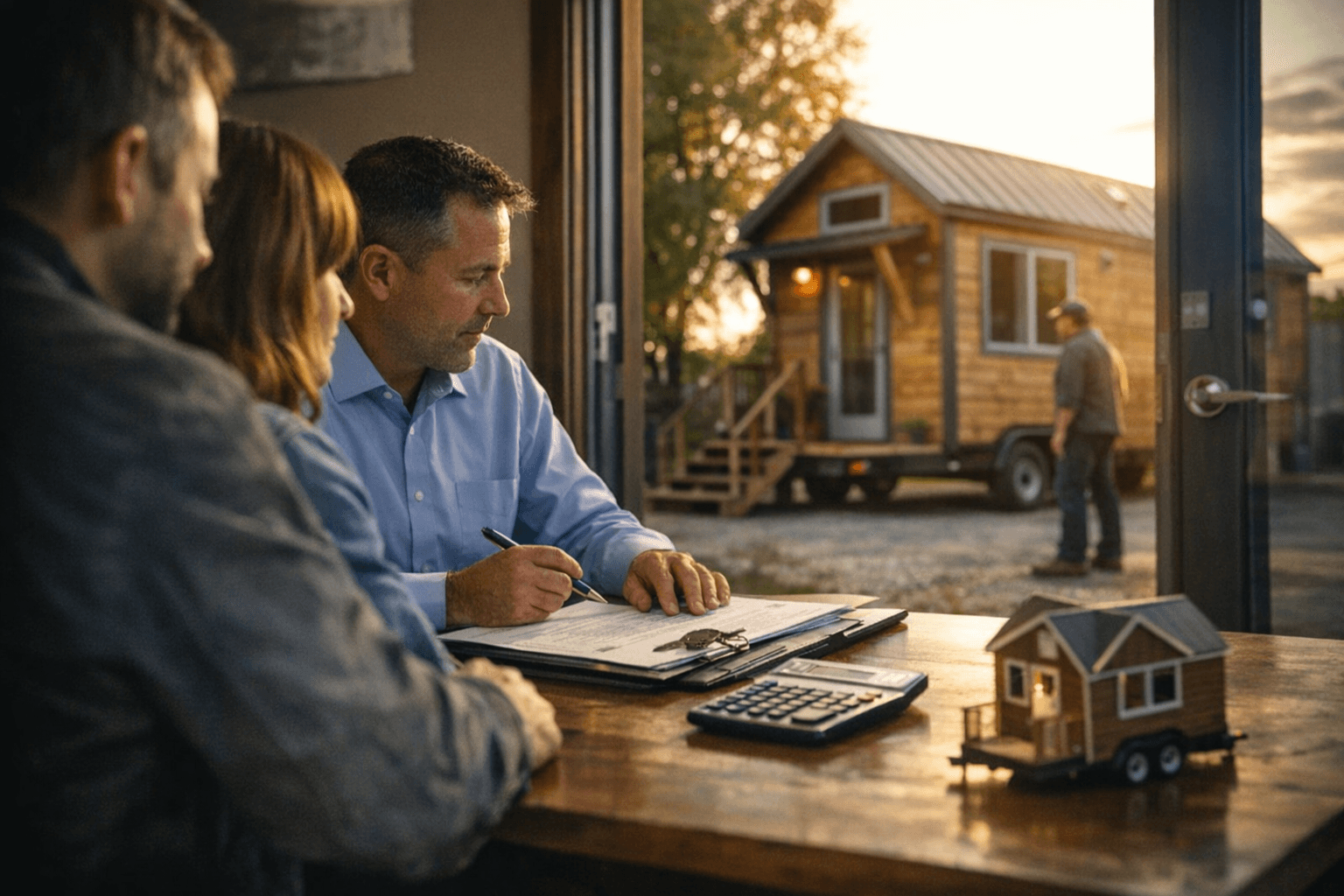

Tiny House Financing Options, Obstacles, and Best Practices Explained

Getting a tiny house financed in 2026 is entirely doable, but only if you match the right loan type to how your home is classified before you walk into a lender's office.

The Classification Question Lenders Ask First

Before any lender quotes you a rate, they need to know one thing: what exactly is your tiny house? That single question drives everything from the interest rate you'll receive to whether you qualify for financing at all. A tiny house on wheels (THOW) that carries RVIA or ANSI A119.5 certification is legally a recreational vehicle in most jurisdictions, which opens one set of financing doors. A foundation-based tiny house built to IRC Appendix Q or HUD manufactured-home standards opens an entirely different set. Mixing up those categories, or arriving at a lender without documentation that answers the question cleanly, is the single most common reason tiny-house loan applications stall or fail.

The Four Main Financing Pathways

Cash or personal savings is the simplest route if it's available, and it sidesteps every classification headache. But for the majority of buyers, it's unrealistic given that turnkey tiny houses regularly reach $80,000 or more once site infrastructure is included.

