Francisco Blaha Critiques FFA Report on Western and Central Pacific Tuna Trade

Francisco Blaha published a critical analysis of an FFA report on Western and Central Pacific tuna trade, raising concerns about market players and policy gaps that affect Pacific producers.

Industry commentator Francisco Blaha published an analysis on 6 February 2026 reacting to a Forum Fisheries Agency report on tuna markets, and his critique has already stirred discussion in Pacific fishing circles about who benefits from trade and how policy shapes the business. Blaha’s post highlights the report’s review of major global players, though the supplied excerpt of his commentary is truncated and the full passage needs to be read for his detailed claims.

The wider context shows these are not new questions for Pacific island countries. The FFA’s 2007 guidebook Pacific island countries, the global tuna industry and the international trade regime: a guidebook by L. Campling, E. Havice and V. Ram-Bidesi set out trade-related elements for the Western Central Pacific Ocean fishery and urged political leadership to respond. The guidebook put it plainly: “ministers and senior officials need to take collective responsibility for their country’s tuna trade because they have a responsibility to protect and promote domestic trade interests.” That line underlines longstanding calls for coordinated policy on tariffs, subsidies, standards and market access.

Policy discussions at PTF 2025 carried those themes forward. As the forum summary put it, “Over six lively sessions, the forum tackled everything from how to keep Pacific tuna stocks healthy to how island nations can get a fairer deal from the global fisheries trade.” FAO GLOBEFISH contributed to sessions on sustainability, market access and supply chains, including a session titled “Sustainable Tuna Resources and Supply Chains in the WCPO” that focused on stock assessments, traceability and Port State Measures, and a session titled “Global and Regional Tuna Trade and Market Access” that shared insights on U.S. market access and tariff impacts on Pacific trade.

