China factory growth slows in April as cost pressures rise

China’s factory gauge stayed just above growth in April, but Middle East-linked cost pressures and a slide in services pointed to broader global strain.

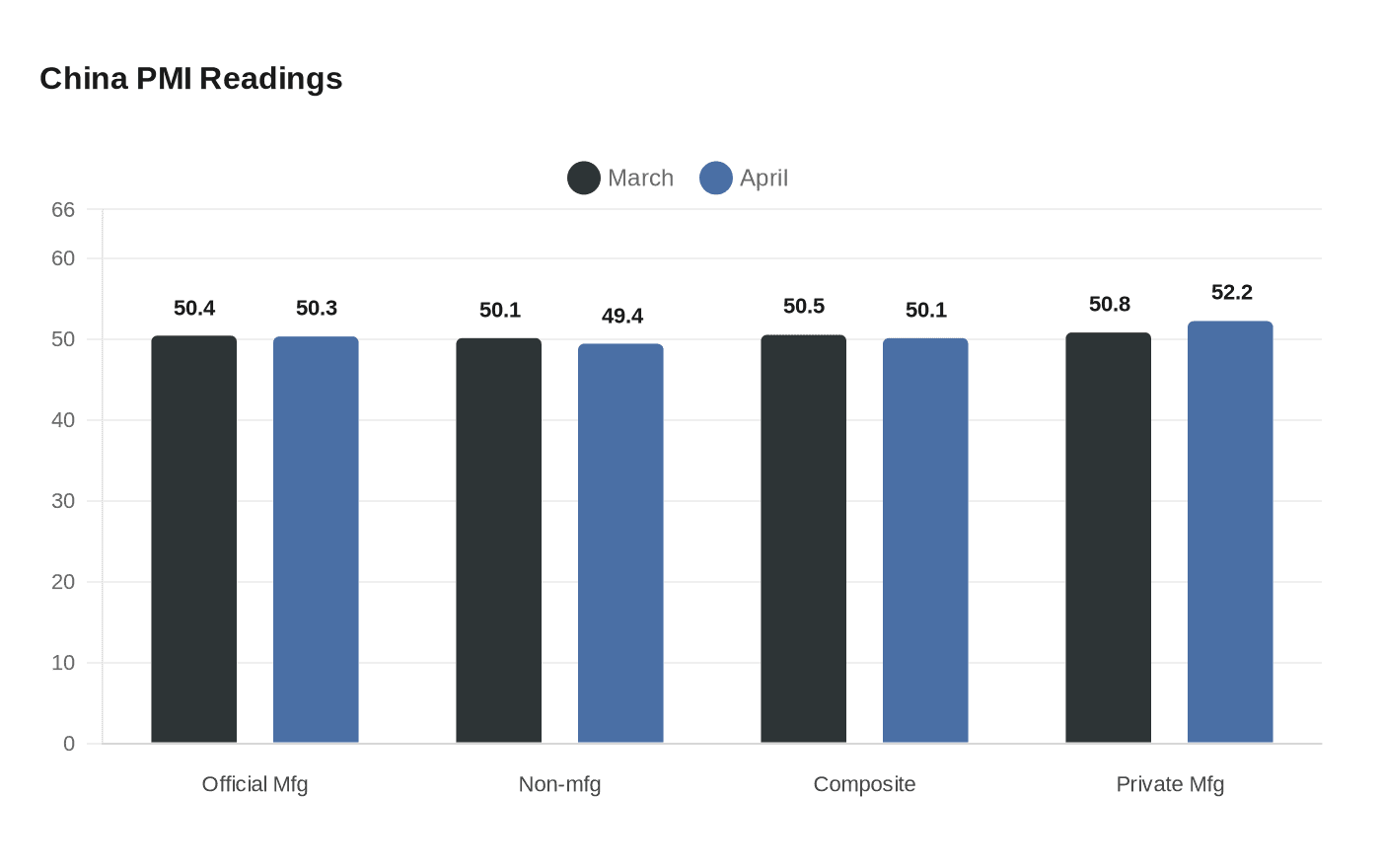

China’s factory sector remained in expansion in April, but only narrowly, as higher costs tied to Middle East tensions and weaker domestic momentum tested the economy’s industrial backbone. The official manufacturing purchasing managers’ index came in at 50.3, down from 50.4 in March and just above the 50 line that separates growth from contraction. A median forecast from 27 economists had pointed to 50.1, underscoring how little room there is between stability and slowdown.

The April reading extended a fragile rebound. March had marked the strongest manufacturing PMI since March 2025 after two months of contraction, and it came alongside signs that the broader economy had started 2026 on firmer footing. First-quarter gross domestic product grew 5%, matching Beijing’s growth floor, industrial profits rose at their fastest pace in six months in March, and factory-gate prices ended a 41-month deflationary streak. April showed that those gains were still vulnerable to outside shocks.

The weakness was clearer beyond factories. The official non-manufacturing PMI fell to 49.4 from 50.1 in March, sliding services and construction into contraction. The composite PMI eased to 50.1 from 50.5, a sign that the economy’s overall pulse weakened even as manufacturing held on. For policymakers in Beijing, that mix is awkward: manufacturing has been a crucial buffer, but it now faces rising input costs and a less supportive domestic backdrop.

A separate private survey painted a very different picture. The RatingDog/S&P Global China General Manufacturing PMI rose to 52.2 in April from 50.8 in March, its strongest reading in more than five years. That gap matters because the private gauge is more sensitive to external demand and more heavily weighted toward private and export-oriented firms, while the official index leans toward larger, state-linked and domestically focused enterprises. Together, the two surveys suggest that some exporters were still benefiting from overseas orders even as the broader economy lost momentum.

The spillover risk is global. If Middle East conflict keeps lifting shipping, energy and materials costs, Chinese factories will face tighter margins, and those pressures can travel through supply chains into Asia, the United States and Europe. For U.S. inflation, the danger is not just higher freight and input costs; it is also a steadier squeeze on imported goods prices if congestion and energy markets worsen. April’s numbers suggest this may still be a blip driven by external shocks, but they also read like an early warning that softer global growth could be taking shape.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?