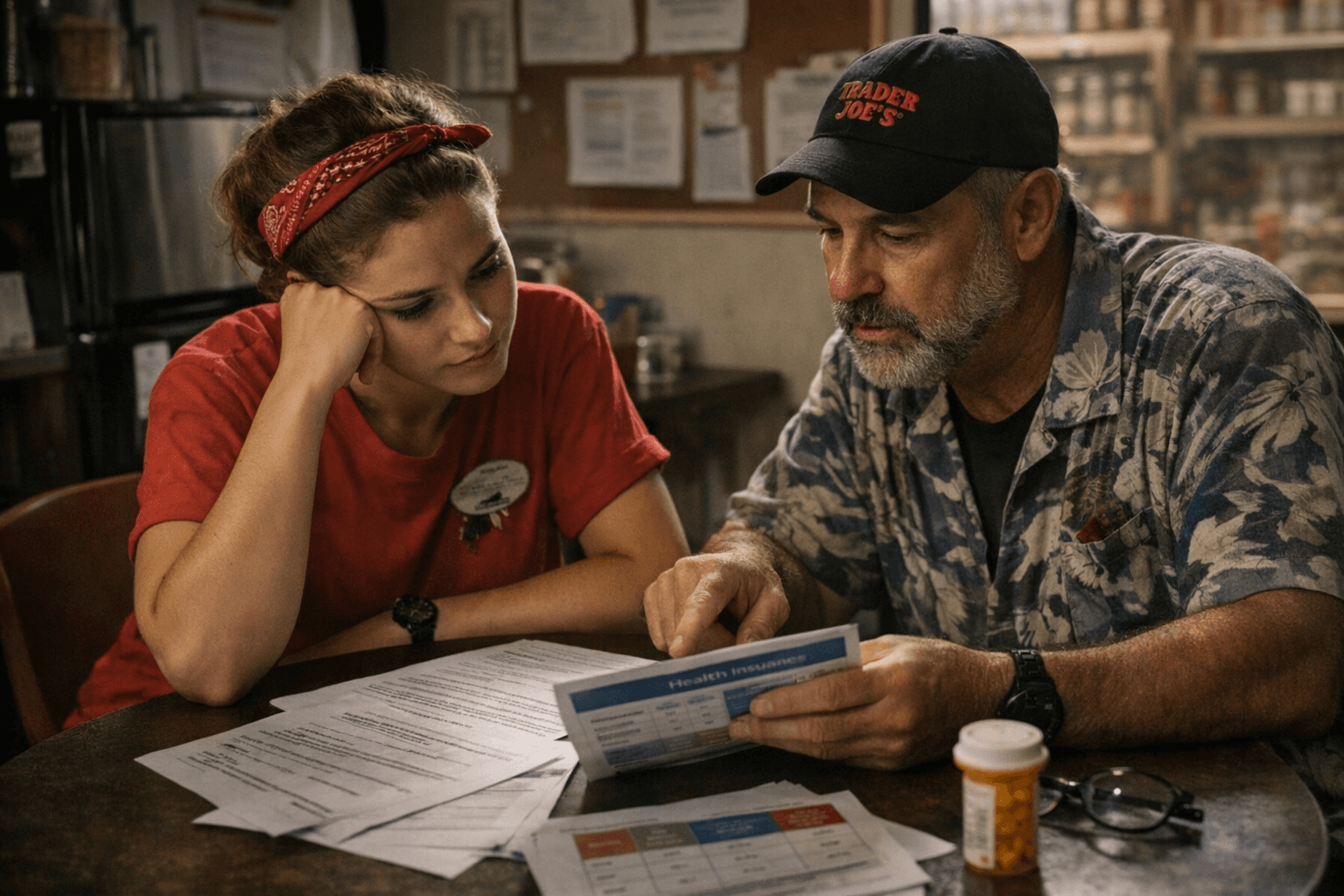

Trader Joe’s employees weigh benefits choices as open enrollment starts

The cheapest premium can be the priciest choice if your prescriptions, specialists, or family needs pile up. Trader Joe’s plan menu can reshape take-home pay all year.

The real money test

The cheapest monthly premium is not always the cheapest health plan. For Trader Joe’s Crew, open enrollment is really a year-long cash-flow decision, because the monthly deduction is only one part of the bill and the rest shows up when you actually need care.

