Debt consolidation loans can cost more than credit cards, experts warn

Debt consolidation only works when the new APR, fees and payoff timeline beat your current debt. In this rate environment, many borrowers are finding the opposite.

Debt consolidation is not automatically cheaper

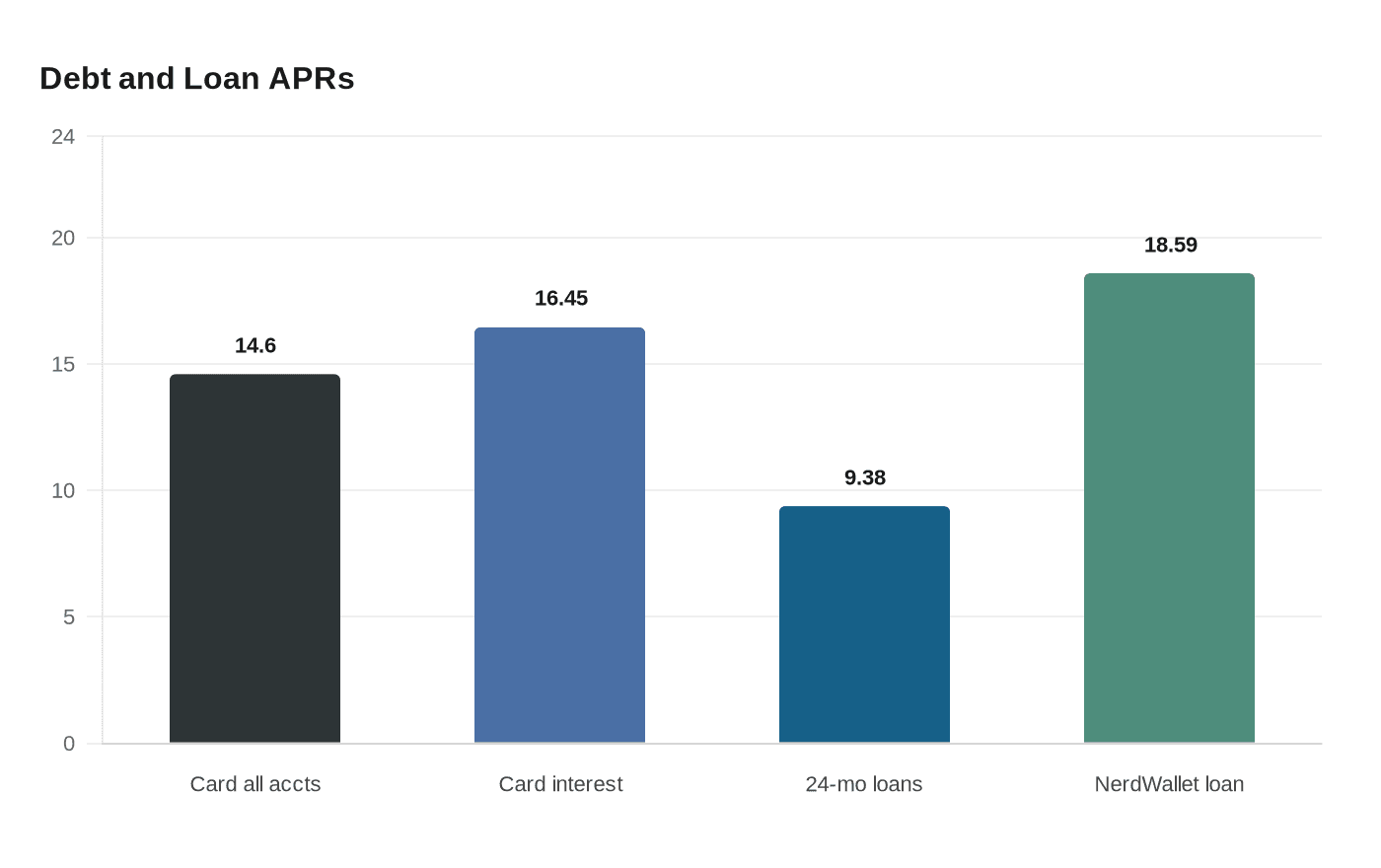

Debt consolidation sounds like relief, but the math has become unforgiving. A new loan only saves money if its APR is lower than the debt it replaces, and the Federal Reserve Board’s latest G.19 consumer credit data show why that test matters: credit card plans average 14.60% for all accounts and 16.45% for accounts assessed interest, while 24-month personal loans at commercial banks sit at 9.38%. That spread looks helpful on paper, but it can vanish once fees, term length and borrower qualifications enter the picture.

