Debt settlement can backfire, fees, lawsuits and tax surprises await

Debt settlement can look like relief, but fees, lawsuits and a surprise tax bill can leave you worse off. The safer first move is often your card issuer.

When debt settlement is the wrong move

Debt forgiveness is not a clean reset if the plan depends on stopping payments, paying steep fees, and hoping creditors cooperate. The Consumer Financial Protection Bureau warns that debt settlement companies often charge expensive fees, may tell consumers to stop paying credit card bills, and may urge people to stop communicating with their card issuer, all of which can make a difficult situation more dangerous.

The clearest warning signs are easy to spot. A company that guarantees it can make your debt disappear, tells you to stop making minimum payments, or insists you cut off contact with your credit card company should raise immediate concern. The CFPB says those are red flags, and federal consumer-protection rules also bar most debt settlement companies from collecting fees before they actually settle or resolve a debt.

Debt settlement is also not a universal fix. Some creditors refuse to work with settlement firms, and not all debts can be settled. That means a borrower can pay fees for a service that still leaves some balances unresolved, while interest and late charges continue to pile up in the background.

The hidden costs that can follow missed payments

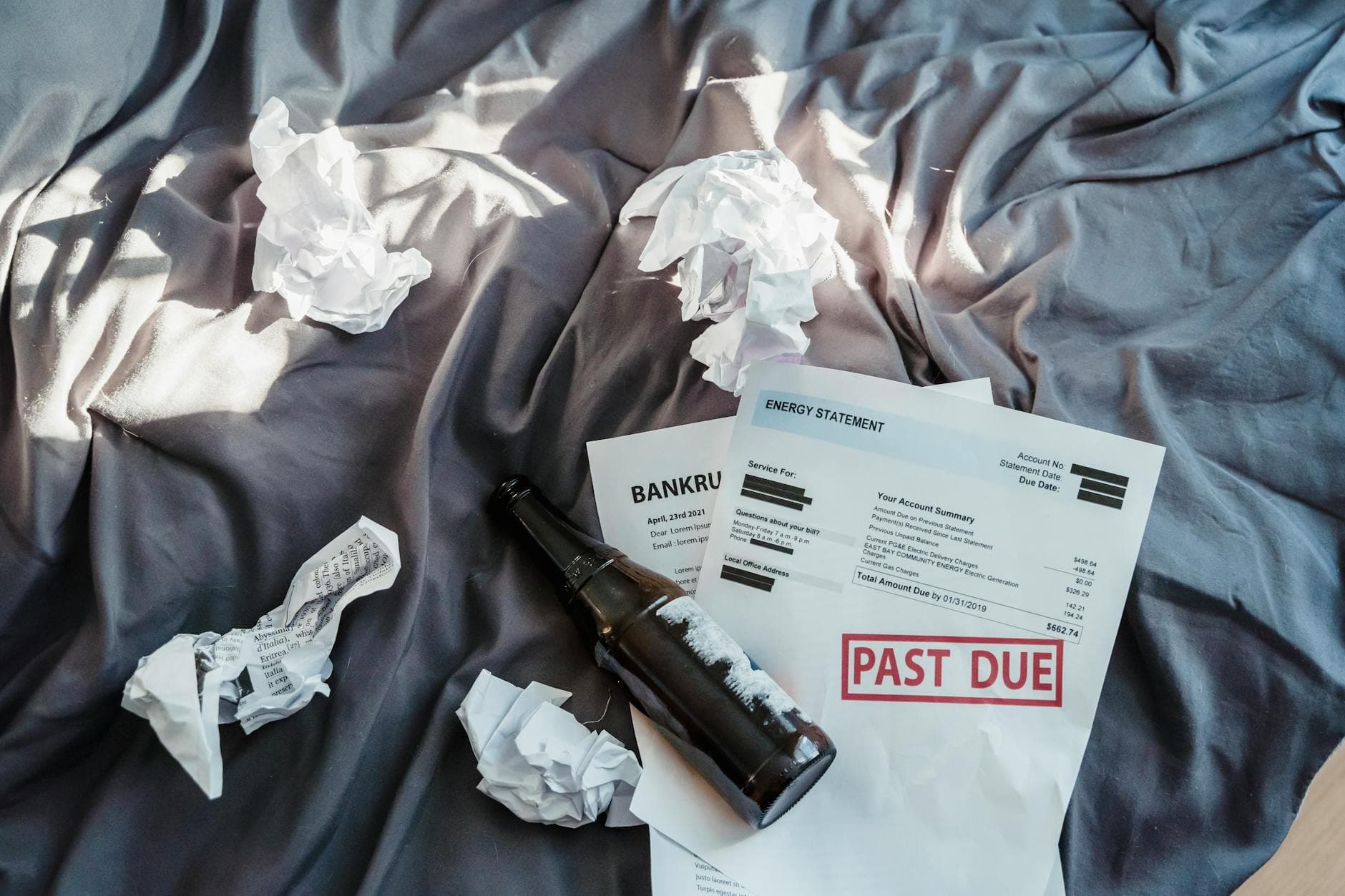

Stopping payments to chase a settlement can trigger a cascade of costs. The CFPB says consumers can face late fees, penalty interest, more collection activity, and even lawsuits after they fall behind. Those consequences matter because the strategy often relies on creating delinquency before a settlement is reached, which can damage financial standing long before any creditor agrees to compromise.

That is why settlement can reduce credit access rather than restore it. Once an account is delinquent, lenders may see a higher-risk borrower, and collection pressure can intensify. For someone already under stress, the total cost of the plan can end up higher than expected, especially if the settlement never covers every account.

The tax bill many borrowers do not see coming

Another reason settlement can backfire is tax treatment. The Internal Revenue Service generally treats canceled, forgiven or discharged debt as taxable income unless an exception applies. In practice, that means a borrower may get debt relief and still owe taxes on the amount that was wiped away.

The usual paperwork is Form 1099-C, which lenders typically send when they cancel debt. That form can turn a financial rescue into a filing issue, because the forgiven amount may need to be reported on a tax return if it is taxable. Borrowers who are already stretched thin can be surprised by a tax bill months after they thought the debt problem was behind them.

There are important exceptions, but they do not apply automatically. The IRS says insolvent taxpayers may be able to exclude forgiven debt from income to the extent of insolvency. Certain debt can also qualify for exclusion in bankruptcy, for qualified farm indebtedness, or for qualified real property business indebtedness. Those rules can soften the blow, but they do not eliminate the need to check tax consequences before agreeing to forgiveness.

What to do first if credit card bills are piling up