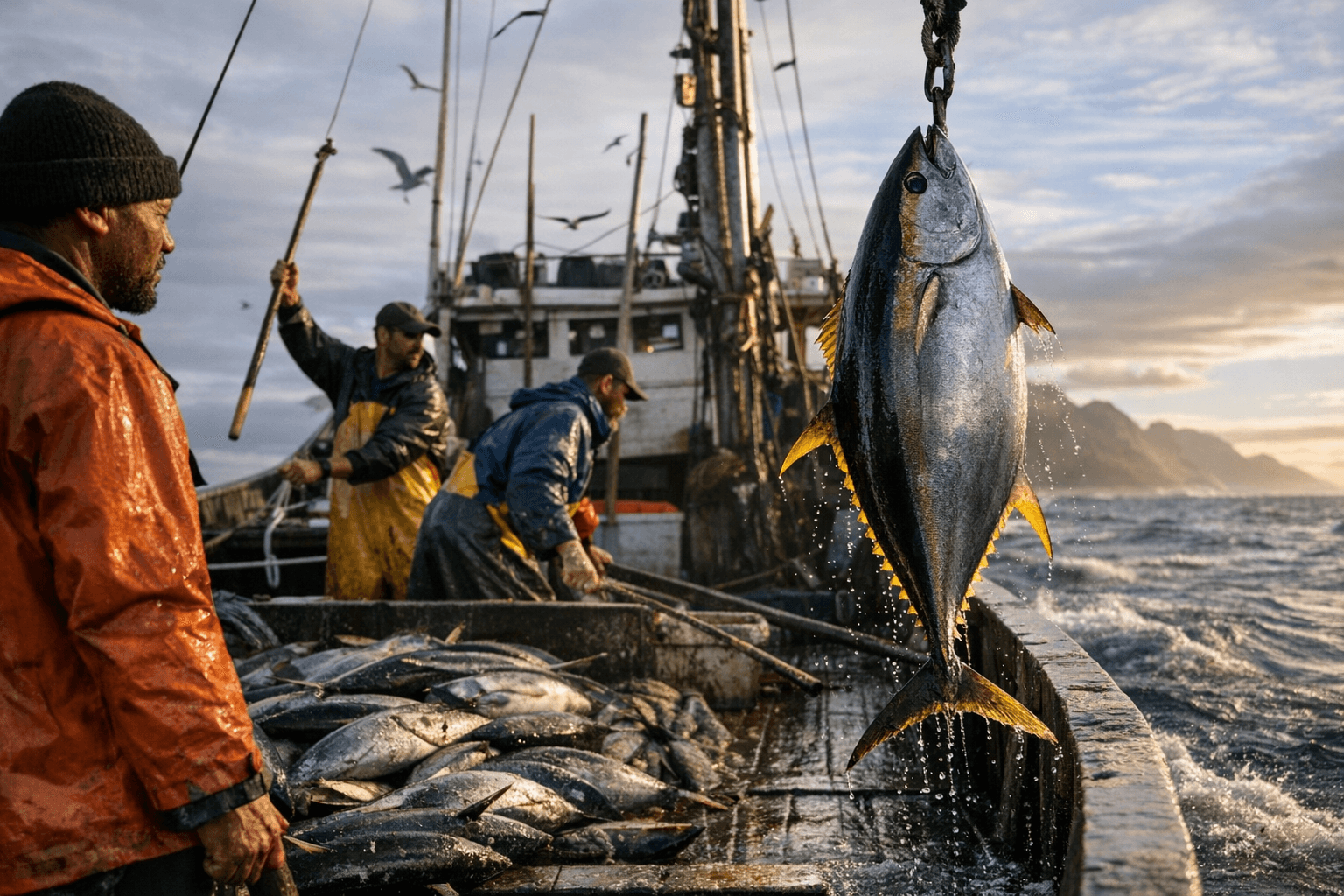

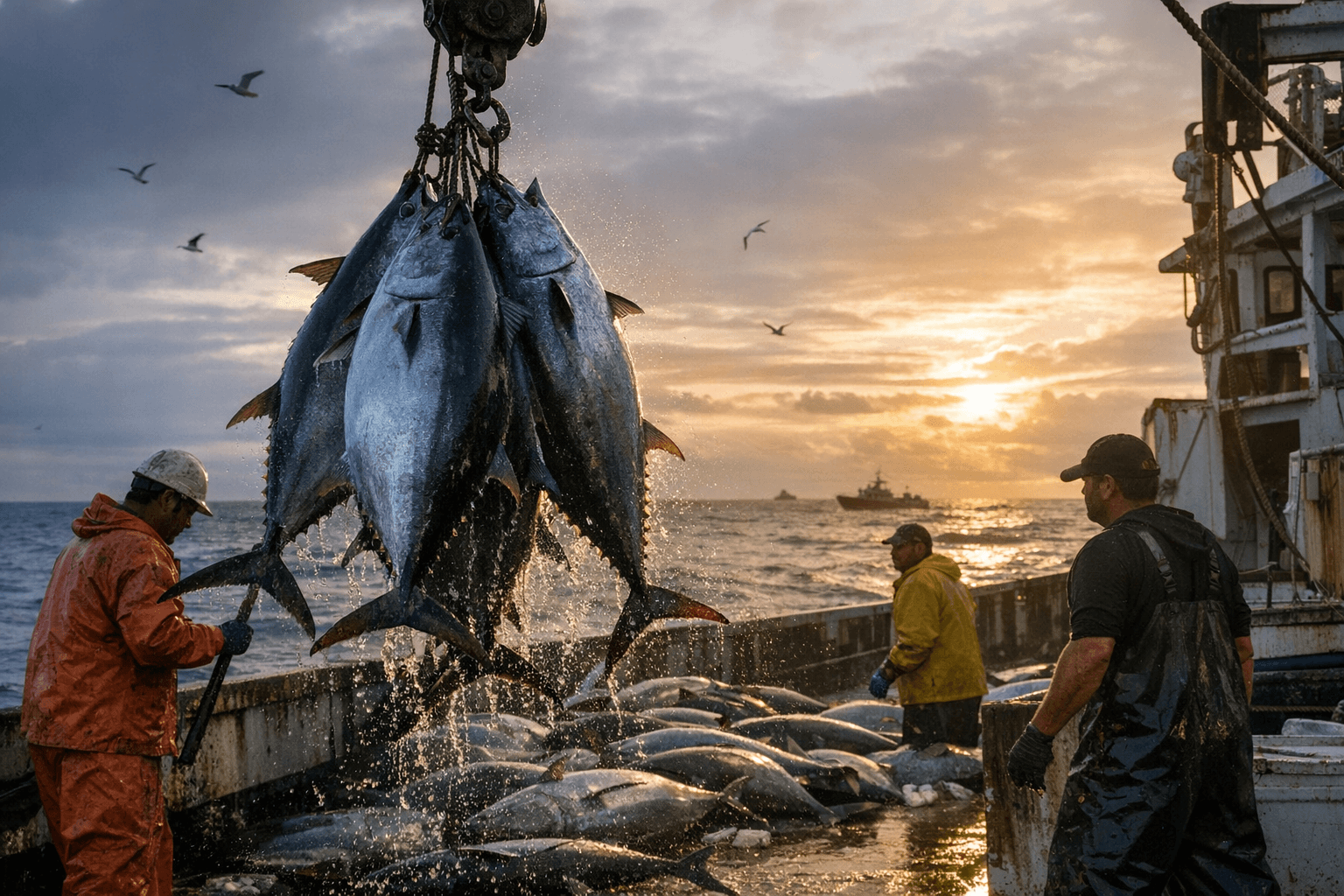

Market forces add pressure on policy. Polarismarketresearch values the global tuna market at USD 45.51 billion in 2024 and projects growth to USD 64.57 billion by 2034, with a CAGR of 3.6% from 2025 to 2034. Industry drivers it lists include rising health awareness, diet trends like keto and paleo, and demand for convenient protein-packed products; it also warns that “Overfishing, bycatch issues, and unsustainable practices threaten tuna populations, raising regulatory scrutiny and limiting long-term supply availability.” Skipjack remains dominant for canned products, and canned tuna still leads global trade.

The historical market structure matters for smaller producers. Scholarship on the Pacific islands notes that in 1985 the region accounted for about 40 percent of global tuna supplies, most harvested by purse seiners and processed into canned products that make up two-thirds of international tuna trade. The United States has long been a major buyer and price reference for cannery-quality fish.

For fishers, processors and island governments, the practical stakes are clear. Market growth and consumer trends create opportunity, but traceability rules, tariffs, and sustainability measures determine who captures value. Blaha’s critique has refocused attention on the balance between global buyers and Pacific producers and on whether current trade arrangements protect local jobs and revenue. Watch for the full FFA report and Blaha’s complete analysis to land; in the meantime verify the figures and policy proposals you rely on, and expect continued debate on tariffs, traceability and fair returns for fish caught in WCPO waters.

Know something we missed? Have a correction or additional information?

Submit a Tip