AI Data Center Infrastructure Stocks Attract Analyst Attention Amid Multi-Year Build-Out

Vertiv's 'grid-to-chip' cooling is becoming the industry standard for Nvidia GPUs, as analysts describe the AI data center build-out as a multi-year, cyclical event.

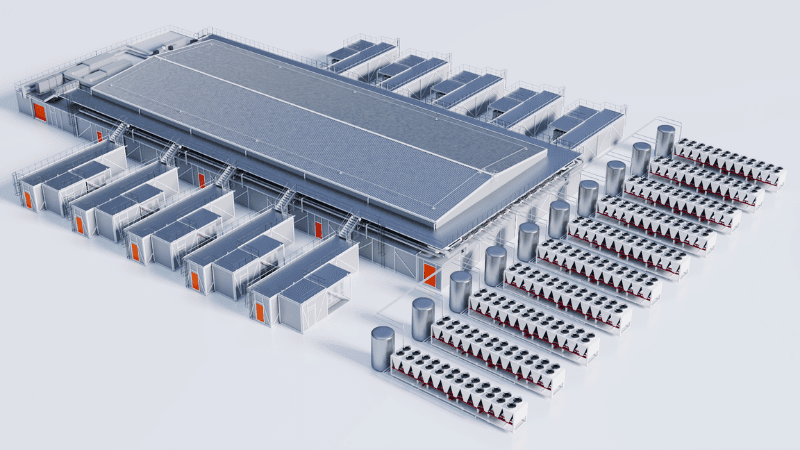

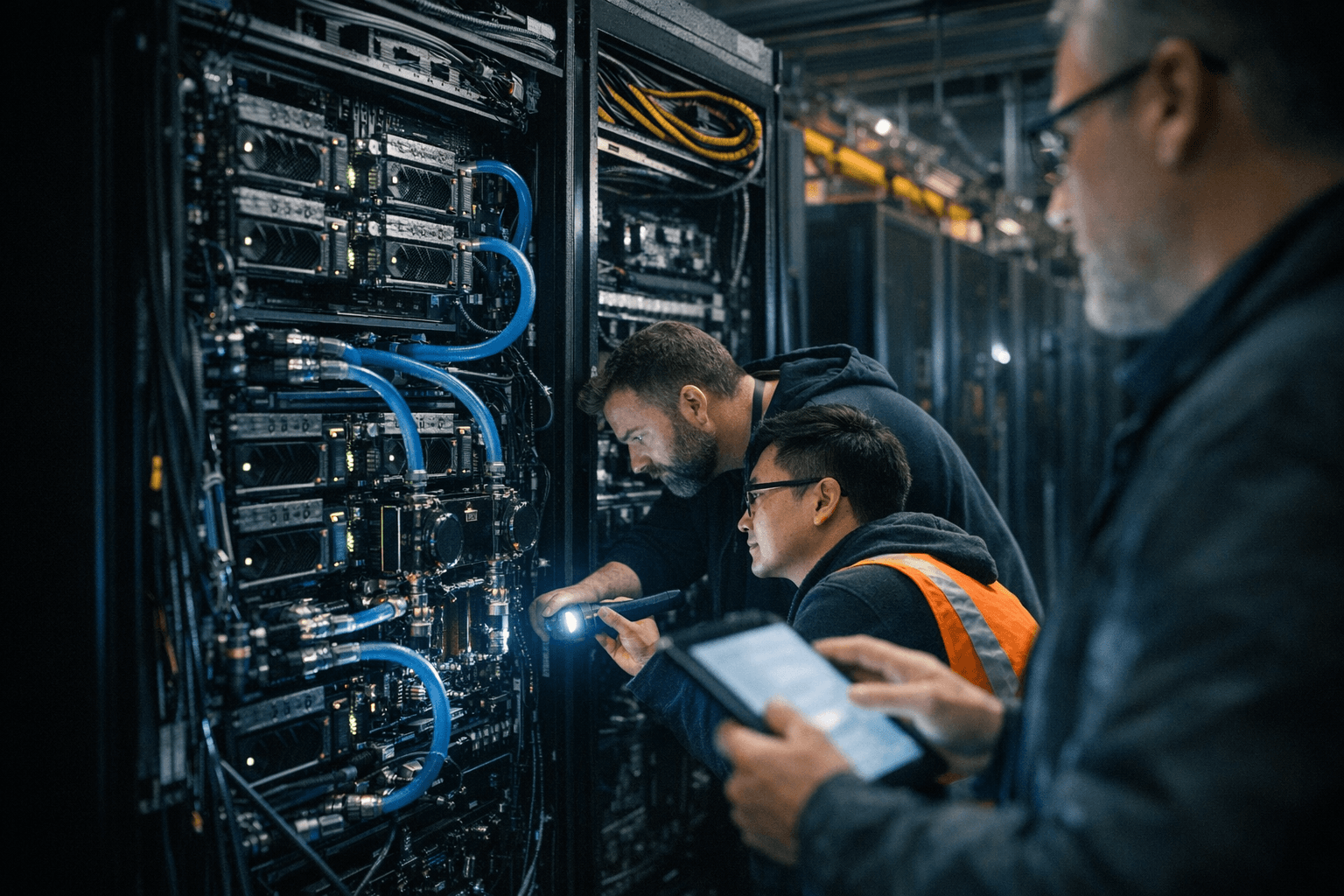

The machines powering today's artificial intelligence workloads run hot enough to force a fundamental rethinking of power and cooling infrastructure, and that physical reality is reshaping where analysts see the most durable investment opportunities in the sector.

Vertiv Holdings Co. (VRT), with a market capitalization of roughly $102 billion and a 0.1% forward dividend yield, has drawn particular attention for its role in solving that problem. The company specializes in the mission-critical power and thermal management systems that keep data centers operational. AI clusters generate more heat and demand significantly more electricity than older, traditional servers, and Vertiv's proprietary liquid cooling technologies and "grid-to-chip" solutions are becoming the industry standard for cooling high-performance GPUs, including those from Nvidia. Analysts have labeled Vertiv the "picks and shovels" leader of the AI data center boom.

Broadcom Inc. (AVGO), valued at $1.5 trillion with a 0.8% forward dividend yield, occupies a different but equally critical position. The company has been described as quietly dominating the plumbing that makes hyperscale data centers actually work. William Kerwin, senior equity analyst for Morningstar, called Broadcom "a prolific generator of cash flow," pointing to the company's long track record of acquiring businesses, streamlining them and turning them into engines of profit.

The broader debate over which specific stocks offer the best exposure to this build-out has drawn investment analysts from multiple platforms. Seeking Alpha contributors Ricardo Fernandez and Petri Dish Reports both weighed in on the sector, with Fernandez characterizing the opportunity in structural terms: the AI data center infrastructure build-out is, in his view, "a