Pearls Gain Appeal as Alternative to Gold Amid Rising Metal Prices

Gold's 66% surge in 2025 is pushing buyers toward pearls, where freshwater prices remain broadly stable and the gemstone, not the metal, carries the value.

Gold surged 66% in 2025, its best annual gain since 1979, and the jewelry trade is recalibrating accordingly. With precious metal prices still ascending, a quiet argument is building for pearls, particularly freshwater varieties, as a category where the stone itself commands the room and the gold setting plays a supporting role.

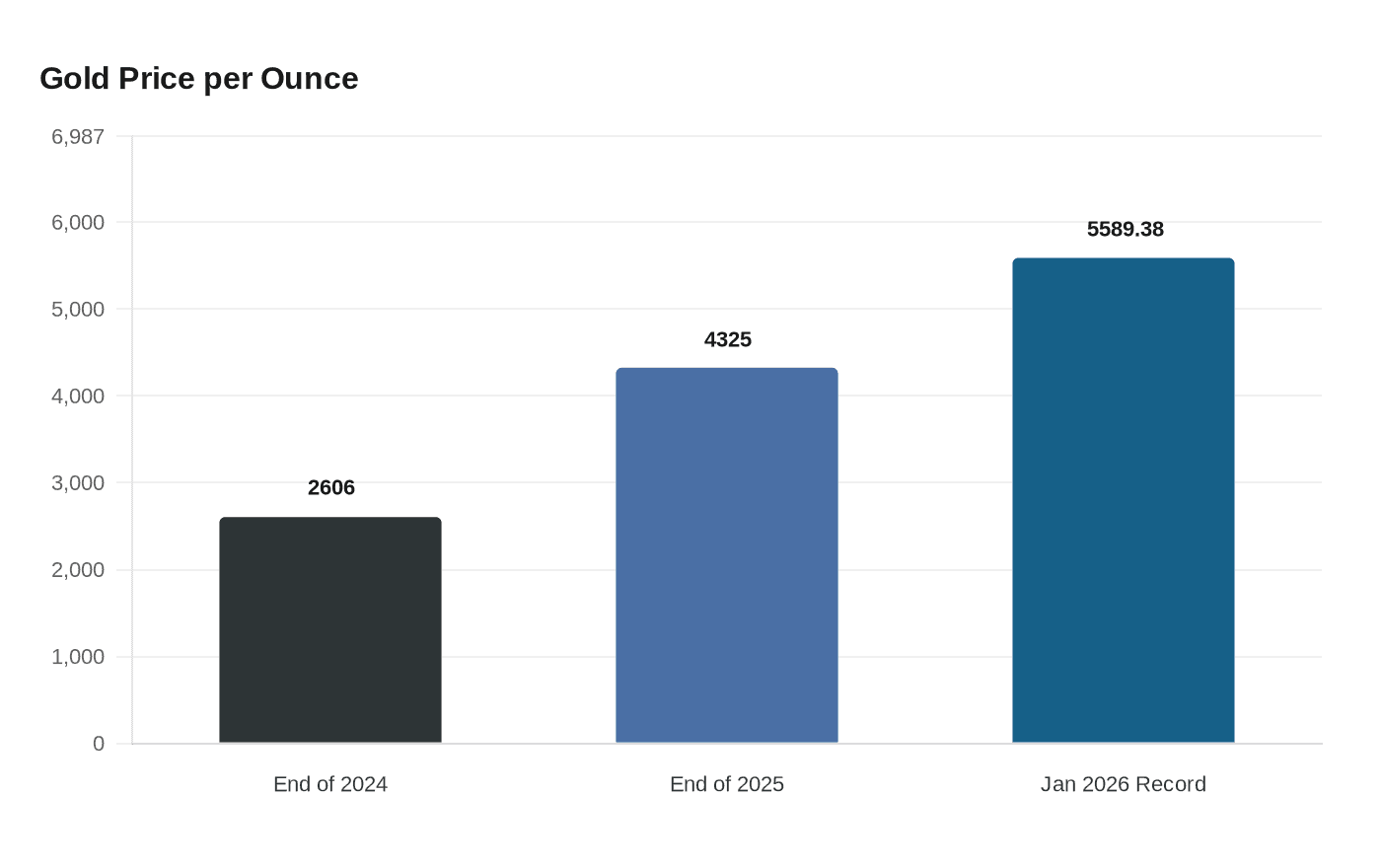

The logic is straightforward. Gold, which sat at roughly $2,606 per ounce at the end of 2024, rallied to around $4,325 by year-end 2025. That momentum culminated in January 2026, when gold surged past the $5,000-per-ounce mark for the first time and reached a record of $5,589.38 per ounce. For jewelers whose designs balance metal weight and stone presence, this is no longer background noise. It is a business model question.