That is why the first comparison should be plain and practical: premium, deductible, copay, coinsurance, out-of-pocket maximum, and network size. Trader Joe’s says eligible Crew Members can get medical, dental and vision coverage, with Crew Member contributions as low as $25 a month, so the stakes are real for hourly workers who have to balance take-home pay against the cost of doctor visits, prescriptions, and specialist care.

A lower premium can look attractive on payday and still cost more over the year if the deductible is high or the network is narrow. A higher premium can be the smarter choice if you already know you will use care often. The right answer is not the plan that sounds best in the abstract. It is the one that matches the care you expect to use in the next 12 months.

When a low-premium plan makes sense

For a single worker who rarely sees a doctor, a lower-premium plan can be the right fit, especially if you do not take routine prescriptions and do not expect specialist visits. In that case, paying less every paycheck may matter more than paying for richer coverage you are unlikely to use.

Still, low utilization does not mean no planning. Check whether your preferred clinic is in network, whether telehealth is available, and how the plan handles urgent care visits. If you spend long shifts on your feet, even a small injury or an unexpected appointment can quickly turn a “cheap” plan into a more expensive one if the provider is outside the network or the deductible is steep.

When to pay more for broader coverage

If you expect frequent doctor visits, ongoing prescriptions, physical therapy, or specialist care, a higher-premium plan can save money in the long run. The reason is simple: you may pay more each month, but you can cut down the amount you owe when care actually happens.

That logic matters even more if your family situation is changing. A spouse’s job, a new baby, a dependent entering college, or a shift from full-time to part-time hours can all change what good coverage looks like. Benefits should fit the year you are about to live, not the one you had last year.

Prescription users should start with the formulary

If you take maintenance medications, the prescription formulary should be one of your first stops. Confirm that your medications are covered, check whether they sit in a preferred tier, and see whether the plan has any prior authorization or refill limits that could affect you later.

That same check applies to people who use a specific clinic or specialist. A plan with a comfortable monthly price can become a headache if your regular doctor is out of network. The provider directory is boring to read, but it is the fastest way to avoid an expensive surprise.

Don’t skip dental and vision

Dental and vision coverage are often treated like extras, but for grocery work they can be unusually relevant. Long shifts, constant movement, and time on your feet can make eye care and dental work more than a nice-to-have. A routine eye exam, new glasses, or a dental filling can affect comfort and day-to-day functioning more than people expect.

That is especially true if you are trying to keep your monthly budget predictable. Vision and dental bills can arrive all at once, while the premium stays flat. If you know you will need both kinds of care this year, buying coverage for them can be one of the cleaner financial decisions in the benefits package.

HSA or FSA? Know what each one is for

If your enrollment options include a health savings account or a flexible spending account, treat that choice as seriously as the medical plan itself. HSAs can come with tax advantages and may roll over from year to year, which makes them useful if you want to save for future medical costs and keep the money available beyond one calendar year.

FSAs are often better for predictable expenses you know you will have this year, but they can come with stricter rules and may not let you carry money forward the same way an HSA can. The exact tax rules, contribution limits, and whether an HSA is paired with a high-deductible health plan still need to be checked in the enrollment packet, because those details can change the math fast.

- Choose an HSA if you want long-term flexibility and expect to build savings for future care.

A simple rule of thumb helps:

- Choose an FSA if you have steady annual expenses and can estimate them pretty well.

- Avoid guessing on either account, because the wrong contribution amount can leave money stranded or short.

Think beyond health coverage

Open enrollment is not only about medical insurance. Trader Joe’s says it also offers a 401(k) retirement plan, paid time off that increases with tenure, and an employee assistance program. Those pieces matter because total compensation is bigger than the premium on a benefits page.

The company also says all Crew Members currently receive up to a 20% discount on all products in its stores. For workers who shop where they work, that discount can be part of the monthly household budget, not just a perk. When you stack that alongside health coverage, PTO, retirement saving, and an employee assistance program, the full package is what supports stability, not one line item by itself.

What the Trader Joe’s culture says about the stakes

Trader Joe’s presents itself as a place where internal growth matters, and its numbers back that up: 78% of Mates started as Crew, and 100% of Captains were promoted from the Mate role. That makes benefits decisions part of a longer work life, not just a single enrollment season.

A Crew member who makes a smart choice now is not only managing this month’s paycheck. They are choosing how much financial stress they carry into the year ahead, and whether coverage, savings, and paid time off work together or fight each other. At Trader Joe’s, that is not a side issue. It is one of the clearest ways the company’s promise shows up in a worker’s actual life.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?