Textile recycling gets a second wind as policy and new pilots revive industry interest

Renewcell's 2024 bankruptcy nearly derailed chemical textile recycling, but a Circulose plant restart, Syre's $600M H&M deal, and mandatory EU EPR schemes are rewriting the sector's prospects.

Renewcell's collapse in 2024 was supposed to be the cautionary endpoint for a decade of chemical textile recycling ambition. The Swedish firm had been the Nordic movement's most visible standard-bearer, its cellulosic fiber technology celebrated and its brand partnerships enviable. Then it went bankrupt anyway. For procurement teams who had quietly begun building circularity into supplier contracts, and for investors who had written early cheques, it felt like confirmation of a thesis: the chemistry works, the economics don't.

Two years on, that verdict looks premature. A convergence of policy mandates, restructured capital strategies, and a fresh cohort of demonstration plants is pushing the sector into what researchers are calling its second wind. This time, the companies advancing are doing so differently, treating market-building as inseparable from process engineering.

What broke the first wave

The lesson of the first cycle is not that chemical recycling failed; it is that commercial strategy lagged the science. Renewcell's own story is instructive. Reborn under private equity firm Altor as Circulose, the company has announced plans to restart commercial-scale production at its Sundsvall, Sweden plant toward the end of 2026. CEO Jonatan Janmark is candid about what went wrong the first time: "They went from 0 to 100 in a short amount of time in terms of supply and hadn't really prepared a market for that." The technology itself, a process that chemically recycles waste cotton into cellulosic fiber, was not the problem. The reborn company has merely refined how it mechanically shreds waste fibers to improve the quality of the pulp the fibers are converted to.

Ali Harlin, a research professor at VTT Technical Research Centre of Finland, frames the damage in time rather than technology. Chemical textile recycling lost "2 or 3 years of progress, easily" to changes in the financing environment. His warning for the next phase is blunter still: the sector could replicate plastics recycling's dead ends if firms open commercial plants without guarantees that the textile industry will buy enough of their products. "The road to textile recycling is there," Harlin says, "but first we need to get the whole value chain streamlined."

Olli Kähkönen, CEO and co-founder of Nordic Bioproducts Group, identifies the underlying cause as industry-wide indifference. There remains a lack of interest in chemical recycling across the textile value chain. "That's a global problem," he says.

The pilot landscape in 2026

The structural shift that distinguishes this wave from the last one is the presence of pre-committed offtake. Syre, co-founded by H&M Group, Vargas Holding, and private equity firm TPG Rise Climate, is the most conspicuous example. H&M Group has made a $600 million offtake agreement to purchase recycled polyester from Syre, with the company's first plant in North Carolina built on an initial combined investment of roughly $60 million. Syre's long-range ambition is annual production of over 3 million metric tons of recycled polyester from 12 plants by 2034. The model is a direct answer to Harlin's critique: volume commitments come before shovels go in the ground.

Alongside Syre, two other names are reaching commercial thresholds this year. Evrnu's first commercial manufacturing facility, which takes cotton-rich waste from the manufacturing process and discarded consumer fashion items to make lyocell fiber, is due to be completed in 2026 and will produce 18,000 metric tonnes of fiber annually once operational. Infinited Fiber Company is building its first commercial plant with 30,000 metric tonnes of annual capacity, enough fiber for around 100 million T-shirts, transforming cellulose-rich textile waste into a cotton-like fiber. The Finnish company raised $44 million to underwrite the buildout. Brand partnerships, including multi-year offtake deals struck by Ganni with Ambercycle for recycled polyester, are increasingly the mechanism for de-risking these plants before they produce a single kilogram.

