly-decisive balances, especially in the first years of Big Four life.

The guidance did not appear out of nowhere. The American Retirement Association asked the IRS for student-loan match rules in January 2024, and later said many of its recommendations showed up in the final guidance. Benefits consultants say employers can need six to 12 months of planning to implement the feature, because administration is not as simple as flipping a switch. Some plans may rely on payroll-period tracking or employee self-certification to confirm qualified student loan payments, while others may use a vendor or annual true-up process.

KPMG has already framed retirement design as part of employee financial wellbeing, including the idea that workers should not have to choose between paying student loans and saving for retirement. The firm’s retirement materials have included a traditional 401(k) plan and later the KPMG 401(k) Capital Accumulation Plan, making this a live workplace issue rather than a distant policy point.

The practical stakes are real. A 2024 impact report from a student-loan match provider found a 13.5% increase in first-time retirement-plan participation and a 27% increase in employees maximizing the employer match. For a firm built on up-or-out promotion cycles and heavy busy-season pressure, that kind of design can shape who builds savings early and who leaves money on the table.

KPMG employees should ask whether the retirement plan offers a student-loan match, how the matching formula works, what documentation is required, whether payroll tracking or self-certification is accepted, and whether the match is handled as a per-pay-period credit or with a year-end true-up. The law now allows the feature. The question for workers is whether their plan makes it usable.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)