IRS 2026 retirement rules change KPMG catch-up contribution strategies

Higher-paid KPMG employees near retirement may see catch-up dollars move to Roth and lose the pre-tax break that once softened payroll. The biggest flashpoint is the $150,000 wage test for age 50-plus savers.

Why this rule hits paychecks, not just retirement math

The IRS’s 2026 retirement limits change the cash flow picture for a slice of KPMG’s workforce that often has the most at stake: senior managers, directors, and partners who are trying to catch up late in their careers. If your prior-year wages with KPMG exceeded $150,000 and the firm’s plan offers Roth features, the extra catch-up dollars may have to go in on a Roth basis, which means less immediate tax relief and a different take-home-pay pattern. That is not a small technical tweak. It changes how much lands in your paycheck now, not just how much compounds decades from now.

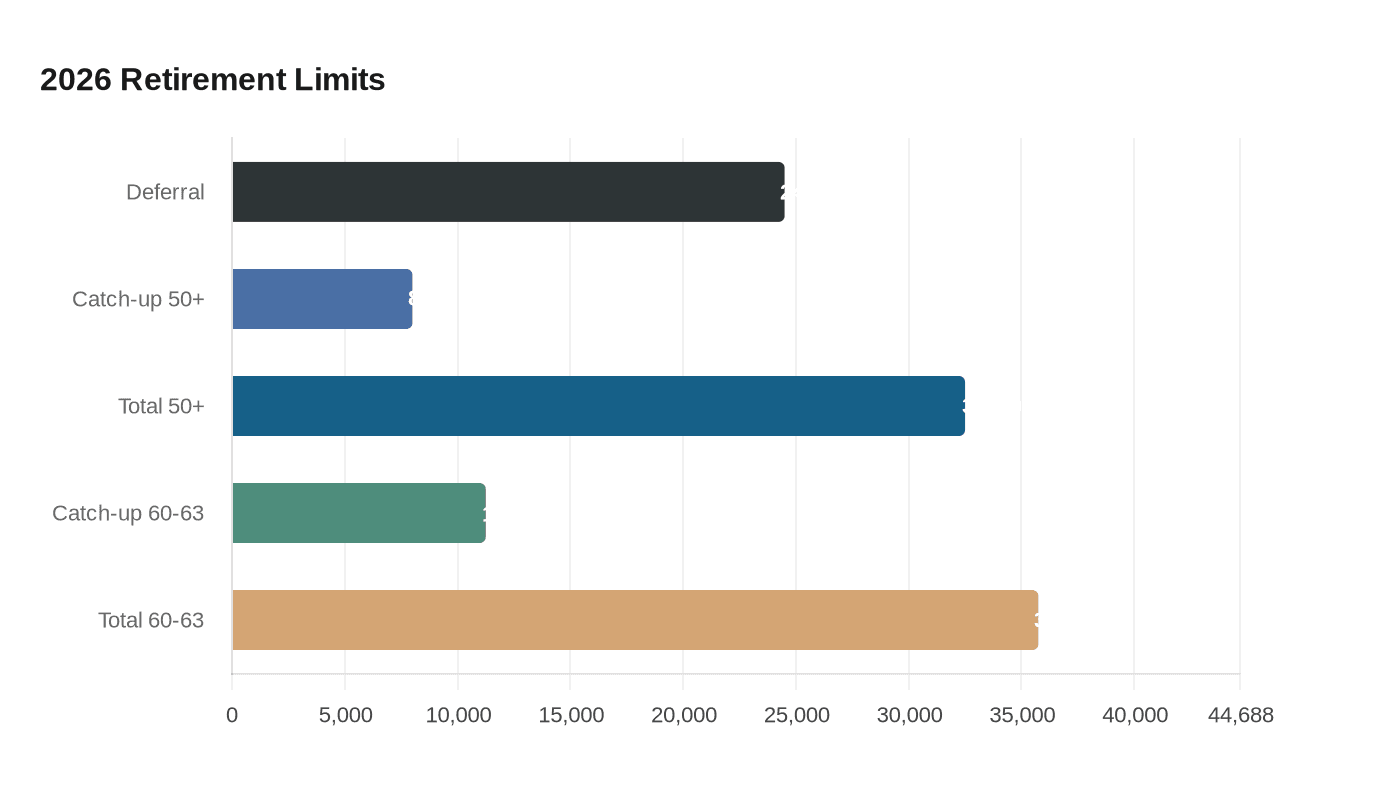

For 2026, the basic elective deferral limit for 401(k), 403(b), governmental 457, and Thrift Savings Plan accounts is $24,500. The general catch-up limit for participants age 50 and over is $8,000, which puts many workers at a combined annual ceiling of $32,500. For people who turn 60, 61, 62, or 63 in 2026, the higher catch-up limit rises to $11,250, pushing the total to $35,750 in most applicable employer plans. In a profession where bonus timing, promotion cycles, and busy season already make cash planning hard, those numbers matter immediately.