Textile-to-textile vs. downcycling: the distinction that matters

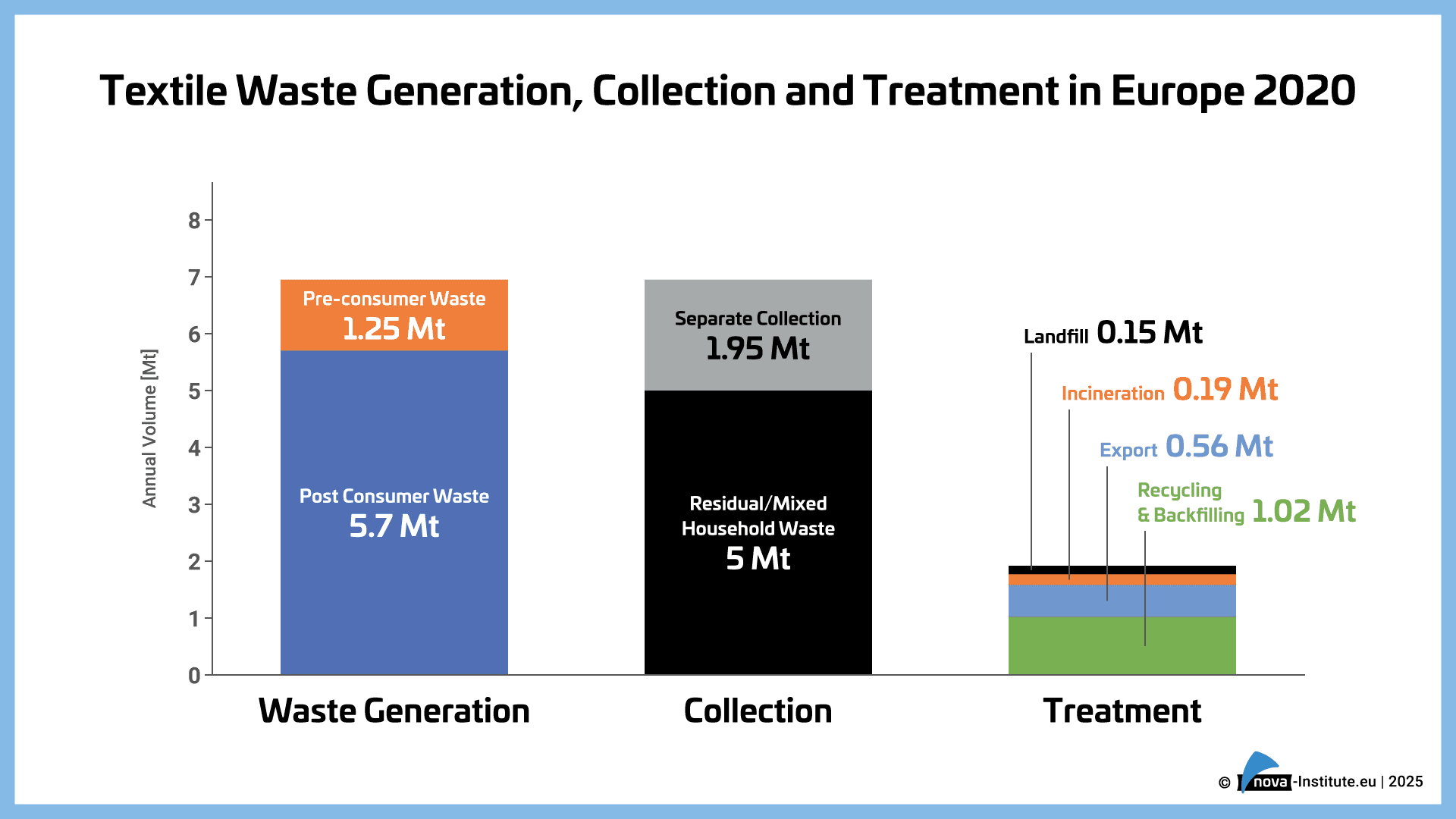

For procurement teams evaluating supplier claims, the vocabulary matters enormously. Genuine textile-to-textile recycling, what Syre and Circulose are doing, returns fiber to apparel-quality feedstock: a recycled polyester or cellulosic fiber that can re-enter the same supply chain that generated the waste. Downcycling, the more common fate of collected garments, sends textiles to insulation, industrial rags, or carpet backing. It absorbs material from the loop without returning it, and it cannot fulfill the circularity commitments increasingly embedded in EU procurement regulations.