multi-year, cyclical event," driven by hyperscalers and major AI developers including OpenAI. The Seeking Alpha discussion also raised questions about how competitive advantages differ among smaller, specialized operators including Nebius, CoreWeave, Applied Digital, and Iren, none of which carry the market capitalization of the infrastructure giants but each of which has attracted scrutiny for its positioning within the AI-native segment of the market.

For investors seeking broader exposure without single-stock concentration, the options range from the Global X Data Center & Digital Infrastructure ETF (DTCR), which holds $1.2 billion in total assets with a 1.4% forward dividend yield, to the Pacer Data and Digital Revolution ETF (TRFK), which holds $446.3 million with a 0.1% yield.

The universe of data center-related names spans an enormous range of scale and yield. Nvidia Corp. (NVDA) stands at $4.4 trillion in market capitalization with a 0.02% forward dividend yield. Microsoft Corp. (MSFT) carries $2.9 trillion and a 0.9% yield. American Tower Corp. (AMT), the cell tower and data center REIT, sits at $87.4 billion and offers the highest forward dividend yield among the frequently cited names at 3.7%. Equinix (EQIX), the colocation giant, has also attracted fresh valuation scrutiny following a strong year-to-date run.

The breadth of that list reflects how the AI infrastructure theme has expanded well beyond semiconductor manufacturers to encompass power management, liquid cooling, network connectivity, real estate and diversified funds. The central debate, which analysts are now actively working through, is whether the largest hyperscalers and chip companies still offer more upside than the infrastructure specialists and smaller AI-native operators that have yet to reach comparable scale. Vertiv and Broadcom's positioning in that argument, one supplying the thermal and power layer and the other the silicon connectivity layer, suggests the most contested ground in the trade is not at the top of the market-cap table.

Know something we missed? Have a correction or additional information?

Submit a Tip