Luxury Giants Pivot to Margin Protection Amid Uneven Global Recovery

LVMH's revenue fell to €80.8B in 2025 as all three luxury giants shift capital from runway spectacle to watches, jewelry, and tighter store networks.

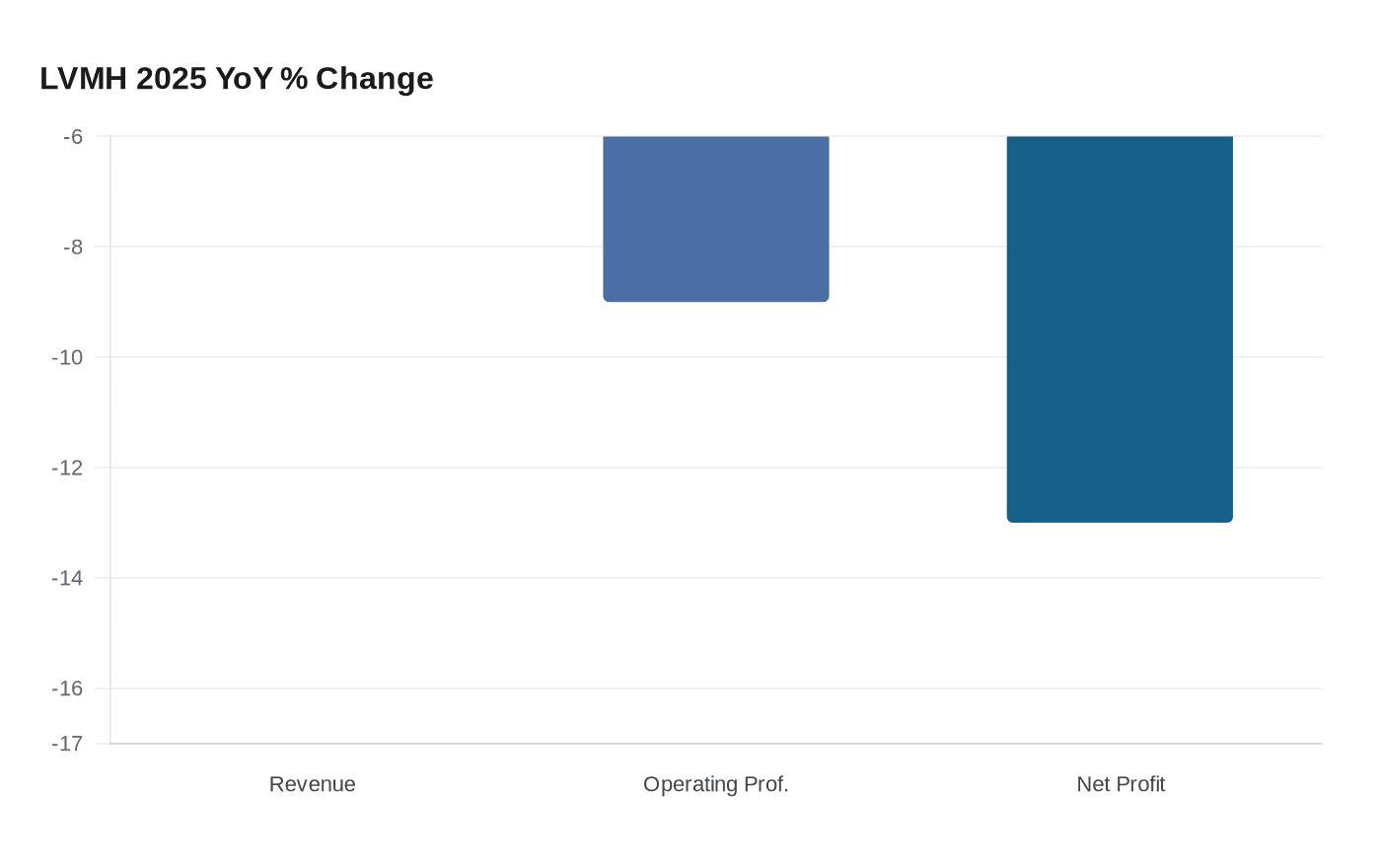

When LVMH reported full-year 2025 revenue of €80.8 billion, down 5 percent from the prior year, it confirmed what investors had already suspected: the post-pandemic luxury supercycle is over, and the conglomerates that built empires on it are now engineering a careful retreat. Profit from recurring operations fell 9 percent to €17.8 billion at LVMH, while net profit attributable to the group declined 13 percent to €10.9 billion. Kering's situation was starker still. Group net profit plummeted 46 percent in the first half of 2025, underscoring the pressure bearing down on incoming CEO Luca de Meo, who took the reins on September 15, succeeding François-Henri Pinault, who had held the title since 2005.

The response from all three major groups has been the same: pull back the network, protect the margin, and stop chasing top-line growth at the expense of profitability. Kering has already moved forward with a plan to close 100 stores in 2026, and the cuts have not been evenly distributed. Of the net store closures in 2025, nearly 40 percent were Gucci locations, with Alexander McQueen also caught in the contraction. For a shopper who has watched Gucci's footprint sprawl through every airport retail corridor over the past decade, the retrenchment signals something significant: the era of omnipresent luxury is giving way to something more deliberate.

Richemont, meanwhile, demonstrated exactly where the safe harbor lies. Its Jewellery Maisons, Cartier, Van Cleef & Arpels, Buccellati, and Vhernier, posted a 9 percent increase in sales in the first half of the fiscal year ended September 2025, rising to €7.7 billion, with Q2 growth hitting 17 percent at constant exchange rates. The operating margin for the Jewellery Maisons stood at 32.8 percent, a figure that makes the conglomerate's strategic logic self-evident. Richemont also completed the sale of YNAP to Mytheresa and added Italian jeweller Vhernier to its stable, moves that sharpened rather than broadened its focus.

