Roper raises profit forecast as AI demand lifts software confidence

Roper’s higher forecast says AI demand still rewards software that saves time, not just software that talks about AI.

Roper Technologies’ stronger profit outlook is a reminder that the AI cycle is not crushing software evenly. The companies still winning are the ones buyers can justify on the basis of time saved, routine work automated and operational results that are easy to measure.

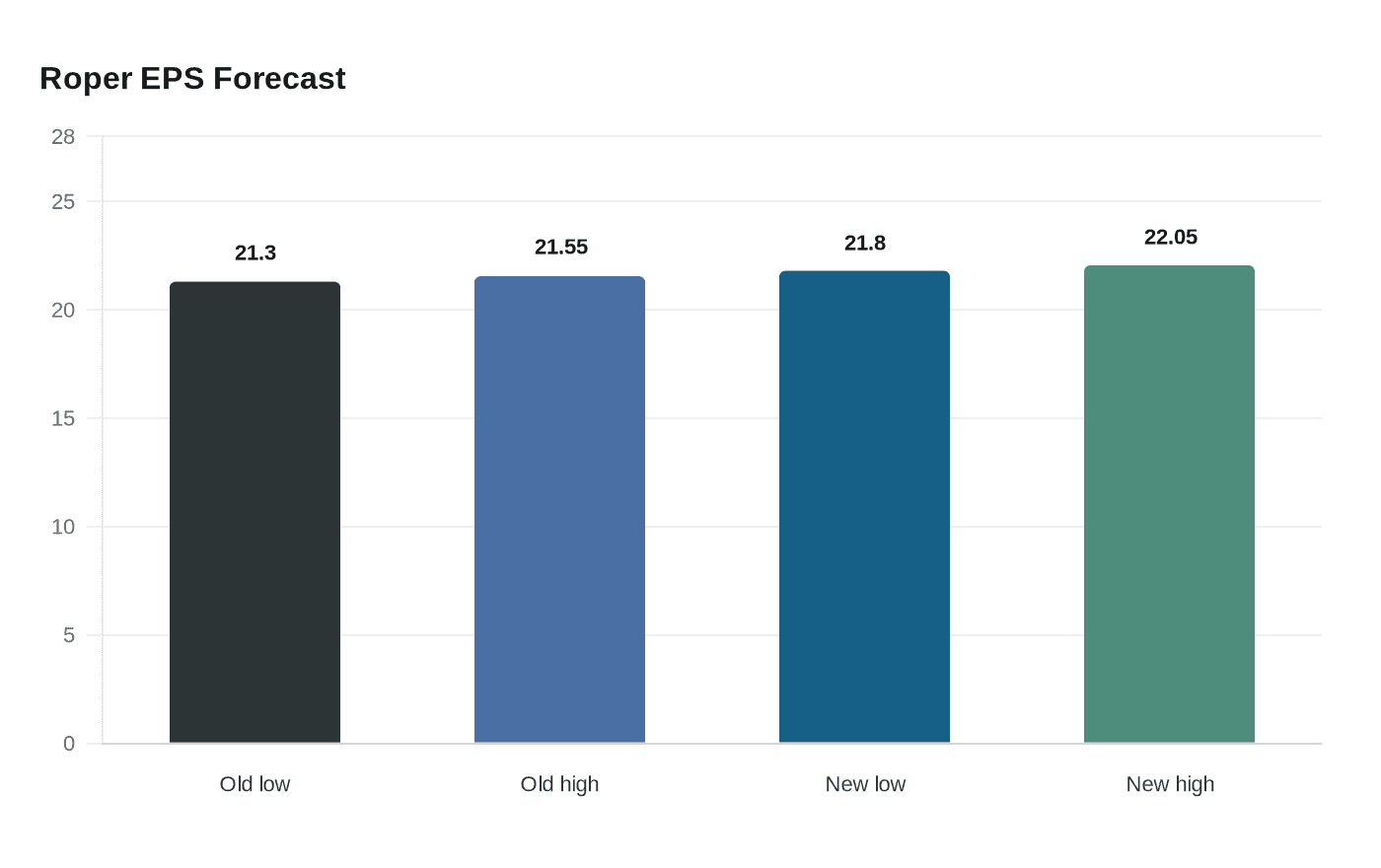

Roper raised its 2026 adjusted earnings forecast to $21.80 to $22.05 per share from $21.30 to $21.55 after first-quarter revenue reached $2.10 billion, up 11% from a year earlier. Management said demand stayed steady and AI adoption was gaining momentum across its customer base, while its businesses continued shipping AI products. Roper also repurchased 4.3 million shares for $1.5 billion in the quarter and said it had $3.8 billion of remaining buyback capacity after adding another $3 billion authorization.

That is the kind of signal monday.com employees should pay attention to. For a company built around work management, CRM, service and dev workflows, the market is increasingly rewarding proof that software actually cuts down manual work. monday.com has been leaning into that message, describing itself in investor materials as an AI work platform that helps manage and orchestrate work across more than 250,000 customers worldwide.

The numbers behind that pitch have been solid. monday.com said fourth-quarter 2025 revenue rose 25% year over year to $333.9 million, while full-year revenue climbed 27% to $1.232 billion. It also said fiscal 2025 non-GAAP operating margin was 14%, monday vibe was the fastest product in company history to pass $1 million in annual recurring revenue, and customers with more than $50,000 in ARR accounted for 41% of total ARR at the end of the year. Co-CEOs Roy Mann and Eran Zinman said the company was expanding its product portfolio and making progress upmarket as larger customers standardized on monday.com for mission-critical workflows.

But the market’s AI enthusiasm has not translated into a free pass. In February, monday.com guided first-quarter revenue to $338 million to $340 million and full-year 2026 revenue to $1.452 billion to $1.462 billion, below expectations, and the stock fell about 21% even after the company beat quarterly earnings and revenue estimates. Zinman said the company was not seeing an impact from AI companies and was shifting messaging to be more AI native.

That split is the lesson for operators and buyers: generic AI branding is not enough. The software businesses that keep confidence in an AI cycle are the ones that can show steady demand, credible product adoption and a direct line from features to saved labor, retained customers and better margins.

Know something we missed? Have a correction or additional information?

Submit a Tip