If you are overwhelmed by card debt, the CFPB says the first call should usually go to the card issuer, not a settlement company. Many issuers offer hardship or repayment options that can be less damaging than defaulting into a settlement process, especially if the problem is temporary, such as a job interruption, medical expense, or short-term cash crunch.

That direct approach can be especially useful when the account is still current or only recently overdue. A hardship plan may reduce the monthly payment, adjust the interest rate, or create a temporary schedule that keeps the account from sliding deeper into delinquency. It will not erase the debt, but it may preserve credit standing better than a settlement strategy that requires missed payments.

Why nonprofit credit counseling often costs less

Nonprofit credit counseling is different from debt settlement and debt consolidation, and that distinction matters. The CFPB says credit counseling organizations are usually nonprofits and typically advise and educate consumers on managing money and debts, often at little or no cost. That makes counseling a useful middle ground for borrowers who need structure, budgeting help, and a realistic repayment plan.

Counseling is often a better fit when the borrower can still repay debt over time but needs help organizing the path. Unlike for-profit settlement firms, nonprofit counselors are focused on budgeting and repayment plans rather than persuading creditors to accept a reduced balance after payment has already been interrupted. For many households, that makes counseling the safer first stop.

Where balance transfers fit, and where they do not

Balance-transfer strategies can help some borrowers, but only in the right situation. They are most useful when credit is still good enough to qualify for a lower-rate card and the borrower can pay the balance down before a promotional period ends. If the debt is small enough and the repayment horizon is clear, a transfer can buy time without the credit damage that often comes with settlement.

But balance transfers are not a cure for chronic overextension. If the borrower cannot reasonably pay down the debt during the promotional window, the remaining balance can roll into a higher rate later and recreate the same pressure in a different form. That makes transfers a tactical tool, not a long-term fix for debt that already exceeds realistic repayment capacity.

When bankruptcy may be the more honest answer

For borrowers whose debts are too large to repay and whose cash flow cannot support a workable plan, bankruptcy can be a more direct legal remedy than settlement. The IRS rules matter here too, because certain debts discharged in bankruptcy are excluded from taxable income. That can make bankruptcy less tax-trappy than private forgiveness arrangements, depending on the facts.

It is still a serious step, with long-lasting credit consequences, but it may be the most rational choice when unsecured debt, collection pressure, and rising fees have made other options unrealistic. The key difference is that bankruptcy is a court-supervised process, while settlement is often a private negotiation that can leave borrowers exposed to fees, tax surprises, and lawsuits before any deal is done.

Debt relief only helps when it actually lowers the full cost of getting back on track. If the plan depends on hidden fees, broken payment habits, or a tax form you were not expecting, the bargain may be worse than the problem.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?