China’s wind power surge, subsidies and imports built global dominance

China turned wind power into an industrial weapon. Subsidies, local-content rules and a giant home market helped it dominate turbines, offshore buildout and global supply chains.

China’s wind power surge is now a power-system story

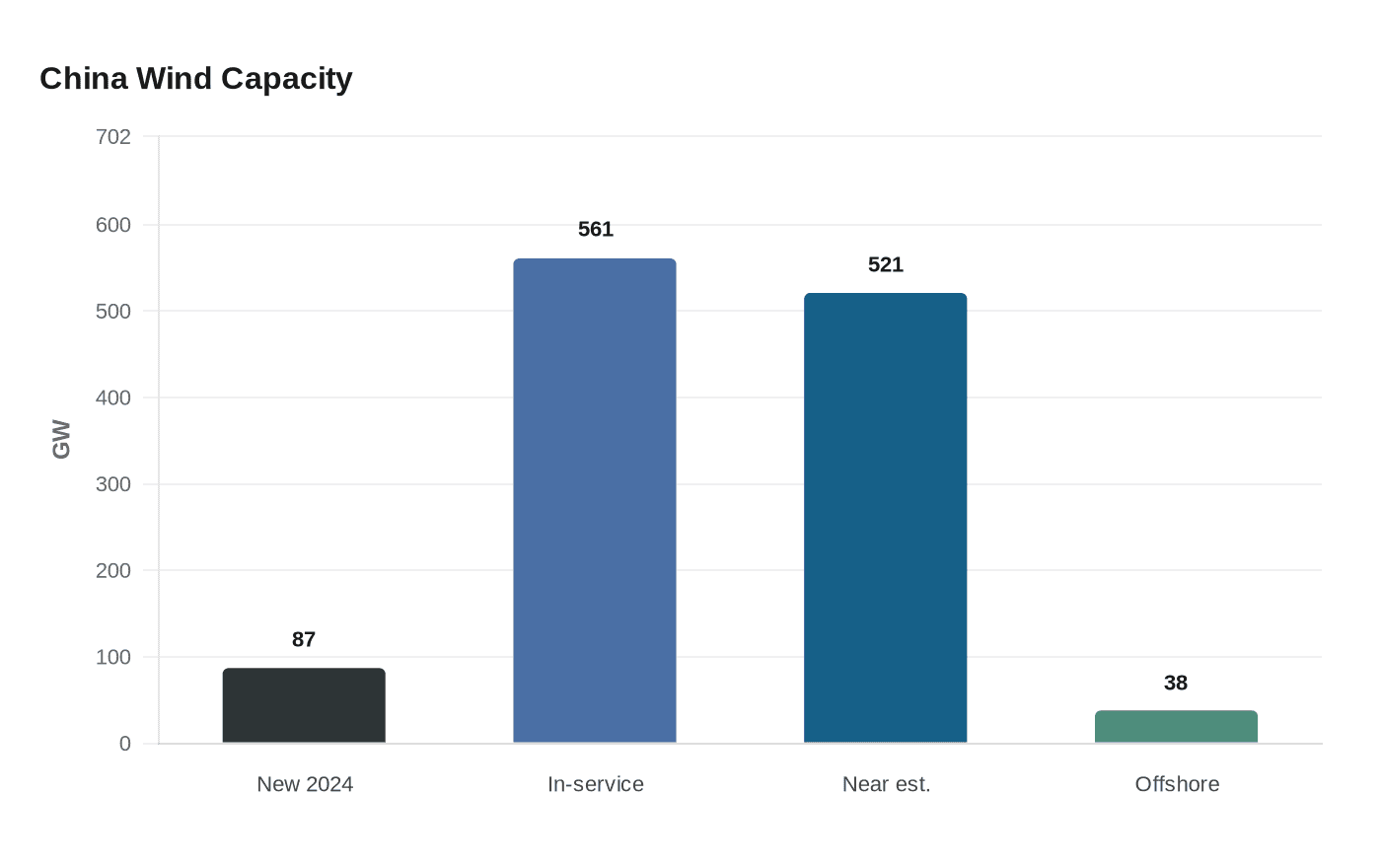

China installed 87 gigawatts of new wind power in 2024, a scale of buildout that would rank among the largest national energy additions anywhere in the world. The Chinese Wind Energy Association says that pushed cumulative in-service wind capacity to 561 GW, while other industry summaries put China near 521 GW and note that wind and solar together surpassed coal capacity in early 2025. However the accounting is done, the direction is unmistakable: China is not just adding turbines, it is building a dominant position in the next generation of electricity infrastructure.

