Nintendo’s blockbuster appeal clashes with investor doubts before May 8 earnings

Nintendo’s fans are still buying in force, but Wall Street is punishing the stock anyway. The gap puts fresh pressure on Shuntaro Furukawa and the teams behind Switch 2.

A brand that still sells, and a market that still doubts it

Nintendo has a rare problem: its products remain hugely popular, yet investors keep asking whether the growth can last. That tension is the real story heading into the company’s next earnings release on Friday, May 8, 2026, because the stock debate is no longer about whether Nintendo can make a hit console. It is about whether the company can turn that hit into a durable earnings story that survives beyond the launch window.

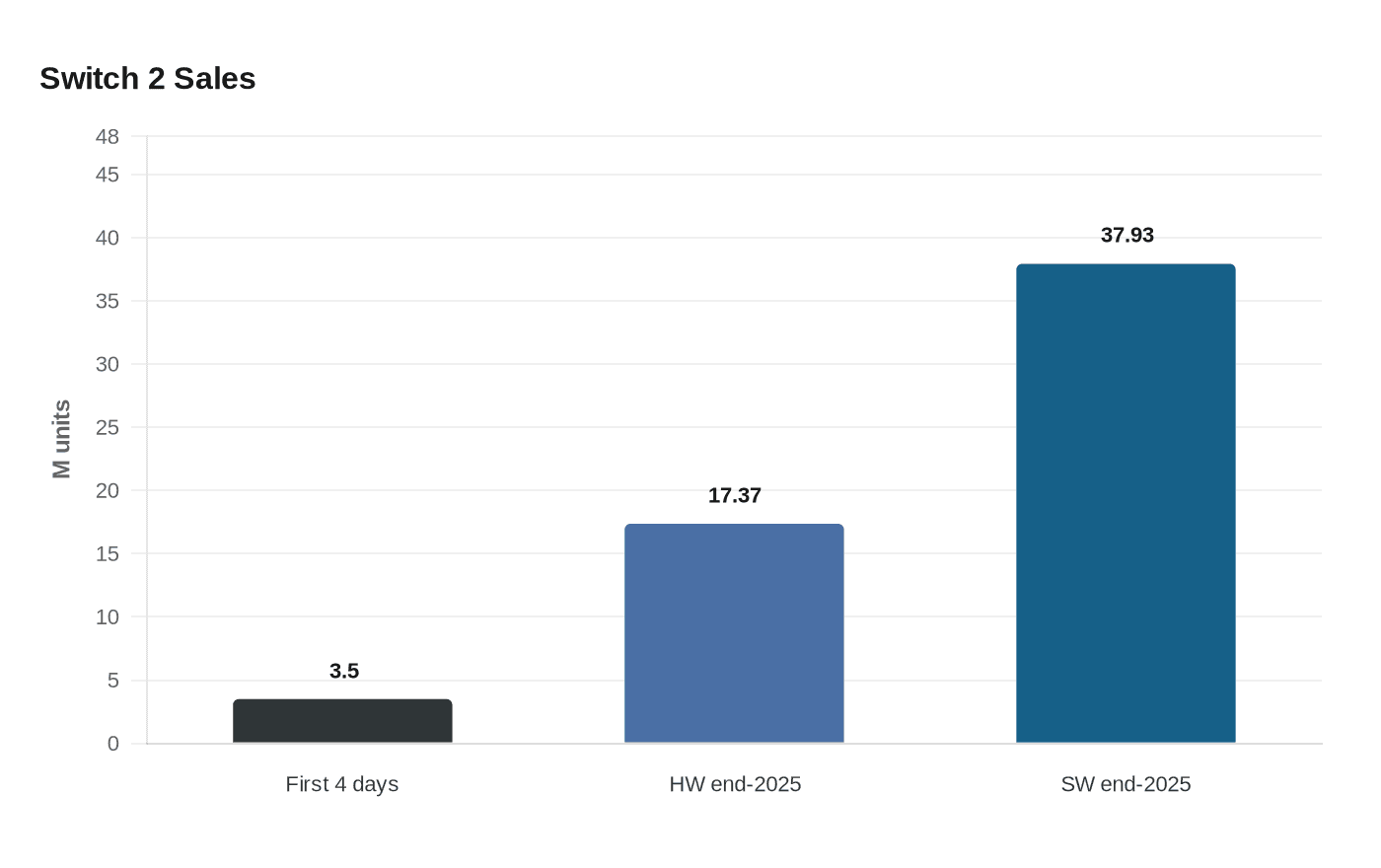

The company’s consumer power is not in question. Nintendo announced Switch 2 on January 16, 2025, with a promise that the successor would arrive that year, and then said on June 11, 2025 that the system had sold more than 3.5 million units worldwide in its first four days. That was the fastest four-day global sales pace ever for Nintendo hardware, a reminder that the brand still has the kind of pull most hardware makers would envy. By the end of 2025, official Nintendo sales data showed Switch 2 hardware at 17.37 million units and software at 37.93 million units, numbers that would normally signal momentum. Yet the market has not treated those figures as a reason for calm.