At LVMH, the same category hierarchy is asserting itself. The Watches and Jewelry division outperformed expectations with revenue of €10.5 billion, exceeding forecasts by 1.4 percent, while Fashion and Leather Goods, the group's largest division at €37.8 billion, declined year-over-year. The divergence is a blueprint: icon jewelry and fine watchmaking are holding value; experimental ready-to-wear and the smaller ateliers dependent on runway spectacle for visibility are getting squeezed.

For anyone building a wardrobe with an eye on longevity, these corporate decisions translate directly into what to buy and what to hold off on. Core leather goods from heritage houses, Vuitton's monogram canvas, Cartier's Love bracelet, Van Cleef's Alhambra, sit above the restructuring fray because they generate the margins that justify protecting them. The same capital allocation logic that keeps those lines fully staffed in the atelier also keeps their price architecture stable and their clienteling programs funded. What faces greater risk is the category that luxury groups expanded into most aggressively during the growth years: experimental RTW from houses without deep couture roots, limited-edition collaborations engineered for social media velocity, and the second-tier labels within each conglomerate's portfolio that lack the heritage to command the prices necessary to survive a margin-protection cycle.

The fragrance and wellness push, framed by the conglomerates as a lower-barrier entry point into a brand's world, is worth watching as a quality signal. When a house accelerates its fragrance rollout, it is often funding its atelier budget by monetizing brand equity at a lower price point. Under scrutiny from top managers and investors, LVMH, Kering, and Richemont are re-examining their brand portfolios, organizational structures, and store networks, having dialed back on the expansionist strategies that propelled past growth. A house whose leather goods quality begins to slip while its fragrance line expands is almost certainly cross-subsidizing; conversely, a house that holds its leather goods price architecture firm and limits fragrance to genuinely complementary categories is more likely protecting its craftsmanship rather than funding it. In 2026, the clienteling shift will be the clearest signal of all: the houses that invest in dedicated advisors and appointment-based service are protecting their top tier, while those that push clients toward digital self-service are trimming the operational cost of the relationship. Watch which side of that line your preferred house lands on.

Know something we missed? Have a correction or additional information?

Submit a Tip