China producer prices hit 45-month high as energy costs rise

China’s factory-gate inflation climbed to a 45-month high in April, signaling that higher energy costs could ripple into global supply chains and U.S. import prices.

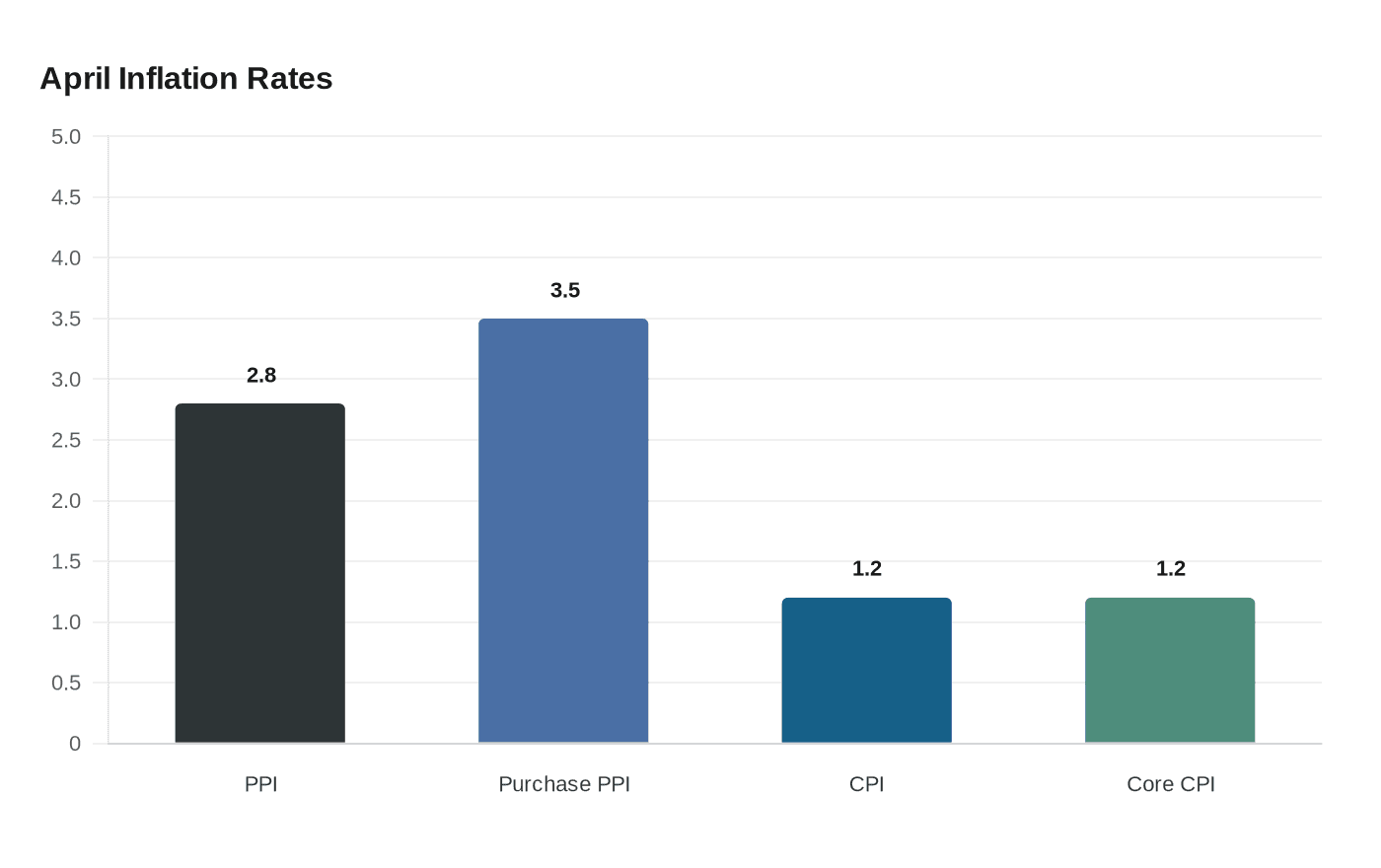

China’s producer prices climbed to a 45-month high in April as rising energy costs fed into factories, adding a fresh warning sign for global inflation even as domestic demand stayed only modest. The National Bureau of Statistics said producer prices rose 2.8% from a year earlier and 1.7% from March, the fastest annual gain since July 2022 and the second straight month of increases after a 41-month slide ended in March.

