India’s auditor cooling-off plan could raise compliance costs 30%

A three-year lockout on post-audit consulting could force KPMG to redraw client handoffs, trim cross-selling and spend more on independence checks across India.

The proposed cooling-off rule would do more than narrow a legal window for auditors. For KPMG’s audit, tax and advisory teams in India, it would redraw how a client is won, staffed and monetized after the audit sign-off, and it could push compliance costs for domestic companies up by 20% to 30%.

The Corporate Laws (Amendment) Bill, 2026, introduced in late March, proposes a three-year cooling-off period that would bar auditors from providing non-audit services after their tenure ends. That means the usual bridge from statutory audit into consulting, tax support or other advisory work for the same client would become much harder to cross. For firms built on long-running account relationships, the rule would force a cleaner split between the audit book and the rest of the commercial pipeline.

The pressure point is not just abstract independence policy. Section 144 of the Companies Act, 2013 already bars auditors from nine categories of non-audit services during the audit relationship, including accounting and bookkeeping, internal audit, design and implementation of financial information systems, actuarial services, investment advisory and investment banking services, outsourced financial services and management services. The new proposal would extend that separation beyond the audit term itself, which would affect how KPMG teams hand off clients, how partners set cross-selling targets and how quickly advisory leaders can approach former audit clients.

That shift would land hardest on audit partners, sector teams and independence officers who manage large accounts across service lines. It would also change how managers think about promotion and book-building. A high-performing audit team that once created a clear path into tax or advisory revenue on the same client could see that route blocked for three years, forcing the firm to look harder for new business outside the audit relationship.

Industry reaction has been skeptical. Audit firms have said the proposed post-tenure ban is unusual, potentially anti-competitive and likely to raise audit costs and reduce client choice. ICAI, by contrast, has said the tighter restrictions on audit and non-audit services for related entities are largely aligned with its Code of Ethics and the Companies Act framework. The split underscores the tension KPMG and its peers are now managing: independence is becoming both a compliance obligation and a commercial constraint.

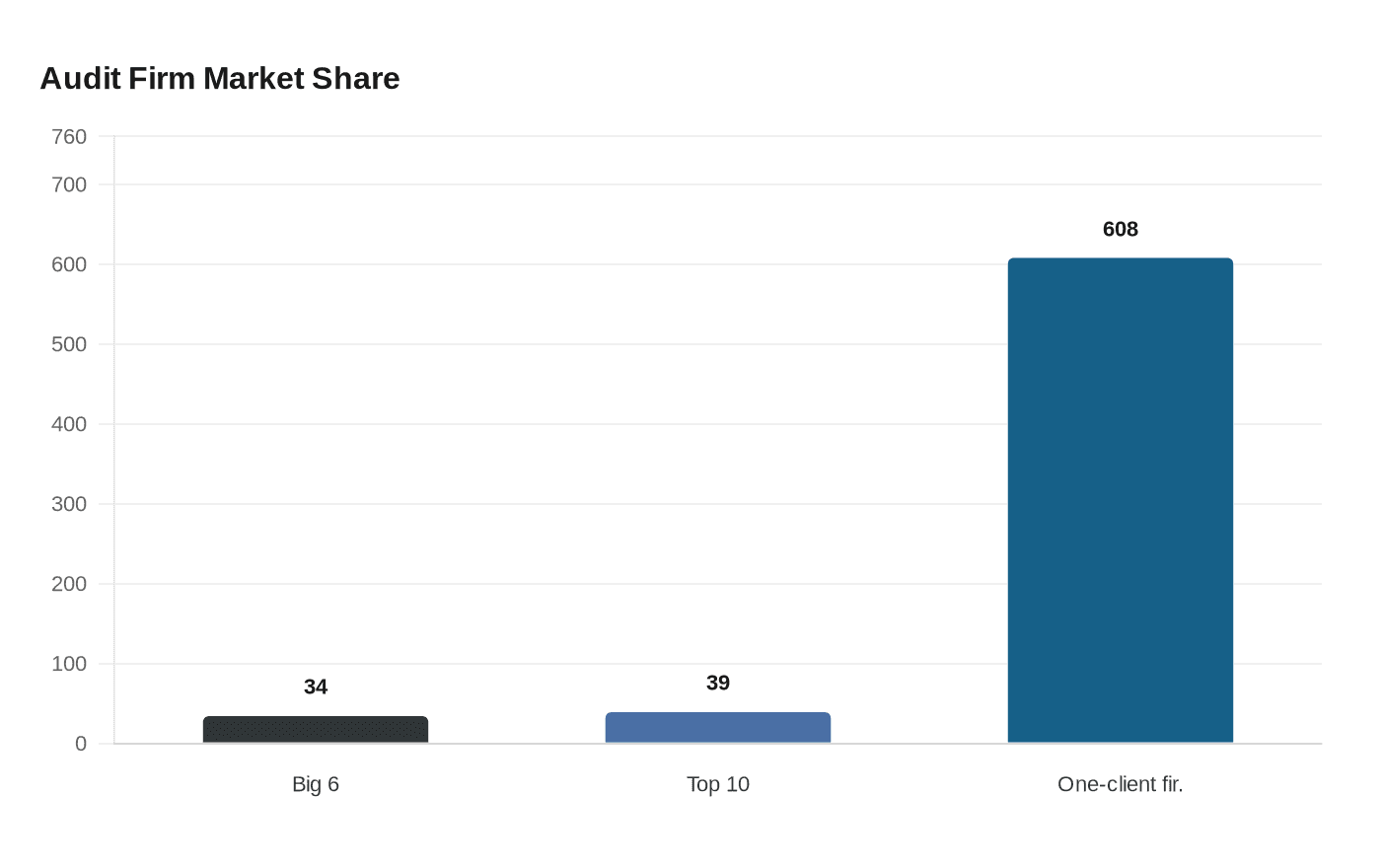

The market structure makes that tension sharper. Prime Database data showed that in FY25 the Big 6 audit firms handled 694 of 2,069 NSE main-board listed companies, or 34%, while the top 10 firms handled 803 companies, or 39%. At the same time, 608 audit firms handled just one listed company each. In that kind of market, a tighter post-audit ban could deepen concentration around the biggest firms while making it even harder for smaller competitors to move up the ladder.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)