The distinction is technical as well as definitional. Polyester accounted for 44.30% of the textile recycling market in 2025, partly because its polymer chemistry is more amenable to true fiber-to-fiber recovery than cotton-synthetic blends. Cotton-dominant and cellulosic waste streams require the more capital-intensive dissolution and regeneration processes that firms like Circulose and Infinited Fiber are scaling. Brands sourcing "recycled content" should verify whether the fiber was recovered at textile grade or simply diverted from landfill into a lower-value application; the difference is commercially and regulatorily significant as EPR fee structures come into force.

The three bottlenecks that still limit scale

Even with capital commitments and regulatory tailwinds, three structural problems constrain how quickly the sector can grow.

Sorting. Consumer-collected textiles arrive at sorting facilities as a heterogeneous, often contaminated stream: mixed fibers, unknown dye lots, zips, buttons, embellishments. Near-infrared scanners, the current standard for automated sorting, reach only 85% accuracy on elastane-rich blends, driving quality downgrades and material loss. AI-enabled systems are showing promise in pilots, with some achieving 80-plus percent classification accuracy, but these are not yet at industrial throughput. Until sorting reliability improves, chemical recyclers are forced to rely on the cleaner, more predictable pre-consumer waste streams (manufacturing offcuts), which limits the volume available and reduces the environmental impact of the process.

Contamination. Even well-sorted feedstock presents chemistry problems. Blended fabrics — the polyester-cotton mixes that dominate fast-fashion production — require separation steps before either polymer can be recovered at quality. Pilot lines in France currently process 25,000 tonnes annually but must divert contaminated fractions to lower-value uses. Novel chemical-separation approaches are in development, but they add process steps and cost, sustaining a price premium for clean, single-fiber feedstock that most consumer wardrobes do not generate.

Economics. The financing fragility exposed by Renewcell has not been fully resolved. Eastman's now-revoked Department of Energy grant highlights the sector's reliance on public policy support. When that support is withdrawn or delayed, as it was during the financing environment shift Harlin describes, timelines slip and capital dries up. The sector's current model, in which brand offtake commitments substitute for policy certainty, is more resilient than the grant-dependent approach, but it still concentrates risk in a small number of anchor partnerships. A brand that renegotiates or cancels an offtake agreement does not merely lose a customer; it can destabilize the commercial case for an entire plant.

The policy architecture that changes the calculus

The structural shift that distinguishes 2026 from 2022 is not primarily technological; it is regulatory. The revised EU Waste Framework Directive, which entered into force in October 2025, mandates that all Member States establish Extended Producer Responsibility schemes for textiles and footwear. Under these schemes, producers will pay a fee for each product they place on the market, with Member States given 30 months to establish their national programs. France is expected to enact its national scheme in 2026; the EU's broader transposition deadline runs through mid-2027.

Across the Atlantic, California has moved first among US states. CalRecycle has appointed European recycling specialist Landbell USA to lead the nation's first textile EPR program, creating a precedent that other states are likely to follow. The significance for recyclers is not merely that fees will flow toward collection and sorting infrastructure; it is that brands now face a direct financial disincentive for placing unrecyclable products on the market. Design-for-recyclability, which requires standardizing fiber compositions to match accepted feedstock specs, becomes a cost-reduction strategy rather than an aspiration.

The brands most exposed are those whose collections rely on complex blends and heavy embellishment. Those best positioned are the ones already locking in multi-year supply agreements with firms like Syre, Circulose, and Infinited Fiber, because those relationships are simultaneously building the market demand that recyclers need to justify industrial-scale investment.

The lesson of the first wave was that chemistry without commerce collapses. The lesson the sector is acting on now is that commerce without policy remains fragile. For the first time, all three elements are moving in the same direction at once.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?