Why investors are still unconvinced

The Financial Times has highlighted the central contradiction: Nintendo can be adored by consumers and still leave investors uneasy. Its stock page showed Nintendo’s Tokyo-listed shares hitting new 52-week lows in late April and early May 2026, a sharp marker of how wary the market has become. Reuters added to that picture in February 2026, reporting that Nintendo shares fell 10% as investors worried about Switch 2 momentum and the lack of major first-party titles.

That reaction says a lot about how Nintendo is judged. The company is not valued only on today’s sales, but on how long the cycle can run, how expensive the hardware will be to support, and whether the software pipeline can keep the platform from stalling. For a company headquartered in Kyoto, Japan and traded in Tokyo under ticker 7974, those are not abstract questions. They shape how leadership is expected to talk about demand, production, margins, and the depth of the next wave of games.

There is also a familiar anxiety around hardware economics. Investors have been watching rising memory-chip costs and wondering whether pricing pressure could squeeze margins, even when demand is strong. Reuters reported in February 2026 that Nintendo said those memory-chip prices were not having a major impact on earnings in the current financial year, but the company also acknowledged pressure on margins. That combination matters because it shows the balance Nintendo is trying to strike: reassure the market without sounding as if it is dismissing a real cost challenge.

The launch story was strong, but the next phase is harder

Switch 2 gave Nintendo exactly the kind of opening it needed. The launch validated the idea that the company can still command attention at a scale few entertainment brands can match, and the 3.5 million unit first four days gave Shuntaro Furukawa and his team a powerful proof point. But launch surges are not the same as sustained platform health, especially in a market that now wants evidence of long-term engagement, predictable software cadence, and margin discipline.

Nintendo itself has signaled that it sees the forecasts as conservative. In its May 2025 earnings briefing, the company said its Switch 2 hardware and software sales assumptions were conservative estimates and that it was working to strengthen production capacity so it could respond flexibly to demand. That matters because it shows management is not just celebrating demand, it is trying to engineer a supply response that avoids frustrating buyers and leaving revenue on the table. For the teams responsible for manufacturing coordination, global logistics, and launch planning, that is the unglamorous side of success: a blockbuster only looks clean from the outside when the supply chain holds together.

The software question remains just as important. Reuters’ February report on investor concern about a lack of major first-party titles gets to the heart of Nintendo’s model. The company depends heavily on its own franchises and on the software pipeline that turns a hardware launch into a multi-year platform. If that pipeline looks thin, the market assumes the cycle may peak early. For developers and producers inside Nintendo, that translates into enormous pressure to protect franchise legacy while also proving that the next releases can deepen the audience rather than simply feed it once.

What May 8 will test at Nintendo

The next earnings release will not just be about numbers. It will test how clearly Nintendo can explain the distance between consumer enthusiasm and investor doubt. If the company leans only on launch sales, the market may treat the story as already priced in. If it can show that production is scaling, that software momentum is broadening, and that margins are holding up despite memory-chip costs, it has a better chance of changing the conversation.

That is why the timing matters. With shares already under pressure and fresh results due on Friday, May 8, the market will be looking for evidence that Switch 2 is more than a one-cycle phenomenon. Investors will want to know whether hardware demand is still outpacing supply, whether software attach rates are healthy, and whether Nintendo sees enough depth in its pipeline to support the platform without depending on a single wave of excitement.

For Nintendo employees, this is more than a stock-market narrative. It is a reminder that quality-first culture has to survive contact with financial expectations. The company’s reputation is built on polish, franchise stewardship, and careful pacing, but the public market increasingly wants faster proof that those strengths can turn into repeatable growth. That can sharpen pressure on leadership, because every message about conservative forecasts, production capacity, or memory costs is also a message about confidence.

The workplace reality behind the brand

Inside a company like Nintendo, investor skepticism can spill into day-to-day priorities. A hardware launch that sells through quickly raises the stakes for localization, QA, customer support, manufacturing coordination, and the software teams expected to keep the platform fresh. In Kyoto, where the company’s identity is rooted, and across its global offices, the challenge is the same: translate a beloved brand into a business that markets can trust quarter after quarter.

That is the tension around May 8. Nintendo is still one of the clearest examples of a consumer company whose cultural power can outrun financial skepticism. But the stock is telling a different story for now. Until the company proves that Switch 2 can carry demand, margins, and software depth at the same time, Wall Street will keep treating a blockbuster launch as a question, not an answer.

Know something we missed? Have a correction or additional information?

Submit a Tip