The biggest trap is that advertised rates are often not the rates real borrowers receive. NerdWallet said good-credit borrowers who pre-qualified for debt consolidation loans over the last 30 days received an average rate of 18.59% as of May 1, 2026. That is higher than both of the Federal Reserve’s credit card benchmarks, which means some consumers who move balances into a consolidation loan could end up paying more interest than if they had left the debt on the card.

Why the current rate environment cuts both ways

The Federal Reserve’s G.19 release is published around the fifth business day of each month, and the version cited here was published April 7, 2026. That matters because borrowing costs are moving targets, not fixed truths. A consolidation loan that looks attractive in one month can become expensive quickly if card rates ease, if loan quotes worsen, or if a borrower’s credit profile changes between shopping and signing.

The policy backdrop also explains why many consumers are tempted to consolidate now. Credit card debt remains costly, and the gap between card rates and personal loan rates can appear large enough to justify a switch. But the spread in official averages is only a starting point. The real decision depends on the rate a lender actually offers, the length of the loan, and whether the new payment schedule creates genuine savings or just stretches the debt farther into the future.

Balance transfers have their own fine print

For cardholders, a balance transfer can look like the cleanest escape hatch, especially when a promotional 0% or low-interest offer is available. The Consumer Financial Protection Bureau says those promotional rates usually last only a limited time, which means the window for savings can be short. If the balance is not paid off before the promo ends, the remaining debt can roll into a much higher rate.

The CFPB also warns that balance transfer fees can still apply even on a zero-percent offer. That detail can erase a meaningful share of the benefit, especially on larger balances. A borrower who focuses only on the introductory rate may miss the fee on the front end and the regular APR on the back end, two costs that can make an apparently cheap transfer more expensive than staying put.

When consolidation helps, and when it quietly worsens the damage

Consolidation can still be useful, but only under specific conditions. The new rate has to beat the weighted average of the debts being rolled in, the fee structure has to be modest, and the repayment schedule has to be realistic. If the loan term is longer than the remaining life of the original debt, the monthly bill may fall while total interest rises. That is the classic household-finance trap: cash flow relief today, a larger bill tomorrow.

A quick reality check can help separate true savings from expensive reshuffling:

- Compare the offered APR with the APRs on your current debts, not just the minimum payment.

- Add fees, including balance transfer charges, into the total cost.

- Check whether a promotional rate expires before the balance is gone.

- Estimate the full payoff timeline, not just the monthly payment.

- Ask whether the new loan is actually improving your debt load or simply extending it.

That last point is especially important because consolidation often feels like progress even when the balance barely changes. Lower monthly payments can create breathing room, but they can also tempt borrowers to stop paying down principal aggressively. If the debt takes longer to disappear, the household may end up spending more over time even though the monthly bill looks friendlier.

Not every consolidation firm deserves trust

The Consumer Financial Protection Bureau says some credit card debt consolidation companies are legitimate but risky, and it recommends consulting a nonprofit credit counselor first. That advice matters because the industry can blur the line between help and salesmanship. Some firms may present consolidation as a cure-all when the real need is budgeting, credit counseling or a structured repayment plan.

A nonprofit counselor can help separate the arithmetic from the marketing. The question is not whether a lower payment sounds good, but whether the borrower can actually retire the debt faster and at a lower total cost. For households already under pressure, a careful review can prevent a move that feels like relief but functions like a more expensive reshuffle.

The bottom line for borrowers

Debt consolidation works best when it is a disciplined refinance, not a rescue fantasy. In the current market, official Federal Reserve data show card borrowing is expensive, but real-world consolidation quotes can be even higher than card rates, especially after fees and term changes are included. Balance transfers can also disappoint once promotional periods and transfer charges are factored in.

The safest approach is brutally simple: compare the APR, count the fees, measure the payoff timeline and verify that the new plan lowers the total cost of the debt. If it does not, the better move is often to keep the balance where it is and attack it with a plan that does not add another layer of cost.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?