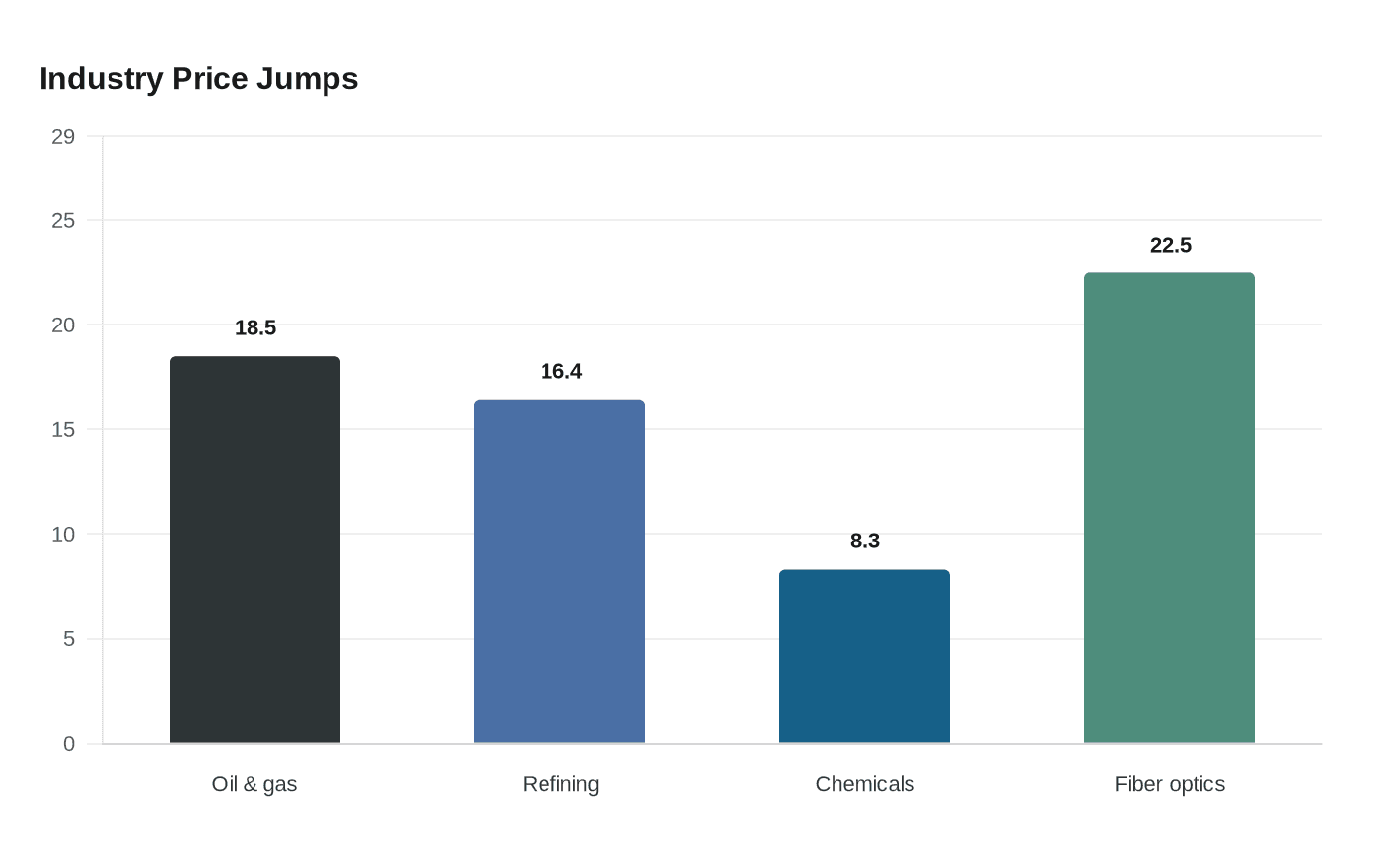

The surge was concentrated in energy- and materials-linked industries. Oil and gas extraction prices jumped 18.5% from March, petroleum refining prices rose 16.4%, chemical raw materials and products increased 8.3%, and optical fiber manufacturing climbed 22.5%. Producer purchase prices, a measure of costs paid by manufacturers for raw materials, rose 3.5% year on year and 2.1% month on month, underscoring how higher input costs are moving deeper into industrial supply chains.

Consumer inflation also firmed, but only gently. China’s consumer price index rose 1.2% from a year earlier and 0.3% from March, while core CPI also advanced 1.2% year on year. The statistics bureau said the monthly consumer price rise reflected higher energy and travel-service costs during the Qingming and May Day holiday period, not a broad-based revival in spending. That matters for policymakers in Beijing, because it suggests price pressure is still coming more from imported cost shocks than from overheating demand.

Analysts said the latest rise in factory inflation was consistent with energy disruption linked to the Middle East and the war involving Iran, but they did not see it as the start of a wider inflation cycle. Reuters reported that the April PPI reading was well above the 1.6% gain expected in its poll, while Bloomberg said economists had looked for a median 1.8% rise. Even so, the pressure remains narrow enough that a major policy response looks unlikely, since China’s bigger problem is still weak domestic demand rather than runaway prices.

For the global economy, the risk is in the transmission channel. When Chinese factory costs rise, exporters can either absorb the hit or pass it on through higher prices for finished goods, parts and industrial inputs. For U.S. consumers, that can show up later in pricier imports. For U.S. manufacturers, it can mean tighter margins on components sourced from China, especially in energy-intensive lines of production. China’s April data does not signal an inflation spiral, but it does show how quickly energy shocks can move from the Middle East into Chinese factories and then outward through global trade.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?