That dominance matters beyond climate policy. Wind power is becoming part of the broader energy-security contest as countries try to reduce exposure to volatile fossil-fuel markets, especially when oil prices remain high or unstable. Beijing has treated that shift as an industrial opportunity, using the same playbook that made it powerful in solar panels, then applying it to wind, where scale, state support and trade barriers have given Chinese firms a structural advantage.

The policy foundation came first, then the market explosion

China’s wind industry did not become dominant by accident. The foundation was laid through feed-in tariffs introduced in 2009, domestic content requirements and direct subsidies that pushed utilities and developers toward Chinese-made equipment. Those policies created a protected domestic market at exactly the moment when the global industry was still expanding, allowing local firms to gain manufacturing experience, cut costs and move up the technology curve.

The political fight over those policies is not new. In 2011, after a World Trade Organization challenge, the U.S. Trade Representative said China had ended a wind-equipment subsidy program that had awarded grants since 2008 to manufacturers using Chinese-made parts instead of imports. The grants reportedly ranged from $6.7 million to $22.5 million each, and the broader program may have amounted to several hundred million dollars. That episode showed how tightly China linked industrial policy and import substitution, using public money not just to support clean power, but to keep value-added manufacturing inside its borders.

Scale inside China has become the real engine of global power

China’s home market is now so large that it sets the pace for the world. The World Wind Energy Association says China accounted for about 72 percent of all new global wind capacity added in 2024, a staggering share for one country. That kind of concentration does more than raise annual totals. It gives Chinese manufacturers a production base, a domestic project pipeline and procurement volume that no rival market can easily match.

The same scale is visible offshore. China’s installed offshore wind capacity was reported at 38 GW in 2024, making it the global leader in a sector where global capacity remains limited relative to potential. Offshore wind is technically demanding, capital-intensive and strategically important because it sits closer to the power grids that will carry future industrial demand. By leading there as well, China is not just expanding generation. It is setting standards for turbines, supply chains, ports, vessels and grid integration.

Chinese turbine makers have moved from participants to leaders

The industrial payoff is showing up in company rankings. Wood Mackenzie says Goldwind, Envision and MingYang finished as the top three global wind turbine original equipment manufacturers in 2024, the first time the Chinese trio filled the top spots together. Goldwind led with 20 GW installed, a sign that the strongest player in the market is now also one of the biggest in the world.

That matters because turbine manufacturing is where margins, intellectual property, and supplier relationships converge. Once local firms dominate their home market, they can spread fixed costs across more units, negotiate better terms for components and deepen their hold on global supply chains. In practical terms, China’s wind machine now shapes everything from nacelle production and blade materials to shipping, installation services and long-term maintenance.

Europe is already reacting to the pressure

The European Commission opened a 2024 investigation into suspected subsidies for Chinese wind turbine suppliers in Spain, Greece, France, Romania and Bulgaria. That is a major signal that Europe sees wind not just as an energy transition story, but as an industrial and competitive one. The concern is straightforward: if heavily supported Chinese imports keep arriving at lower prices, they can squeeze European manufacturers, weaken domestic investment and, in the worst case, hollow out parts of the region’s clean-energy supply chain.

This is where trade policy and energy policy start to merge. Europe needs more wind capacity to meet decarbonization goals, but it also wants industrial resilience and strategic autonomy. Those goals are becoming harder to reconcile when China can combine state support, large-scale manufacturing and a protected internal market to drive prices down faster than rivals can respond.

What it means for the United States and global energy leverage

For the United States, China’s wind rise is a warning about how quickly a strategic sector can be captured when industrial policy is coordinated and persistent. The U.S. once challenged China over wind subsidies in the WTO, but the larger issue has only grown: if China controls a rising share of turbine manufacturing and associated supply chains, it gains leverage over equipment availability, pricing and standards in markets far beyond its borders.

The geopolitical stakes are real because wind is becoming a core part of electricity systems, not a niche add-on. As more countries replace coal and add power to serve data centers, factories and electrified transport, whoever controls the hardware for those grids will influence the terms of the transition. China’s wind buildout, backed by subsidies, import restrictions and manufacturing scale, gives Beijing a stronger hand not only in clean energy, but in global industrial competition.

The lesson from 2024 is that wind power is now a hard-edged economic asset. China used policy to build the market, scale to crush costs and trade pressure to protect its manufacturers. That combination has made it the central power in a technology that will shape electricity systems, supply chains and geopolitical influence for years to come.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?