Freshwater pearl values, sourced primarily from Zhuji, the city in Zhejiang Province that has developed over 60 years into the world's largest freshwater pearl production, processing, and sales center, have remained comparatively insulated. "Freshwater pearl values are broadly stable," Raw Pearls noted in a March 25 market report. "For certain sizes the pricing has softened a little while others have risen marginally where supply is tighter." The conclusion drawn: "Pearls represent particularly good value for retailers and their customers." At a time when precious metal prices are historically high, pearls allow retailers to offer "beautiful, substantial jewellery pieces where the focus of the value lies in the gemstone rather than the weight of the metal."

Not every pearl category has held this line. South Sea and Akoya pearls, both saltwater varieties that require oyster farming, have felt the heat from two directions at once: climate stress on oyster populations and persistent labor shortages. Gold prices posted continuous gains in 2025, climbing as much as 55% and surpassing $4,000 per ounce for the first time in October, and pearl supply constraints have compounded that pressure. South Sea and Akoya prices have surged approximately 50% year-over-year, according to market analysis, and the combination of expensive pearls and expensive gold has effectively doubled end-product costs in some segments. The Yoko London example, cited by Vogue Business, makes this concrete: a gold-clasped Akoya-pearl strand that sold for roughly $3,000 before the pandemic now retails for approximately $6,000, driven almost entirely by material cost increases. Buyers in this category should expect to pay more than 50% above 2019 to 2020 values.

The supply picture for freshwater pearls is shifting in a different way, one driven by farming technique rather than climate. As producers increasingly bead-nucleate freshwater mussels, the proportion of round, near-round and off-round pearls continues to grow, concentrating supply in the shapes that dominate fine jewelry demand. The trade-off is visible at the other end of the shape spectrum: baroque, barrel and especially keshi pearls remain in very short supply, a trend that has persisted for several years and shows no sign of reversing.

Logistics costs have added another layer to final retail pricing across all pearl categories. Red Sea shipping disruptions have rerouted luxury cargo onto longer and costlier alternatives, extending transit times from pearl farming regions in Australia, Japan and French Polynesia to buyers in the US and Europe. Insurance premiums on rerouted voyages have risen sharply, and airspace closures have complicated high-value air freight. These costs accumulate before a piece ever reaches a display case.

Retailers have responded with design discipline rather than absorption. Jewelers are lightening settings, reducing gold weights, and reengineering pieces so that the pearl carries more of the visual and material value. Others are introducing lab-grown or reclaimed vintage pearls as cost-managed alternatives, while leveraging provenance and sustainability narratives to support premium pricing on natural and cultured pieces.

The broader market context suggests this pivot has long-term structural support. According to KBVResearch, the global pearl jewelry market is projected to reach $37 billion by 2030 at a compound annual growth rate of 12.9%. Within North America, the US market is forecast to reach $6.67 billion by 2030, while Canada is growing at a CAGR of 15.1% and Mexico at 14.1% over the same period. Central bank and investor demand for gold is set to remain strong, averaging 585 tonnes per quarter in 2026, suggesting that the price dynamics currently favoring pearl-forward jewelry design are unlikely to reverse quickly.

For jewelers and collectors recalibrating their purchases, the freshwater pearl category, particularly classic white rounds sourced from Zhuji's bead-nucleated harvests, currently offers the clearest value proposition in fine jewelry: gem-quality luster, minimal exposure to gold price volatility, and a market still trading below the crisis-level prices seen in saltwater categories. The pearl's ancient claim to elegance has rarely had such a practical economic argument behind it.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?