British house prices flat in March as market loses momentum

British house prices were flat over the year to March, with the average home at £268,000 and demand softening as borrowing costs bite.

British house prices were unchanged in the 12 months to March 2026, leaving the average home valued at £268,000 and signalling a market that has lost momentum after 1.7% annual growth in February. The flat reading matters because it suggests the recent housing cycle has paused rather than built toward a stronger upturn, with affordability pressures still limiting how far prices can rise.

The monthly movement was weaker still. UK house prices fell 0.4% between February and March, a decline the Office for National Statistics said was partly distorted by comparison with a sharp rise a year earlier, when buyers rushed to complete before April 2025 stamp duty changes in England and Northern Ireland. Even with that technical effect, the broader message was clear: price growth has stalled, and the market is no longer delivering the kind of gains that can quickly rebuild household wealth or encourage sellers to test higher asking prices.

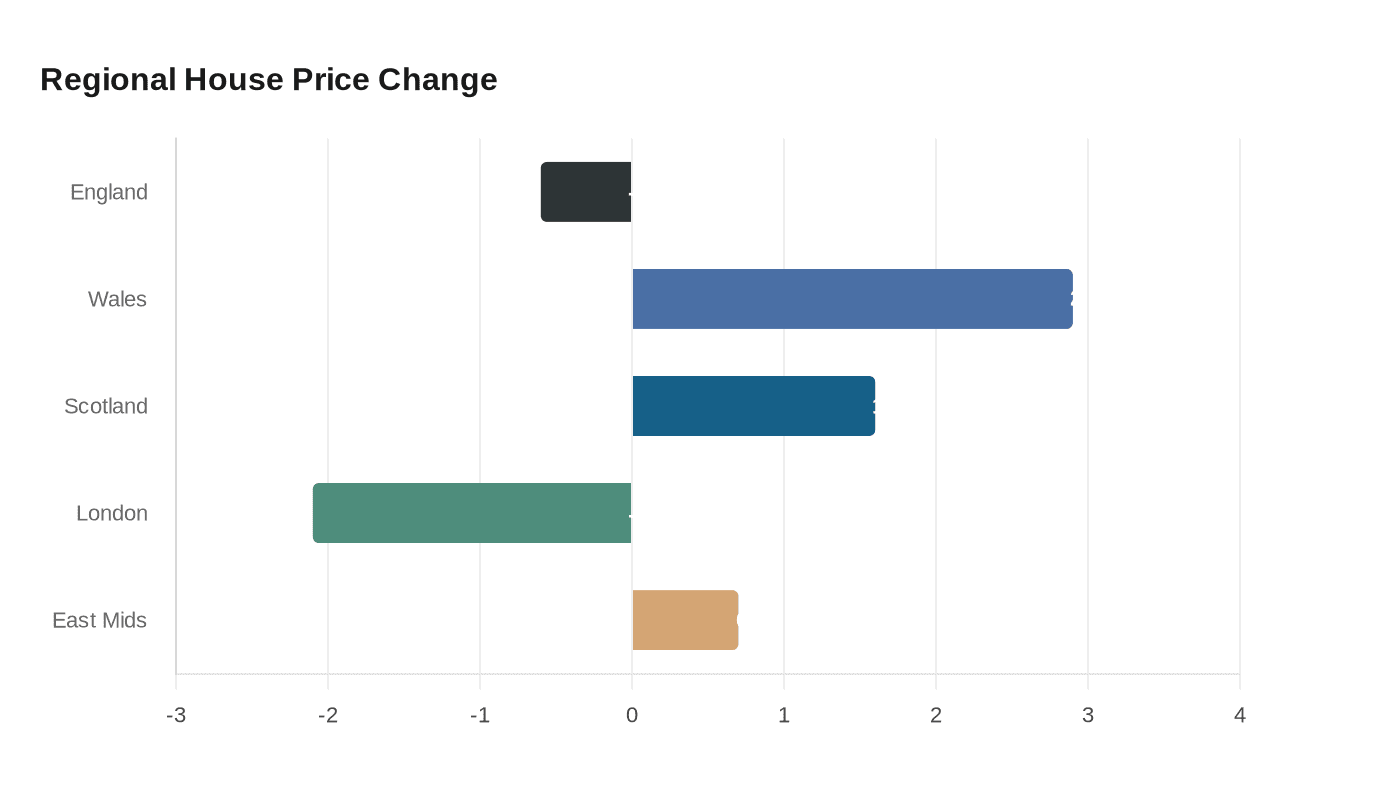

The national figure also masked sharp regional differences. England recorded an average house price of £290,000 in March and an annual fall of 0.6%, while Wales averaged £213,000 and posted 2.9% annual growth. Scotland averaged £187,000, with prices rising 1.6% over the year. London remained the weakest English region, with prices down 2.1% annually, while the East Midlands was the strongest, recording a rise of 0.7%.

The softer tone was already visible in survey data. The Royal Institution of Chartered Surveyors said its March residential survey showed new buyer enquiries at a net balance of -39% and agreed sales at -34%, with surveyors pointing to rising borrowing costs and geopolitical uncertainty as the main drags on demand. RICS said its 12-month outlook for activity and prices had shifted from positive to broadly flat, reinforcing the view that the slowdown was broad-based rather than confined to the official price index.

For first-time buyers, flat prices may ease the pressure to chase a rising market. For existing homeowners, they limit equity gains. For policymakers, the data underline how sensitive Britain’s housing market remains to interest rates, borrowing conditions and buyer confidence, especially after a period when modest gains had suggested a steadier recovery.

Know something we missed? Have a correction or additional information?

Submit a Tip