Who should pay attention at KPMG

This rule is aimed squarely at higher-paid professionals who are still working through the last stretch of their careers. At KPMG, that includes people on the partner track, long-tenured advisory leaders, audit managers approaching director, and senior staff who spent earlier years paying for family expenses, student debt, or the costs that come with mobility in a Big 4 career. If you are 50 or older, the catch-up window is already important. If you are 60 to 63, it becomes even more powerful.

The wage test is more specific than many employees realize. The IRS says the $150,000 threshold is based on prior-year wages with the plan sponsor, not a broader estimate of total compensation. For KPMG professionals, that means the relevant number is tied to what the firm paid you, not to outside income, household income, or a rough sense that you are “probably above the line.” That distinction can decide whether your catch-up dollars stay pre-tax or become Roth.

What changes in the payroll experience

The biggest practical shift is timing. Traditional pre-tax catch-up contributions reduce taxable income today, which can lower withholding and make each paycheck feel a little larger. Roth catch-up contributions do the opposite in the short term: you pay tax up front, take the hit in current cash flow, and get the tax-free withdrawal treatment later if the rules are met.

That is why this is more than a retirement-planning footnote. If you are already balancing student loans, mortgage payments, child-care costs, or HSA funding, a Roth-only catch-up election can change the monthly budget. For someone near retirement, the decision is not simply whether to save more. It is whether to accept higher current taxes in exchange for more flexible tax treatment down the line.

How the KPMG plan fits into the rule

KPMG’s 401(k) Summary Plan Description says the KPMG 401(k) Plan gives employees and partners the ability to save on a tax-deferred basis or through after-tax contributions, including Roth 401(k) contributions. That matters because the Roth catch-up rule does not force KPMG to invent a new savings vehicle from scratch. It pushes some employees into a different tax bucket within a menu the plan already offers.

KPMG has also summarized the IRS’s 2026 guidance and noted that participants age 50 and older in most 401(k), 403(b), governmental 457, and federal Thrift Savings Plan arrangements generally can contribute up to $32,500 in 2026. For KPMG professionals, the real question is not whether the contribution cap exists. It is how much of that cap will be pre-tax, how much will be Roth, and how payroll will classify the catch-up portion before elections are locked in.

The compliance clock is already moving

The IRS issued final regulations on the Roth catch-up rule on September 15, 2025. The agency says those rules generally apply to contributions in taxable years beginning after December 31, 2026, while the transition period under Notice 2023-62 generally ended on December 31, 2025. That timeline helps explain why 2025 was a systems year for employers, with payroll updates, employee communications, and plan document revisions all moving in the background.

SECURE 2.0, enacted in December 2022, set this sequence in motion, but the employer-side mechanics are what will shape the employee experience. An Aon Pulse Survey on SECURE 2.0 Roth catch-up contributions, based on 268 organizations, found employers gearing up for changes in payroll, communications, and administration. In plain terms, this is not just a personal finance issue. It is a plan-sponsor operations problem that reaches directly into how KPMG runs deductions for senior people.

What to decide before payroll elections lock in

The safest move is to treat this as a payroll decision before it becomes a year-end scramble. If you are eligible for catch-up contributions, review your age, your prior-year KPMG wages, and whether the plan’s Roth feature triggers the new rule. Then decide whether the current mix of pre-tax and Roth still fits your tax picture.

A few checks belong on the list:

- Confirm whether your KPMG account is subject to Roth catch-up treatment.

- Verify whether your prior-year wages with KPMG were above $150,000.

- Decide whether you want the immediate tax deduction from pre-tax deferrals or the future tax treatment of Roth.

- Revisit the choice early, before busy season and year-end deadlines make the change harder to process.

- Run a retirement projection that includes near-term withholding, not just long-term account growth.

The IRS is also drawing a contrast with simpler retirement arrangements. For SIMPLE plans, the 2026 catch-up limit is $4,000, and the age 60-to-63 SIMPLE catch-up limit is $5,250. Those lower amounts show how differently the law treats smaller plans versus the larger employer plans that matter to KPMG’s professional ranks.

The bottom line is straightforward: for many KPMG employees, the new rule is less about a retirement headline than about the amount that clears payroll every two weeks. Higher earners who want to maximize catch-up saving should check their elections early, because once the year advances, the tax treatment of those dollars is harder to change.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)