Pearl prices surge as China and livestreaming drive demand

Pearl prices are climbing as China’s buying power and livestream selling collide with tighter supply, pushing freshwater and Akoya categories higher.

Pearl pricing is feeling pressure from both ends of the market: production has tightened, while demand in China has stayed remarkably strong, amplified by livestream selling and a younger buyer who sees pearls less as heirloom formality and more as modern, wearable luxury. The result is a category-wide squeeze that is lifting prices across freshwater, Akoya and Tahitian pearls, with the sharpest gains visible where supply is most constrained.

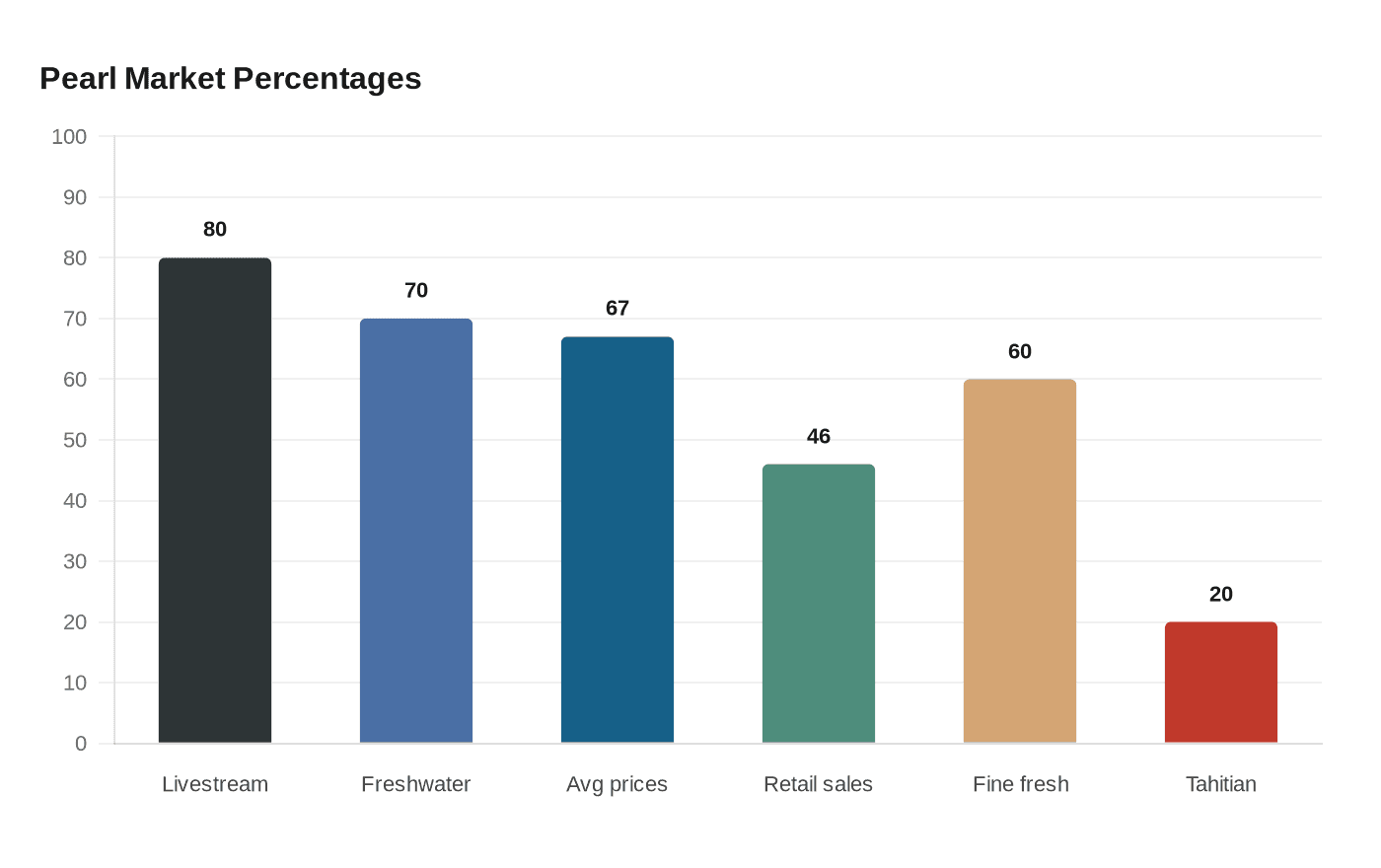

China’s pearl sector cooled in the first half of 2024 after the boom of 2023, but it recovered through the first half of 2025. Zhuji, in Zhejiang Province, remains the center of gravity. The city produced 600 tonnes of freshwater pearls in 2024, or about 70% of global freshwater output, and its pearl sector generated annual sales above RMB50 billion, about US$6.98 billion. Pearl jewelry retail sales in China rose about 46% in 2023 to RMB35 billion, about US$4.85 billion, underscoring how quickly the domestic market expanded before moderating and then rebounding.

Livestreaming has become one of the industry’s most important sales engines. At Y&M Pearls, Ye XiaoBo said 80% of overall sales in 2024 came from livestreaming, a figure that shows how decisively the category has moved online. On social platforms such as Xiaohongshu, pearls are being recast as quiet-luxury staples rather than old-fashioned dress jewelry, helping fuel demand among younger consumers in China and beyond.

The tightening is visible in pricing. The American Gem Trade Association has said Japanese Akoya production has fallen more than 80% over 30 years, and that Japanese harvested pearls in early 2023 were down nearly 10% year over year even as average prices rose 67%. U.S. buyers were seeing Akoya prices 40% to 50% higher than the previous year. Fine freshwater pearl prices were up as much as 60%, while Tahitian pearls rose at least 20%.

That leaves a more nuanced value picture for buyers. Chinese freshwater pearls still offer one of the clearest entry points, especially because they can be more affordable than Akoya while delivering strong whiteness, luster and color range. Jeremy Shepherd of the Cultured Pearl Association of America has said U.S. consumers prefer non-beaded pearls, which are largely produced in China, and that Chinese freshwater pearls are winning on sales volume. The sector’s roots run back to 1962, when professor Xiong Daren began the first freshwater pearl cultivation experiments in China, a reminder that today’s surge sits atop more than six decades of industrial buildout. For the next 6 to 12 months, the categories most likely to stay tight are top-grade Akoya and fine-luster freshwater strands, while well-matched Chinese freshwater pearls should remain the best relative value in a rising market.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?