Personal loans and home-equity products are the most broadly accessible option. Unsecured personal loans require no collateral and can fund quickly, but they carry a real cost: the average personal loan rate stood at 12.04% as of April 2026, and most products cap out at a seven-year term. On an $80,000 purchase, a seven-year loan at 12% produces a monthly payment roughly double what a longer-term secured loan would require. Home-equity loans and HELOCs use existing real estate as collateral, which typically brings rates down considerably, but they require 15 to 20% equity in a property you already own, and they put that property at risk.

Specialized tiny-home and RV lenders serve the THOW market specifically. For a towable unit carrying RVIA certification, RV loans are often the most favorable path: current secured RV loan rates range from under 7% to around 12% for well-qualified borrowers, and terms can stretch to 15 or 20 years, making monthly payments far more manageable than a personal loan on the same balance. The trade-off is qualification: most RV lenders want a credit score of 680 or better, a debt-to-income ratio under 45%, and a down payment of 10 to 20%. Not all tiny house builders are RVIA-certified, so confirming certification before you shop is essential, not an afterthought.

Construction and manufactured-home loans apply to foundation-based units. For this pathway to work, the home generally needs to be built to a recognized standard, either IRC Appendix Q (the dedicated code appendix for houses under 400 square feet) or HUD manufactured-home standards, and it must be sited on real property with a legal right of use. HUD guidelines require a permanent foundation and at least 400 square feet for traditional mortgage eligibility; Fannie Mae sets its manufactured-home floor at 600 square feet. That threshold eliminates many tiny houses from conventional financing, which is why finding lenders who specifically work with sub-600-square-foot structures matters so much. Community banks and credit unions are often more flexible here than national lenders.

The Three Obstacles That Kill Applications

Zoning and code classification ambiguity is obstacle number one. Lenders and insurers alike need a definitive answer on whether your home is an RV, a manufactured dwelling, or a site-built structure, and "it depends on the county" is not an acceptable answer in an underwriting file. Getting a formal written determination from your local jurisdiction before you apply converts vague intent into bankable documentation.

Appraisal and collateral uncertainty is the second major barrier. Tiny houses have a relatively thin resale market compared to conventional housing, which makes it harder for lenders to establish reliable collateral values. Shorter loan amortizations are one response to that risk: lenders sometimes compress terms to limit their exposure, which pushes monthly payments higher and reduces borrower qualification rates. Addressing this proactively means supplying a detailed cost breakdown, a fixed-price contractor estimate, and comparable sale data if any exists in the local market.

Utilities and site readiness round out the trio. A lender financing a residential structure wants assurance that the property has confirmed utility hookups, an approved septic or sewer connection, and a legal pad or foundation. Infrastructure costs are among the most commonly underestimated line items in any tiny-house budget, and showing a lender that those costs are already scoped and funded signals that the project is real, not aspirational.

Best-Practice Checklist Before You Apply

Working through these steps in sequence dramatically improves the odds of approval:

1. Determine your home's legal classification (THOW versus foundation-based) and identify the applicable code: RVIA/ANSI A119.5, IRC Appendix Q, or HUD manufactured-home standards.

2. Secure a written zoning or permit letter from the local jurisdiction. A recorded assurance that the site is approved for the intended use is worth more to an underwriter than any verbal confirmation.

3. Get a fixed-price contractor scope covering all construction and site work. Lenders want line items, not ballpark estimates.

4. Collect proof of stable income and a clear occupancy plan, whether that is a long-term residency commitment or a documented exit strategy such as a future sale.

5. Compare rates across loan categories: specialized tiny-home lenders, credit unions, and personal loan providers. The gap between a well-sourced RV loan and an unsecured personal loan can easily exceed five percentage points.

6. Investigate insurance early, because coverage rules differ sharply between RV-classified and dwelling-classified structures. Discovering at closing that your lender requires dwelling insurance for a unit your insurer treats as an RV is a deal-stopper.

7. Budget explicitly for infrastructure: utility hookups, septic or sewer connections, foundation or pad work, and any required land improvements. These costs often dwarf the line items buyers plan for, and lenders scrutinize them closely.

Putting It Together

Tiny-house financing in 2026 is not standardized the way a 30-year fixed mortgage is, but it is increasingly viable for buyers who do the classification and documentation work upfront. The buyers who get approved are, almost without exception, the ones who show lenders clarity: a permit letter in hand, a contractor quote with a firm number attached, and a financing pathway logically matched to how their home is legally defined. For anyone still navigating the jurisdictional patchwork, connecting with a mortgage broker who has actually closed tiny-house deals in the target area, or with a local builder familiar with what lenders in that market require, remains the fastest way to avoid expensive detours.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?