Annuity sales hit record highs as uncertainty boosts demand

Sales climbed to $432.4 billion in 2024, but the fine print still punishes early exits and can leave retirees exposed to inflation.

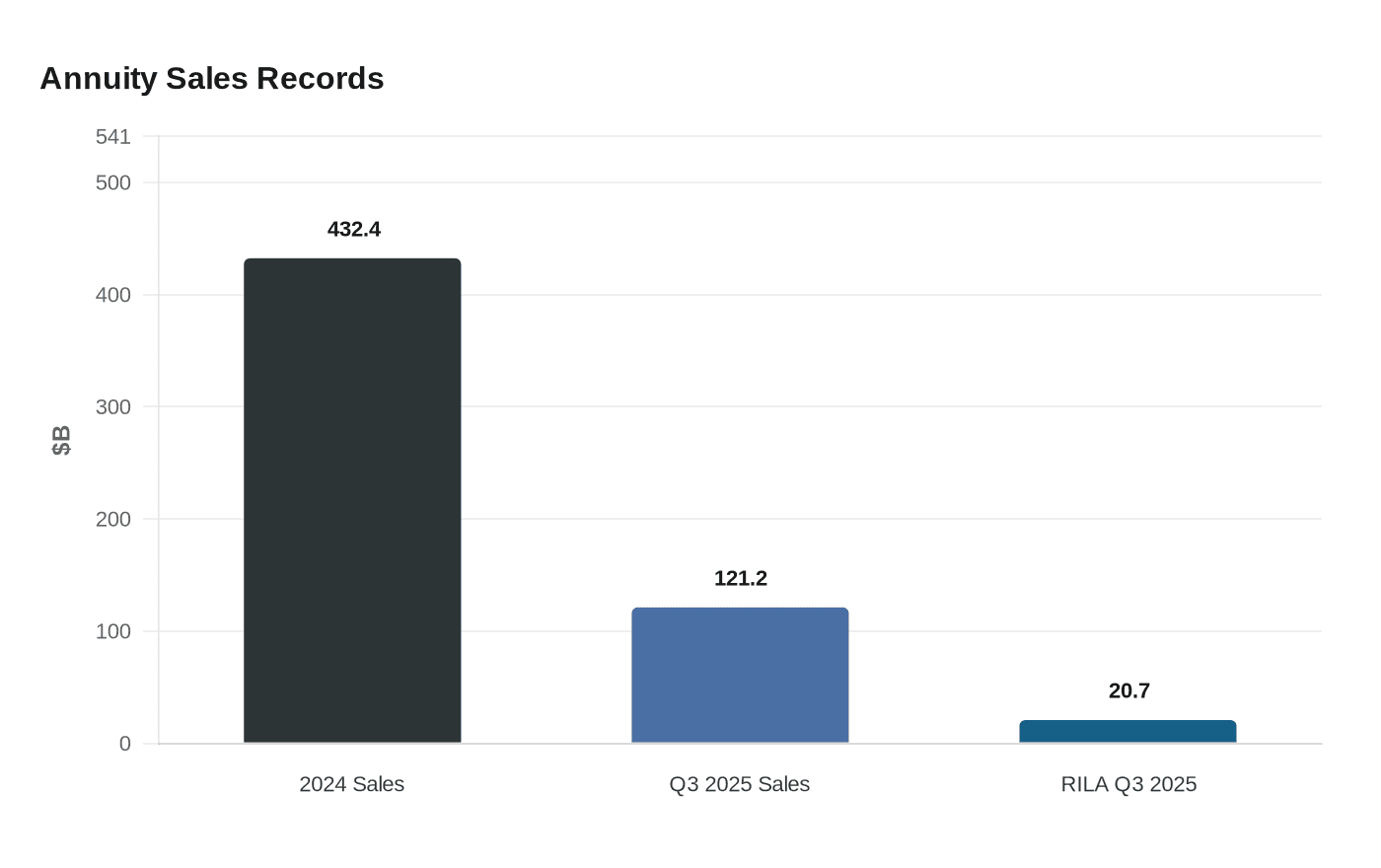

Annuity demand has surged as households search for safety, and the sales numbers show how far the rush has gone. U.S. annuity sales reached a record $432.4 billion in 2024, the third straight year of record highs, and climbed to $121.2 billion in the third quarter of 2025 alone, the first quarterly total above $120 billion. LIMRA said its survey covers 92% of the U.S. market, making the trend hard to ignore.

The appeal is straightforward: an annuity is a contract with an insurance company that can provide tax-deferred growth, income payments and death benefits. In a market shaped by uncertainty, LIMRA said fixed-rate deferred annuity sales have more than doubled from just a few years ago as risk-averse investors sought shelter from volatility. Registered index-linked annuities also posted a quarterly record, with sales of $20.7 billion in the third quarter of 2025, while traditional variable annuities remained a strong source of demand. Fixed indexed annuity sales, by contrast, softened after their record run in 2024.

That enthusiasm comes with tradeoffs that consumers often underestimate. Investor.gov warns that taking money out as a lump sum can trigger surrender charges, taxes and tax penalties. The U.S. Securities and Exchange Commission says buyers of variable annuities should compare costs and benefits carefully and review the prospectus, which lays out fees, charges, investment options, death benefits and payout options. The National Association of Insurance Commissioners has tried to reduce confusion through standardized disclosure documents and buyer’s guides, but the basic warning remains the same: read the paperwork and ask questions before signing.

That makes annuities best suited to a narrow group of buyers in this rate environment. They can fit retirees, or near-retirees, who want a guaranteed income stream and can leave the money alone for years. They are a poor fit for savers who may need cash quickly, because surrender periods can make early withdrawals expensive. They are also an imperfect hedge against inflation, since a fixed payout can lose purchasing power over time even when the headline guarantee looks attractive.

The outlook may shift again if interest rates fall. LIMRA said projected Federal Reserve rate cuts could cool fixed-annuity sales in 2026, which would remove part of the urgency now pushing buyers toward guaranteed products. For consumers, the central question is not whether annuities are popular, but whether the promise of income is worth the fee load, the lockup and the risk that inflation will erode the check later.

Know something we missed? Have a correction or additional information?

Submit a Tip