KPMG workers weigh HSA versus FSA as 2026 limits shift

The wrong election can quietly shave money off your paycheck. For KPMG workers, 2026 HSA and FSA limits make the trade-off bigger, especially if you change roles or plans later.

Why this is really a pay decision

At KPMG, the HSA versus FSA choice is not a small benefits formality. It is one of those enrollment decisions that can quietly change how much of your compensation you keep, especially if you work unpredictable hours, move teams, or expect your medical needs to shift during the year.

The hidden cost shows up in different ways. An FSA can leave you racing to spend every last dollar before year-end, while an HSA can turn the same paycheck deduction into a portable reserve that stays with you if you leave the firm. For consultants, auditors, and advisory professionals who live through busy season, promotion cycles, and project changes, that difference matters more than the sticker price of the health plan.

The HSA: the account that keeps working after the year ends

HealthCare.gov says an HSA lets you set aside pre-tax money for qualified medical expenses, including deductibles, copayments, and coinsurance. It is generally paired with a high-deductible health plan, and the money stays with you even if you leave your employer. That portability is the big advantage for KPMG workers who may change roles, offices, or even firms before the next benefit year rolls around.

The 2026 limits make the long-term case for HSAs even clearer. The Internal Revenue Service set the annual HSA deduction limit at $4,400 for self-only coverage and $8,750 for family coverage. For workers with higher and less predictable medical spending, that is a meaningful amount of tax-advantaged space, especially if an employer contributes too. Over time, the account can function like a healthcare buffer rather than just a reimbursement tool.

HSAs also fit professionals who want flexibility. If you are healthy now but expect a surgery, fertility treatment, or a child’s recurring prescriptions later, money in an HSA can sit and grow instead of being forced out by the calendar. That is where the account becomes more than a tax break. It becomes a way to smooth out the financial spikes that hit during busy season, during a family transition, or right after a job move.

The FSA: useful for budgeting, but less forgiving

An FSA works differently. An employer may offer a health flexible spending arrangement that lets you pay for certain out-of-pocket medical costs with pre-tax dollars, but the money is tied to the employer plan and usually follows a use-it-or-lose-it logic. For 2026, the health FSA salary-reduction limit is $3,400, and some plans may allow a carryover up to $680, but only if the employer’s plan permits it.

That is why the wrong FSA election can become a quiet loss. If you set aside too much for predictable care and your spending comes in lower than expected, the leftover money may be partially forfeited or capped by a small carryover. For a worker who overestimates routine doctor visits or prescriptions by a few hundred dollars, that is not a theoretical drawback. It is money that can disappear from the paycheck you already earned.

FSAs make sense when your medical costs are steady and easy to forecast. They can work well as a budgeting tool for workers who know they will use the money within the plan year. But they are much less forgiving for people with changing schedules, uncertain family expenses, or the kind of travel-heavy client work that can make healthcare plans harder to predict.

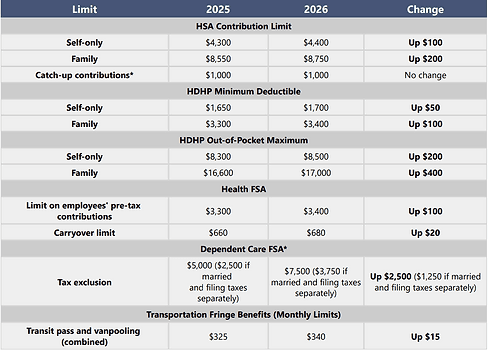

The 2026 numbers that should shape enrollment

The new federal limits are what turn this from a general benefits choice into a hard math problem.

- HSA contribution limits for 2026: $4,400 for self-only coverage and $8,750 for family coverage.

- HDHP minimum deductible for 2026: $1,700 for self-only coverage and $3,400 for family coverage.

- HDHP maximum out-of-pocket limit for 2026: $8,500 for self-only coverage and $17,000 for family coverage, excluding premiums.

- Health FSA salary-reduction limit for 2026: $3,400.

- Health FSA carryover maximum for 2026: $680, if the plan allows carryovers.

Those numbers tell the story plainly. A family HSA can shelter $5,350 more pre-tax than an FSA can in 2026, before even considering any employer contribution or long-term savings behavior. If your household expects meaningful healthcare spending, that gap can compound into real value. If your plan is a bad fit, the loss can be just as concrete.

HealthCare.gov also says all 2026 Bronze and Catastrophic Marketplace plans are HSA-eligible. That matters if you are comparing coverage outside KPMG or thinking through a spouse’s plan, because HSA eligibility is not just about one employer’s menu. It is about whether the coverage structure lets you build the account at all.

Three KPMG worker profiles show the trade-off

A second-year auditor heading into busy season may not know whether the year will bring a dentist bill, an urgent care visit, or nothing at all. For that person, an HSA can be the better hedge because unspent money rolls forward and stays portable. An FSA may look attractive if the spending is obvious and near-term, but it creates a deadline that can be awkward when client work swallows the week and a medical appointment gets delayed.

A manager in advisory with family coverage faces a different calculation. The household may already be juggling childcare, prescriptions, and recurring appointments, which makes the higher 2026 HSA limit especially valuable. The family HSA limit of $8,750 can absorb a lot more tax-advantaged spending than the $3,400 FSA cap, and the account does not disappear if the manager changes teams or takes a different role later in the partner-track journey.

A consultant who expects a planned procedure later in the year may like the certainty of the FSA, especially if the spending amount is known. But that worker should treat the election as close to irreversible for the year. If the estimate is off, the worker is left managing the downside, not the firm.

KPMG’s benefits package gives context, but not a free pass

KPMG’s own benefits pages show the firm leans into flexibility. In Canada, employees have access to a Health Spending Account and a customizable Wellness Pool. In the United States, KPMG has also expanded mental-health support, including 10 free counseling sessions per issue per year. The firm’s broader benefits messaging also points to family-building support and flexible work arrangements.

That matters because it shows KPMG is selling benefits as part of a personalized total rewards package, not a one-size-fits-all plan. But a flexible philosophy does not erase the hard arithmetic of enrollment. The account you choose still determines how much you can shelter from tax, how quickly you must spend it, and whether the money follows you if you leave.

The practical rule is simple. Choose an FSA if your spending is steady and you are confident you will use it. Choose an HSA if you want portability, long-term tax sheltering, and a better fit for unpredictable care. In a firm where compensation, workload, and career timing can all move at once, the wrong choice is not just a benefits mistake. It is a pay decision you feel later.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)